Table of contents

- Example active heading

- Example heading

There are many different kinds of small business loans, making it essential to do your research before beginning any application process.

Before you kick off any loan process, make sure you know the following:

The following information covers the common types of business loans. Pay attention to the dollar amounts, rates, terms, and qualification criteria to help you choose the small business loan type perfectly suited for your business needs.

A term loan provides a lump sum of money repaid in monthly installments with interest over a set term.

Common use cases: A business term loan is a great way to acquire working capital, expand business operations, purchase equipment, or hire additional staff.

Typical terms: Term loan amounts range from $5K to $500K with a repayment period between six months and 10 years. You can often see that money in as little as 1-3 days. These loans generally have a fixed interest rate, but some lenders may offer a variable rate that fluctuates with the market.

Minimum eligibility requirements: Each lender will have its eligibility criteria. In general, minimum requirements for a term loan include a 600 credit score, $8K in monthly revenue, and one year in business.

| Pros of a Business Term Loan | Cons of a Business Term Loan |

| Fixed repayment schedule - a term loan has a clear repayment timeline, which helps businesses plan and manage their budget | Collateral required - A term loan often requires collateral, which could be a risk if the business fails to repay the loan. |

| Lower interest rates - Compared to other types of loans, term loans usually come with lower interest rates. | Strict requirements - The eligibility criteria for term loans tend to be stricter, which might not suit businesses with lower credit scores. |

| Access to larger amounts - Term loans typically allow businesses to borrow larger amounts, which can be beneficial for significant investments or expenditures. | Long-term commitment - The repayment of term loans span over a long period which might not suit businesses wanting short-term solutions. |

| Building Credit - Regular and timely repayments can increase a business' credit score. | Early repayment penalties - Some lenders might charge a penalty for paying off the loan earlier than the agreed term. |

Unlike a traditional loan, where you receive a lump sum all at once, a line of credit allows you to borrow only what you need and pay interest on the amount you use. Think of it as a credit card for your business, but typically with lower interest rates and higher borrowing limits.

Common use cases: This flexibility makes it an excellent tool for managing cash flow, handling unexpected expenses, or addressing short-term funding needs.

Typical terms: You can get anywhere from $1,000 to $250,000, and the money is typically available in one to two days with a 6- to 18-month maturity. Most lenders charge a simple interest rate on the amount you draw with no prepayment penalty.

Minimum eligibility requirements: If you’ve been in business for more than half a year, are bringing in $50,000 or more in annual revenue, and have a credit score of 600 or higher, consider yourself a prime candidate.

The Small Business Administration (SBA) was created to assist small businesses through various educational and funding programs. SBA loans are unique because the SBA isn’t the lender. Rather, it guarantees a substantial portion of each loan, which reduces other lenders’ risk and makes them more willing to approve your request.

Common use cases: SBA loans are typically used for working capital or to purchase fixed assets such as equipment or real estate.

Typical terms: With an SBA loan, you can expect amounts from less than $50K up to $5M. Terms also cover a broad range, typically from 10-25 years. Expect the entire process to take 1-2 months.

Types of SBA loans: The SBA offers an array of loans to small business owners. Here are a few of the most popular options:

Minimum eligibility requirements: SBA loans have stringent credit requirements. You’ll need a minimum credit score of 650, at least two years in business, and a minimum of $8,000 in monthly revenue to be considered by an SBA lender.

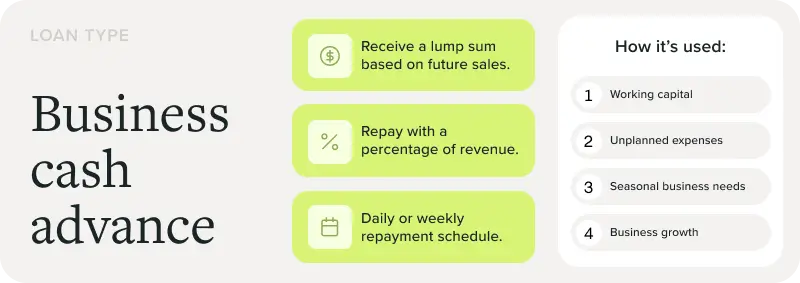

Revenue-based financing borrows against your future earnings to secure the financing you need. Once you’ve been approved and the funds are advanced to your account, you’ll repay the funder a fixed daily amount via a withdrawal from your bank account. Some funders offer a merchant cash advance where you’ll have an agreed-upon percentage of your daily credit card deposits withheld for the lender.

Common use cases: Revenue-based financing can be used for any business expense. Common use cases include working capital, covering seasonal business needs, and expansion costs.

Typical terms: Revenue-based financing is known for speedy delivery. You can apply for anywhere from $5,000 to $500,000, and time to funds can be as short as 24 hours. A cash advance comes with a factor rate instead of an interest rate. Factor rates are expressed as a decimal number, such as 1.5. To calculate payback, multiply the total borrowed by the factor rate. For example, $10,000 borrowed x 1.5-factor rate = $15,000 total payback.

Minimum eligibility requirements: Qualifying for revenue-based financing is surprisingly simple because the nature and terms of the loan make the risk lower for a lender. Minimum credit score requirements start at 500. You’ll need a minimum monthly revenue of $10,000 and a minimum time in business of three months to qualify for a cash advance.

Equipment financing is a specialized form of financing used to purchase equipment. With amounts available up to $5 million, you can use them to buy any kind of equipment your business might need.

Common use cases: When most people hear the word “equipment,” they think of heavy equipment like backhoes, trucks, tractors, refrigerators, and trash compactors. But this type of financing can also be used for less obvious equipment, such as payment processing programs, solar panels, or accounting software for your office. The point is, if the purchase will equip your business for its needs, it probably meets the criteria.

Typical terms: Equipment financing is available from $5K-$5M with terms from one to 10 years. After submitting your application, you may see funds in as little as 24 hours. Interest rates start as low as 7.5%. The equipment you purchase will serve, at least in part, as collateral for the loan, so you may need less additional collateral than you would for other loan types. Some funders may require a down payment.

Minimum eligibility requirements: Qualifying for equipment financing is easier than many other types of loans. If your business has been running for a year or more, brings in $50,000 or more in annual revenue, and has a credit score of 520 or above, you should be sitting pretty. Some equipment financing companies will work with day-one startups. The lender will also evaluate the value and condition of the equipment as part of the approval process.

A commercial mortgage or commercial real estate loan is used to purchase or renovate commercial property such as an office building or warehouse.

Common use cases: A commercial mortgage can be used for just about any property need, whether that’s retail space, an office, a warehouse, or a restaurant. If you’ve been around for decades and want to expand, that’s no problem. Ready to purchase your first location? Perfect.

Typical terms: A commercial mortgage is similar to a home mortgage but with a few key differences. One, you’ll need to provide a down payment. There are typically no options for 100% financing. Two, the terms will be shorter, typically 10-25 years. Three, some commercial real estate loans come with a balloon payment at the end of the term, which is one large payment that pays off the remaining balance of the loan.

This financing option is an asset-based loan, so the amount and rate of your commercial mortgage will be based on your credit and the value of the property you’ll be using as collateral. You can expect amounts ranging from $250,000 to $5,000,000. The interest rates are usually on the lower end, starting at around 6.25%.

Minimum eligibility requirements: Qualifying for a commercial mortgage loan requires a clear plan for how you’ll put the cash to use. For example, if you’ll be making renovations to a property, your lender will want to know how you intend to do it and will also assess the after-repair value (or ARV) of the property.

Lenders will also look for:

You can plan on a lender requesting several property-related documents, including the purchase contract, property blueprints, market analysis for the property, project budget, scope of work, and assessment of the property’s existing condition.

Invoice factoring (sometimes called accounts receivable factoring) is tailor-made for when you need money but cashflow is tied up in outstanding invoices. With this type of financing, you’ll sell your outstanding invoices to a factoring company that will pay you a percentage of the invoice’s value upfront. The factoring company will collect the money from your customer when the invoice comes due and pay you back any remaining balance minus the factoring fee.

Common use cases: Invoice factoring is frequently used to boost cash flow, cover short-term expenses, and manage business seasonality.

Typical terms: The amounts vary, but you can often get up to 80% of your receivables. The money arrives in as little as 24 hours, and the loan term can last up to a year. As for the factoring fee, it starts as low as 3%.

Minimum eligibility requirements: To qualify for invoice factoring, your business must be B2B or B2G, have a minimum monthly revenue of $10K, and operate in the funder’s preferred industry.

The term “startup loan” can be a bit of a misnomer. While there are a handful of lenders who will work with day-one startups, it’s rare to find financing to start a brand-new business. However, there are still business loan options available for young startups with only a year or two in business. Common loan types for startups include revenue-based financing, invoice factoring, and equipment financing. The SBA also offers two programs for startups: SBA microloans and the Community Advantage program. These programs are meant to support underserved communities and will typically have less stringent qualifying criteria.

A business acquisition loan is used to buy an existing business or franchise.

Typically these loans will be structured as a term loan or line of credit used to purchase equipment, real estate, and intangible assets. SBA loans can also be used to acquire an existing business.

The loan terms will be specific to the loan type, lender, and specific acquisition costs. In general, expect lenders to look for a minimum credit score of 650, steady revenue, post-acquisition business plans and financial projections, and in many cases a significant cash contribution to the overall purchase. Lastly, lenders will want to know about any relevant experience to help you run the business successfully.

Short-term loans are repaid in a term of six months to three years. They can be structured as a term loan, revenue-based financing, a line of credit, or invoice factoring. Be aware that many term loans with short term lengths will require a daily or weekly payment similar to revenue-based financing.

Many entrepreneurs use short-term loans when they need quick solutions to pressing circumstances. So whether you need to pay for unexpected expenses, hire new staff, endure a sales slump, replace a broken piece of equipment, or take action on an exciting business opportunity, a short-term loan can be a solid option.

Of all the types of small business financing out there, the business credit card is the most user-friendly. If you’ve had a personal credit card, you know how it works. You can access amounts up to $500,000 with a business credit card, with interest rates from 8-24%. It’s not unusual to get a 0% introductory rate. There’s very little paperwork required compared to many loans, and the time to funds rarely exceeds 2 weeks.

This option is excellent for those who don’t feel ready to pursue a business loan or have been repeatedly turned down for them in the past. You’ll boost your working capital with fast access to cash, plus get the added benefits of leveraging a card rewards program and building your credit.

Business credit cards can be used for just about anything related to your operations. Whether you need to buy a new dump truck, add inventory, expand your office, take a client out to lunch, or hold an off-site staff event, this financing can be just the ticket.

Qualifying for a card isn’t difficult, which makes it a good match for those who are new to business. As long as you’ve got a credit score above 680 and have a decent business history, you should be in good shape.

Once you click submit on a loan application, the lender will use multiple factors to determine their response. These same factors also play a role in determining the loan’s terms and rates if you’re approved.

So how are approval decisions made? Here are 6 essential factors lenders use to evaluate your business credit and decide whether or not to open their wallet to you.

| Factors lenders use to evaluate your business credit |

| Personal credit – You can almost always expect lenders to be keenly interested in your business credit. But your business credit is inextricably linked to your personal credit, so it’s safe to assume they’ll also want to take a look at your personal financial health. This information typically includes your credit in use, credit history, payment history, and amounts owed. |

| Personal debt coverage – Again, your personal and business finances are related, so a lender will be interested in your personal debt coverage. If you’ve got a healthy state of affairs, expect lenders will consider you less of a risk and will be more keen to work with you. |

| Business debt coverage – There’s no problem with your business carrying debt. The question is whether your business can handle its debt obligations. To get a bead on your business debt coverage, a lender evaluates your cash flow and debt payments. |

| Personal debt utilization – If you’re carrying personal debt, you’re in good company. About 80% of Americans have some form of debt. What can set you apart from the masses is if you have credit available that you’re not currently using. To get this metric, a lender will divide your outstanding debt by the cumulative amount of your available revolving credit. |

| Business debt utilization – Lenders also care about the state of your business debt. Having debt isn’t a big deal. What matters is whether the amount of debt you’re carrying is appropriate compared to the size of your business and the industry you’re working in. This assessment comes from comparing your outstanding business debt to your assets and revenue. |

| Business revenue trend – Lenders are more motivated to work with you if your business is trending in the right direction, so they’ll want to ascertain what your average revenue growth will be over time. If yours lands at or above the average for your industry, you’re in great shape. If you fall below the average, plan on there being some possible challenges in your pursuit of financing. |

It’s often beneficial to speak with an expert who can evaluate your financing needs and guide you toward the best financing solutions. By doing your research, asking the right questions, and keeping your mind open, you’ll be setting yourself up for success.

Many small business owners find short-term loans, equipment financing, or merchant cash advances easier to qualify for—especially if they have lower credit scores or limited time in business.

SBA loans typically offer the most competitive interest rates, but they also have stricter eligibility requirements and a longer approval process.

The best loan depends on your specific business needs. Whether it’s managing cash flow, buying equipment, or expanding operations. Lendio’s loan marketplace helps match you with the right option based on your goals.

Yes, some loan types, like invoice financing, revenue-based financing, and certain equipment loans, are available to businesses with less-than-perfect credit. Just expect higher rates or shorter terms.

Some lenders provide same-day or next-day funding, especially for short-term loans and MCAs. SBA loans and term loans typically take longer—anywhere from a few days to several weeks.

Not always. While some loans (like equipment financing) are secured, others (business lines of credit or unsecured term loans) don’t require collateral, though they may require a personal guarantee.

A term loan gives you a lump sum upfront, which you repay over a fixed schedule. A line of credit offers flexible access to funds. You borrow only what you need and pay interest on what you use.

The information provided on this blog is for general informational purposes only, and should not be construed as business, legal, tax, accounting or financial advice. Readers should consult with a qualified professional before making any business, financial, or legal decisions. The views and opinions expressed in this blog are solely those of the authors and do not necessarily reflect the official policy, position, or endorsements of Lendio. While Lendio strives to keep its content current, it is accurate only as of the date posted. Business trends, financial conditions, regulations, and offers are subject to change without notice and may no longer be relevant or available. Lendio expressly disclaims all liability for any reliance placed on this information. By accessing this blog, you acknowledge and agree that Lendio shall not be held liable for any direct, indirect, incidental, consequential, or other damages arising from your use or reliance on the information provided.

Applying is free and won’t impact your credit1.

There are many different kinds of small business loans, making it essential to do your research before beginning any application process.

Before you kick off any loan process, make sure you know the following:

The following information covers the common types of business loans. Pay attention to the dollar amounts, rates, terms, and qualification criteria to help you choose the small business loan type perfectly suited for your business needs.

A term loan provides a lump sum of money repaid in monthly installments with interest over a set term.

Common use cases: A business term loan is a great way to acquire working capital, expand business operations, purchase equipment, or hire additional staff.

Typical terms: Term loan amounts range from $5K to $500K with a repayment period between six months and 10 years. You can often see that money in as little as 1-3 days. These loans generally have a fixed interest rate, but some lenders may offer a variable rate that fluctuates with the market.

Minimum eligibility requirements: Each lender will have its eligibility criteria. In general, minimum requirements for a term loan include a 600 credit score, $8K in monthly revenue, and one year in business.

| Pros of a Business Term Loan | Cons of a Business Term Loan |

| Fixed repayment schedule - a term loan has a clear repayment timeline, which helps businesses plan and manage their budget | Collateral required - A term loan often requires collateral, which could be a risk if the business fails to repay the loan. |

| Lower interest rates - Compared to other types of loans, term loans usually come with lower interest rates. | Strict requirements - The eligibility criteria for term loans tend to be stricter, which might not suit businesses with lower credit scores. |

| Access to larger amounts - Term loans typically allow businesses to borrow larger amounts, which can be beneficial for significant investments or expenditures. | Long-term commitment - The repayment of term loans span over a long period which might not suit businesses wanting short-term solutions. |

| Building Credit - Regular and timely repayments can increase a business' credit score. | Early repayment penalties - Some lenders might charge a penalty for paying off the loan earlier than the agreed term. |

Unlike a traditional loan, where you receive a lump sum all at once, a line of credit allows you to borrow only what you need and pay interest on the amount you use. Think of it as a credit card for your business, but typically with lower interest rates and higher borrowing limits.

Common use cases: This flexibility makes it an excellent tool for managing cash flow, handling unexpected expenses, or addressing short-term funding needs.

Typical terms: You can get anywhere from $1,000 to $250,000, and the money is typically available in one to two days with a 6- to 18-month maturity. Most lenders charge a simple interest rate on the amount you draw with no prepayment penalty.

Minimum eligibility requirements: If you’ve been in business for more than half a year, are bringing in $50,000 or more in annual revenue, and have a credit score of 600 or higher, consider yourself a prime candidate.

The Small Business Administration (SBA) was created to assist small businesses through various educational and funding programs. SBA loans are unique because the SBA isn’t the lender. Rather, it guarantees a substantial portion of each loan, which reduces other lenders’ risk and makes them more willing to approve your request.

Common use cases: SBA loans are typically used for working capital or to purchase fixed assets such as equipment or real estate.

Typical terms: With an SBA loan, you can expect amounts from less than $50K up to $5M. Terms also cover a broad range, typically from 10-25 years. Expect the entire process to take 1-2 months.

Types of SBA loans: The SBA offers an array of loans to small business owners. Here are a few of the most popular options:

Minimum eligibility requirements: SBA loans have stringent credit requirements. You’ll need a minimum credit score of 650, at least two years in business, and a minimum of $8,000 in monthly revenue to be considered by an SBA lender.

Revenue-based financing borrows against your future earnings to secure the financing you need. Once you’ve been approved and the funds are advanced to your account, you’ll repay the funder a fixed daily amount via a withdrawal from your bank account. Some funders offer a merchant cash advance where you’ll have an agreed-upon percentage of your daily credit card deposits withheld for the lender.

Common use cases: Revenue-based financing can be used for any business expense. Common use cases include working capital, covering seasonal business needs, and expansion costs.

Typical terms: Revenue-based financing is known for speedy delivery. You can apply for anywhere from $5,000 to $500,000, and time to funds can be as short as 24 hours. A cash advance comes with a factor rate instead of an interest rate. Factor rates are expressed as a decimal number, such as 1.5. To calculate payback, multiply the total borrowed by the factor rate. For example, $10,000 borrowed x 1.5-factor rate = $15,000 total payback.

Minimum eligibility requirements: Qualifying for revenue-based financing is surprisingly simple because the nature and terms of the loan make the risk lower for a lender. Minimum credit score requirements start at 500. You’ll need a minimum monthly revenue of $10,000 and a minimum time in business of three months to qualify for a cash advance.

Equipment financing is a specialized form of financing used to purchase equipment. With amounts available up to $5 million, you can use them to buy any kind of equipment your business might need.

Common use cases: When most people hear the word “equipment,” they think of heavy equipment like backhoes, trucks, tractors, refrigerators, and trash compactors. But this type of financing can also be used for less obvious equipment, such as payment processing programs, solar panels, or accounting software for your office. The point is, if the purchase will equip your business for its needs, it probably meets the criteria.

Typical terms: Equipment financing is available from $5K-$5M with terms from one to 10 years. After submitting your application, you may see funds in as little as 24 hours. Interest rates start as low as 7.5%. The equipment you purchase will serve, at least in part, as collateral for the loan, so you may need less additional collateral than you would for other loan types. Some funders may require a down payment.

Minimum eligibility requirements: Qualifying for equipment financing is easier than many other types of loans. If your business has been running for a year or more, brings in $50,000 or more in annual revenue, and has a credit score of 520 or above, you should be sitting pretty. Some equipment financing companies will work with day-one startups. The lender will also evaluate the value and condition of the equipment as part of the approval process.

A commercial mortgage or commercial real estate loan is used to purchase or renovate commercial property such as an office building or warehouse.

Common use cases: A commercial mortgage can be used for just about any property need, whether that’s retail space, an office, a warehouse, or a restaurant. If you’ve been around for decades and want to expand, that’s no problem. Ready to purchase your first location? Perfect.

Typical terms: A commercial mortgage is similar to a home mortgage but with a few key differences. One, you’ll need to provide a down payment. There are typically no options for 100% financing. Two, the terms will be shorter, typically 10-25 years. Three, some commercial real estate loans come with a balloon payment at the end of the term, which is one large payment that pays off the remaining balance of the loan.

This financing option is an asset-based loan, so the amount and rate of your commercial mortgage will be based on your credit and the value of the property you’ll be using as collateral. You can expect amounts ranging from $250,000 to $5,000,000. The interest rates are usually on the lower end, starting at around 6.25%.

Minimum eligibility requirements: Qualifying for a commercial mortgage loan requires a clear plan for how you’ll put the cash to use. For example, if you’ll be making renovations to a property, your lender will want to know how you intend to do it and will also assess the after-repair value (or ARV) of the property.

Lenders will also look for:

You can plan on a lender requesting several property-related documents, including the purchase contract, property blueprints, market analysis for the property, project budget, scope of work, and assessment of the property’s existing condition.

Invoice factoring (sometimes called accounts receivable factoring) is tailor-made for when you need money but cashflow is tied up in outstanding invoices. With this type of financing, you’ll sell your outstanding invoices to a factoring company that will pay you a percentage of the invoice’s value upfront. The factoring company will collect the money from your customer when the invoice comes due and pay you back any remaining balance minus the factoring fee.

Common use cases: Invoice factoring is frequently used to boost cash flow, cover short-term expenses, and manage business seasonality.

Typical terms: The amounts vary, but you can often get up to 80% of your receivables. The money arrives in as little as 24 hours, and the loan term can last up to a year. As for the factoring fee, it starts as low as 3%.

Minimum eligibility requirements: To qualify for invoice factoring, your business must be B2B or B2G, have a minimum monthly revenue of $10K, and operate in the funder’s preferred industry.

The term “startup loan” can be a bit of a misnomer. While there are a handful of lenders who will work with day-one startups, it’s rare to find financing to start a brand-new business. However, there are still business loan options available for young startups with only a year or two in business. Common loan types for startups include revenue-based financing, invoice factoring, and equipment financing. The SBA also offers two programs for startups: SBA microloans and the Community Advantage program. These programs are meant to support underserved communities and will typically have less stringent qualifying criteria.

A business acquisition loan is used to buy an existing business or franchise.

Typically these loans will be structured as a term loan or line of credit used to purchase equipment, real estate, and intangible assets. SBA loans can also be used to acquire an existing business.

The loan terms will be specific to the loan type, lender, and specific acquisition costs. In general, expect lenders to look for a minimum credit score of 650, steady revenue, post-acquisition business plans and financial projections, and in many cases a significant cash contribution to the overall purchase. Lastly, lenders will want to know about any relevant experience to help you run the business successfully.

Short-term loans are repaid in a term of six months to three years. They can be structured as a term loan, revenue-based financing, a line of credit, or invoice factoring. Be aware that many term loans with short term lengths will require a daily or weekly payment similar to revenue-based financing.

Many entrepreneurs use short-term loans when they need quick solutions to pressing circumstances. So whether you need to pay for unexpected expenses, hire new staff, endure a sales slump, replace a broken piece of equipment, or take action on an exciting business opportunity, a short-term loan can be a solid option.

Of all the types of small business financing out there, the business credit card is the most user-friendly. If you’ve had a personal credit card, you know how it works. You can access amounts up to $500,000 with a business credit card, with interest rates from 8-24%. It’s not unusual to get a 0% introductory rate. There’s very little paperwork required compared to many loans, and the time to funds rarely exceeds 2 weeks.

This option is excellent for those who don’t feel ready to pursue a business loan or have been repeatedly turned down for them in the past. You’ll boost your working capital with fast access to cash, plus get the added benefits of leveraging a card rewards program and building your credit.

Business credit cards can be used for just about anything related to your operations. Whether you need to buy a new dump truck, add inventory, expand your office, take a client out to lunch, or hold an off-site staff event, this financing can be just the ticket.

Qualifying for a card isn’t difficult, which makes it a good match for those who are new to business. As long as you’ve got a credit score above 680 and have a decent business history, you should be in good shape.

Once you click submit on a loan application, the lender will use multiple factors to determine their response. These same factors also play a role in determining the loan’s terms and rates if you’re approved.

So how are approval decisions made? Here are 6 essential factors lenders use to evaluate your business credit and decide whether or not to open their wallet to you.

| Factors lenders use to evaluate your business credit |

| Personal credit – You can almost always expect lenders to be keenly interested in your business credit. But your business credit is inextricably linked to your personal credit, so it’s safe to assume they’ll also want to take a look at your personal financial health. This information typically includes your credit in use, credit history, payment history, and amounts owed. |

| Personal debt coverage – Again, your personal and business finances are related, so a lender will be interested in your personal debt coverage. If you’ve got a healthy state of affairs, expect lenders will consider you less of a risk and will be more keen to work with you. |

| Business debt coverage – There’s no problem with your business carrying debt. The question is whether your business can handle its debt obligations. To get a bead on your business debt coverage, a lender evaluates your cash flow and debt payments. |

| Personal debt utilization – If you’re carrying personal debt, you’re in good company. About 80% of Americans have some form of debt. What can set you apart from the masses is if you have credit available that you’re not currently using. To get this metric, a lender will divide your outstanding debt by the cumulative amount of your available revolving credit. |

| Business debt utilization – Lenders also care about the state of your business debt. Having debt isn’t a big deal. What matters is whether the amount of debt you’re carrying is appropriate compared to the size of your business and the industry you’re working in. This assessment comes from comparing your outstanding business debt to your assets and revenue. |

| Business revenue trend – Lenders are more motivated to work with you if your business is trending in the right direction, so they’ll want to ascertain what your average revenue growth will be over time. If yours lands at or above the average for your industry, you’re in great shape. If you fall below the average, plan on there being some possible challenges in your pursuit of financing. |

It’s often beneficial to speak with an expert who can evaluate your financing needs and guide you toward the best financing solutions. By doing your research, asking the right questions, and keeping your mind open, you’ll be setting yourself up for success.

There are many different kinds of small business loans, making it essential to do your research before beginning any application process.

Before you kick off any loan process, make sure you know the following:

The following information covers the common types of business loans. Pay attention to the dollar amounts, rates, terms, and qualification criteria to help you choose the small business loan type perfectly suited for your business needs.

A term loan provides a lump sum of money repaid in monthly installments with interest over a set term.

Common use cases: A business term loan is a great way to acquire working capital, expand business operations, purchase equipment, or hire additional staff.

Typical terms: Term loan amounts range from $5K to $500K with a repayment period between six months and 10 years. You can often see that money in as little as 1-3 days. These loans generally have a fixed interest rate, but some lenders may offer a variable rate that fluctuates with the market.

Minimum eligibility requirements: Each lender will have its eligibility criteria. In general, minimum requirements for a term loan include a 600 credit score, $8K in monthly revenue, and one year in business.

| Pros of a Business Term Loan | Cons of a Business Term Loan |

| Fixed repayment schedule - a term loan has a clear repayment timeline, which helps businesses plan and manage their budget | Collateral required - A term loan often requires collateral, which could be a risk if the business fails to repay the loan. |

| Lower interest rates - Compared to other types of loans, term loans usually come with lower interest rates. | Strict requirements - The eligibility criteria for term loans tend to be stricter, which might not suit businesses with lower credit scores. |

| Access to larger amounts - Term loans typically allow businesses to borrow larger amounts, which can be beneficial for significant investments or expenditures. | Long-term commitment - The repayment of term loans span over a long period which might not suit businesses wanting short-term solutions. |

| Building Credit - Regular and timely repayments can increase a business' credit score. | Early repayment penalties - Some lenders might charge a penalty for paying off the loan earlier than the agreed term. |

Unlike a traditional loan, where you receive a lump sum all at once, a line of credit allows you to borrow only what you need and pay interest on the amount you use. Think of it as a credit card for your business, but typically with lower interest rates and higher borrowing limits.

Common use cases: This flexibility makes it an excellent tool for managing cash flow, handling unexpected expenses, or addressing short-term funding needs.

Typical terms: You can get anywhere from $1,000 to $250,000, and the money is typically available in one to two days with a 6- to 18-month maturity. Most lenders charge a simple interest rate on the amount you draw with no prepayment penalty.

Minimum eligibility requirements: If you’ve been in business for more than half a year, are bringing in $50,000 or more in annual revenue, and have a credit score of 600 or higher, consider yourself a prime candidate.

The Small Business Administration (SBA) was created to assist small businesses through various educational and funding programs. SBA loans are unique because the SBA isn’t the lender. Rather, it guarantees a substantial portion of each loan, which reduces other lenders’ risk and makes them more willing to approve your request.

Common use cases: SBA loans are typically used for working capital or to purchase fixed assets such as equipment or real estate.

Typical terms: With an SBA loan, you can expect amounts from less than $50K up to $5M. Terms also cover a broad range, typically from 10-25 years. Expect the entire process to take 1-2 months.

Types of SBA loans: The SBA offers an array of loans to small business owners. Here are a few of the most popular options:

Minimum eligibility requirements: SBA loans have stringent credit requirements. You’ll need a minimum credit score of 650, at least two years in business, and a minimum of $8,000 in monthly revenue to be considered by an SBA lender.

Revenue-based financing borrows against your future earnings to secure the financing you need. Once you’ve been approved and the funds are advanced to your account, you’ll repay the funder a fixed daily amount via a withdrawal from your bank account. Some funders offer a merchant cash advance where you’ll have an agreed-upon percentage of your daily credit card deposits withheld for the lender.

Common use cases: Revenue-based financing can be used for any business expense. Common use cases include working capital, covering seasonal business needs, and expansion costs.

Typical terms: Revenue-based financing is known for speedy delivery. You can apply for anywhere from $5,000 to $500,000, and time to funds can be as short as 24 hours. A cash advance comes with a factor rate instead of an interest rate. Factor rates are expressed as a decimal number, such as 1.5. To calculate payback, multiply the total borrowed by the factor rate. For example, $10,000 borrowed x 1.5-factor rate = $15,000 total payback.

Minimum eligibility requirements: Qualifying for revenue-based financing is surprisingly simple because the nature and terms of the loan make the risk lower for a lender. Minimum credit score requirements start at 500. You’ll need a minimum monthly revenue of $10,000 and a minimum time in business of three months to qualify for a cash advance.

Equipment financing is a specialized form of financing used to purchase equipment. With amounts available up to $5 million, you can use them to buy any kind of equipment your business might need.

Common use cases: When most people hear the word “equipment,” they think of heavy equipment like backhoes, trucks, tractors, refrigerators, and trash compactors. But this type of financing can also be used for less obvious equipment, such as payment processing programs, solar panels, or accounting software for your office. The point is, if the purchase will equip your business for its needs, it probably meets the criteria.

Typical terms: Equipment financing is available from $5K-$5M with terms from one to 10 years. After submitting your application, you may see funds in as little as 24 hours. Interest rates start as low as 7.5%. The equipment you purchase will serve, at least in part, as collateral for the loan, so you may need less additional collateral than you would for other loan types. Some funders may require a down payment.

Minimum eligibility requirements: Qualifying for equipment financing is easier than many other types of loans. If your business has been running for a year or more, brings in $50,000 or more in annual revenue, and has a credit score of 520 or above, you should be sitting pretty. Some equipment financing companies will work with day-one startups. The lender will also evaluate the value and condition of the equipment as part of the approval process.

A commercial mortgage or commercial real estate loan is used to purchase or renovate commercial property such as an office building or warehouse.

Common use cases: A commercial mortgage can be used for just about any property need, whether that’s retail space, an office, a warehouse, or a restaurant. If you’ve been around for decades and want to expand, that’s no problem. Ready to purchase your first location? Perfect.

Typical terms: A commercial mortgage is similar to a home mortgage but with a few key differences. One, you’ll need to provide a down payment. There are typically no options for 100% financing. Two, the terms will be shorter, typically 10-25 years. Three, some commercial real estate loans come with a balloon payment at the end of the term, which is one large payment that pays off the remaining balance of the loan.

This financing option is an asset-based loan, so the amount and rate of your commercial mortgage will be based on your credit and the value of the property you’ll be using as collateral. You can expect amounts ranging from $250,000 to $5,000,000. The interest rates are usually on the lower end, starting at around 6.25%.

Minimum eligibility requirements: Qualifying for a commercial mortgage loan requires a clear plan for how you’ll put the cash to use. For example, if you’ll be making renovations to a property, your lender will want to know how you intend to do it and will also assess the after-repair value (or ARV) of the property.

Lenders will also look for:

You can plan on a lender requesting several property-related documents, including the purchase contract, property blueprints, market analysis for the property, project budget, scope of work, and assessment of the property’s existing condition.

Invoice factoring (sometimes called accounts receivable factoring) is tailor-made for when you need money but cashflow is tied up in outstanding invoices. With this type of financing, you’ll sell your outstanding invoices to a factoring company that will pay you a percentage of the invoice’s value upfront. The factoring company will collect the money from your customer when the invoice comes due and pay you back any remaining balance minus the factoring fee.

Common use cases: Invoice factoring is frequently used to boost cash flow, cover short-term expenses, and manage business seasonality.

Typical terms: The amounts vary, but you can often get up to 80% of your receivables. The money arrives in as little as 24 hours, and the loan term can last up to a year. As for the factoring fee, it starts as low as 3%.

Minimum eligibility requirements: To qualify for invoice factoring, your business must be B2B or B2G, have a minimum monthly revenue of $10K, and operate in the funder’s preferred industry.

The term “startup loan” can be a bit of a misnomer. While there are a handful of lenders who will work with day-one startups, it’s rare to find financing to start a brand-new business. However, there are still business loan options available for young startups with only a year or two in business. Common loan types for startups include revenue-based financing, invoice factoring, and equipment financing. The SBA also offers two programs for startups: SBA microloans and the Community Advantage program. These programs are meant to support underserved communities and will typically have less stringent qualifying criteria.

A business acquisition loan is used to buy an existing business or franchise.

Typically these loans will be structured as a term loan or line of credit used to purchase equipment, real estate, and intangible assets. SBA loans can also be used to acquire an existing business.

The loan terms will be specific to the loan type, lender, and specific acquisition costs. In general, expect lenders to look for a minimum credit score of 650, steady revenue, post-acquisition business plans and financial projections, and in many cases a significant cash contribution to the overall purchase. Lastly, lenders will want to know about any relevant experience to help you run the business successfully.

Short-term loans are repaid in a term of six months to three years. They can be structured as a term loan, revenue-based financing, a line of credit, or invoice factoring. Be aware that many term loans with short term lengths will require a daily or weekly payment similar to revenue-based financing.

Many entrepreneurs use short-term loans when they need quick solutions to pressing circumstances. So whether you need to pay for unexpected expenses, hire new staff, endure a sales slump, replace a broken piece of equipment, or take action on an exciting business opportunity, a short-term loan can be a solid option.

Of all the types of small business financing out there, the business credit card is the most user-friendly. If you’ve had a personal credit card, you know how it works. You can access amounts up to $500,000 with a business credit card, with interest rates from 8-24%. It’s not unusual to get a 0% introductory rate. There’s very little paperwork required compared to many loans, and the time to funds rarely exceeds 2 weeks.

This option is excellent for those who don’t feel ready to pursue a business loan or have been repeatedly turned down for them in the past. You’ll boost your working capital with fast access to cash, plus get the added benefits of leveraging a card rewards program and building your credit.

Business credit cards can be used for just about anything related to your operations. Whether you need to buy a new dump truck, add inventory, expand your office, take a client out to lunch, or hold an off-site staff event, this financing can be just the ticket.

Qualifying for a card isn’t difficult, which makes it a good match for those who are new to business. As long as you’ve got a credit score above 680 and have a decent business history, you should be in good shape.

Once you click submit on a loan application, the lender will use multiple factors to determine their response. These same factors also play a role in determining the loan’s terms and rates if you’re approved.

So how are approval decisions made? Here are 6 essential factors lenders use to evaluate your business credit and decide whether or not to open their wallet to you.

| Factors lenders use to evaluate your business credit |

| Personal credit – You can almost always expect lenders to be keenly interested in your business credit. But your business credit is inextricably linked to your personal credit, so it’s safe to assume they’ll also want to take a look at your personal financial health. This information typically includes your credit in use, credit history, payment history, and amounts owed. |

| Personal debt coverage – Again, your personal and business finances are related, so a lender will be interested in your personal debt coverage. If you’ve got a healthy state of affairs, expect lenders will consider you less of a risk and will be more keen to work with you. |

| Business debt coverage – There’s no problem with your business carrying debt. The question is whether your business can handle its debt obligations. To get a bead on your business debt coverage, a lender evaluates your cash flow and debt payments. |

| Personal debt utilization – If you’re carrying personal debt, you’re in good company. About 80% of Americans have some form of debt. What can set you apart from the masses is if you have credit available that you’re not currently using. To get this metric, a lender will divide your outstanding debt by the cumulative amount of your available revolving credit. |

| Business debt utilization – Lenders also care about the state of your business debt. Having debt isn’t a big deal. What matters is whether the amount of debt you’re carrying is appropriate compared to the size of your business and the industry you’re working in. This assessment comes from comparing your outstanding business debt to your assets and revenue. |

| Business revenue trend – Lenders are more motivated to work with you if your business is trending in the right direction, so they’ll want to ascertain what your average revenue growth will be over time. If yours lands at or above the average for your industry, you’re in great shape. If you fall below the average, plan on there being some possible challenges in your pursuit of financing. |

It’s often beneficial to speak with an expert who can evaluate your financing needs and guide you toward the best financing solutions. By doing your research, asking the right questions, and keeping your mind open, you’ll be setting yourself up for success.