The IRS announced an immediate moratorium on processing new Employee Retention Credit (ERC) claims on September 14, 2023. The moratorium will last through at least the end of the year in an effort to protect small business owners and taxpayers from scams and fraudulent claims.

As a small business owner, you may be wondering what this moratorium means for you and your business. Here’s everything we know and how you may still be able to apply for the ERC during the moratorium.

What we know.

We know that the IRS is continuing to process ERC applications that were received prior to the moratorium. However, processing times will be longer, the IRS advised in its Sept. 14, 2023 update — potentially going from a 90-day turnaround to 180 days or more. The agency has increasingly shifted its focus to review claims for compliance concerns and recently announced that thousands of ERC claims have been referred for audit. It is also working on hundreds of criminal cases on promoters and businesses filing suspicious claims.

Payouts for these previously filed claims will continue through the moratorium, but at a slower pace due to the more in-depth compliance reviews. This payout period will extend to 180 days from its previously standard processing goal of 90 days, according to the IRS. However, a payout may take even longer if its claim requires the IRS to further review or audit it.

The IRS is implementing this more scrutinous compliance review period to protect businesses from facing penalties or interest payments that stem from bad claims that aggressive marketers pushed.

For any business owners wanting to submit claims after September 14, 2023, while the IRS is not reviewing new applications until at least January 1, 2024, you can still submit an ERC claim during the moratorium.

Applying for the ERC.

Small business owners planning to submit an ERC claim after September 14, 2023 should ensure that their businesses are eligible for the tax credit prior to filling out the stringent application.

Pay qualified wages.

First, ensure that your business paid qualified wages to your employees. The definition of qualified wages varies depending on the amount of employees your business had on the payroll in tax years 2020 and 2021.

For tax year 2020, the IRS defined a small business as a business that averaged 100 or fewer full-time monthly employees in 2019. For tax year 2021, it expanded the definition to include businesses that averaged 500 or fewer full-time employees in 2019.

Larger employers can claim the ERC but only for wages and some healthcare costs paid to employees who did not work.

Small businesses can claim the credit for all employees, whether they worked during the period or not.

Government-mandated full or partial suspension.

Your business must have been impacted by either a government-mandated lockdown or decrease in revenue to be eligible for the ERC. You can qualify if your business was impacted by a full or partial suspension of operations due to a government COVID-19 order during any quarter (this includes restrictions on hours or capacity).

This area of eligibility criteria can be complex, so make sure to work with a vendor who is familiar with government orders, their impact, and the timeframe they were enacted.

Significant decline in gross receipts.

If your business experienced a “significant decline” in gross receipts as defined by the IRS, then it can be eligible for the ERC. For tax year 2020, a significant decline means that gross receipts for a quarter are less than 50% compared to the same period in 2019. For the first 3 quarters in 2021, a significant decline means quarterly receipts are less than 80% compared to the same period in 2019.

If your business did not see a 20% decline in gross receipts in the first 3 quarters of 2021 compared to 2019, you can also elect to use the immediately preceding quarter for comparison. This means that if a business’s Q2 of 2021 isn’t eligible compared to Q2 of 2019, it can instead use Q1 or 2021 and compare it to Q1 of 2019 to meet eligibility requirements.

Recovery startup business.

The ERC was amended in 2021 by The American Rescue Plan to let newer businesses gain access to the tax credit. A recovery startup business is defined as one that opened after February 15, 2020, and has annual gross receipts under $1 million. As long as you meet these two criteria and have one or more W2 employees, you don’t have to meet the other eligibility requirements. If your business qualifies as a “recovery startup business,” you can apply for the credit for Q3 and Q4 of 2021, and your business can receive a maximum of $50,000 in ERC per quarter.

If your business meets these requirements, then it may be eligible for the ERC. When applying, make sure that you have gathered thorough records proving wages paid, gross receipts, government orders, and other required documentation. Please note that businesses that improperly claim the ERC will be required to pay it back, potentially with penalties and interest.

Applying for the ERC during the moratorium period.

You should consult an accountant or tax professional prior to filling out any forms. They will help guide your business through this stringent and potentially confusing process.

You can apply for the ERC during the moratorium period through Lendio. We’ll help you identify what documents you need to claim the ERC. We’ve partnered with ERC and tax experts to aid you in the complex application process. They can help navigate you through tricky tax laws and avoid costly mistakes while calculating the full tax credit that you qualify for. After your application is complete, we’ll file your ERC claim with the IRS.

Please note that this process will be extended significantly due to the moratorium. While you will be able to submit your application to the IRS prior to January 1, 2024, it will not be reviewed until after that date (and with more stringent compliance review terms).

If you have additional questions regarding the ERC and/or the ERC moratorium period, check FAQ resources from the IRS and Lendio.

The Paycheck Protection Program (PPP) and Employee Retention Credit (ERC) were created to help businesses stay afloat during COVID-19. If the pandemic has had a negative impact on your small business, you might wonder whether you can take advantage of both of these programs. Keep reading to find out.

Key Points:

- The PPP was a forgivable loan. The ERC is a refundable tax credit.

- The PPP loan program is no longer available. The ERC can still be claimed retroactively.

- Businesses that received a PPP loan can still apply for the ERC.

- Employee wages used to receive PPP loan forgiveness cannot be used in your ERC claim.

What Is the Paycheck Protection Program?

Established by the CARES Act and administered by the U.S. Small Business Administration (SBA), the PPP offered loans of up to $10 million to small businesses that faced financial hardship as a result of COVID-19.

As long as you qualified, you could have received a loan for up to 2.5 times of your average monthly payroll costs. The loan can be forgiven completely if you file a forgiveness application and show you used the proceeds to cover rent, utilities, payroll costs, and other qualifying expenses.

What is the Employee Retention Credit?

The ERC is a refundable payroll tax credit for qualified wages paid to employees in 2020 and 2021. It was created under the CARES Act and administered by the Internal Revenue Service (IRS) to encourage businesses to retain their employees during the pandemic.

You may qualify if you experienced partial shutdowns due to government orders or significant declines in quarterly gross receipts due to COVID-19. If you meet certain eligibility criteria, you can claim as much as $5,000 per employee in 2020 and as much as $21,000 per employee in 2021.

Differences Between PPP and ERC

While the PPP and ERC were both designed to support businesses that have struggled financially as a result of the pandemic, there are several noteworthy differences between these two programs.

| PPP | ERC | |

| Type of funding | Forgivable loan | Tax credit |

| Funding time | 10 days | 3-6 months |

| Cost | Any funds you didn’t receive forgiveness for | None |

| Amount | 2.5x the average monthly payroll costs | Up to $26,000 per W-2 employee |

| Still available | No | Yes |

Type of Funding

The PPP offers a forgivable loan. If you used the funds on payroll, rent, and other qualifying expenses, you wouldn’t have to pay it back. In the event you used part of the loan for non-qualifying reasons, that portion won’t be forgiven. You’ll have to repay it with a fixed interest rate of 1% over a period of either two or five years. The ERC, on the other hand, is a tax credit you won’t have to repay.

Funding Time

If you qualified for the PPP loan, you would have received the funds via direct deposit, usually within ten days of approval. The ERC, however, will be distributed to you after you file Form 941-X and the IRS has reviewed your claim. The IRS will process the credit you’re owed and send you a check. The IRS can take anywhere from 3-6 months+ to process your credit. We highly recommend reserving your place in line now by filing the necessary paperwork with the IRS.

Cost

It was free to apply for the PPP loan. You would only incur a cost if you don’t use the loan proceeds on qualifying expenses and must pay it back. There’s no governmental fee to receive the ERC either. It’s a tax credit that you can receive by filing an amended payroll tax form for each of the tax periods that you qualify for. The only expense you may face will be service charges if you ask an accountant or tax professional to assist in preparing and filing your tax forms.

Eligibility

The eligibility requirements for the ERCwere updated in 2021.

2020 qualifications:

- Qualifying wages of up to 100 full-time employees

- A decrease in gross revenue of at least 50% compared to the corresponding quarter in 2019

- Or either a full or partial suspension of business operations created by a government mandate

2021 qualifications:

- Qualifying wages of up to 500 full-time employees

- A decrease in gross revenue of at least 20% compared to the corresponding quarter in 2019

- Or either a full or partial suspension of business operations created by a government mandate

PPP loan requirements included:

- A small business with 500 employees or less

- The business was operational before February 15, 2020

- For second-draw loans, the business must have used up previous loan funds and demonstrate a 25% or more reduction in gross revenue.

Can You Get Employee Retention Credit and PPP?

Initially, a business that received a PPP loan was not eligible for the ERC. Thanks to the Consolidated Appropriations Act of 2021, however, a business that received a PPP loan may also apply for the ERC retroactively back to 2020.

The caveat, however, is that you can’t use the wages that qualify you for PPP loan forgiveness to determine your ERC amount. You’ll need documentation that proves you’re not “double dipping” and using both programs to cover the same wages.

Let’s say you used your PPP funds to pay for $50,000 in wages and you expect to qualify for forgiveness. In this scenario, you can’t use those wages that have been forgiven to calculate your ERC.

How to Apply for PPP and ERC

You can no longer apply for a PPP loan, but you can still fill out an application for the ERC. If you’d like to claim the ERC, you can do so on Form 941-X. Don’t hesitate to consult a tax professional for assistance.

How to Maximize the PPP and ERC

There are a few ways you can maximize the benefits of both the PPP and ERC, including:

- If you included non-payroll costs in your PPP loan forgiveness application, show you used a minimum of 60% of the total loan on payroll. This way you’ll be eligible for full forgiveness.

- In the event you don’t list qualifying non-payroll costs on your application, you must prove that you used 100% of the loan amount on payroll to get your loan completely forgiven.

- Provide detailed explanations to help the tax professional you work with understand exactly how the government orders impacted your business. This will help them maximize the amount you qualify for.

- Don’t forget to separate the total payroll costs you used for the PPP loan from the total payroll costs you list with the ERC. This can help you avoid getting denied for using the same payroll costs for both programs.

- Use a tax professional vs. filing yourself. Though you may pay money, these professionals often understand the program much better than you ever could on your own. As a result, they often can help you qualify for more money than you would on your own. They also will help ensure that you file the credit correctly so that in the event of an audit all of your i’s are dotted and t’s are crossed.

Reap the Benefits of the PPP and ERC

If you previously applied for PPP, there’s no reason not to apply for the ERC. By doing so, you can mitigate the financial losses you may have incurred during the pandemic and set your business up for future success.

Have you heard of the Employee Retention Credit (ERC)? For business owners who endured the COVID-19 pandemic and the economic roller-coaster it brought, the ERC was meant to provide financial relief and keep their workforce employed. Now, even though the economic impacts of the pandemic have subsided, business owners like you can still take advantage of this tax credit. To find out if you qualify and how the Employee Retention Credit works, read our answers to the Employee Retention Credit FAQs below.

General overview questions

What is the Employee Retention Credit (ERC)?

The ERC is a tax credit. This means, when applied, the ERC will reduce the total amount of taxes a business owes to the Internal Revenue Service (IRS). The ERC was part of the Coronavirus Aid, Relief, and Economic Security Act (CARES Act) which was passed in March 2020 by the U.S. Congress. It was intended to lessen the pandemic's economic impact on businesses and encourage them to retain employees as much as possible.

The ERC is a fully refundable tax credit. This means, that if your business’ ERC is greater than your federal employment taxes, it could create a negative federal tax liability for a business and result in a tax refund. At the very least, it could lower the amount of taxes your business pays—at most, you could receive a refund check.

Am I eligible for the Employee Retention Credit?

To be eligible to receive the Employee Retention Credit, you must meet the following criteria:

- Your business is a private sector or tax-exempt organization that carried out business in 2020 and/or 2021.

- Your business paid qualified wages to employees in 2020 and/or 2021.

- Your business experienced hardship in one of the following areas:

- You were forced to suspend your business’s operations, including limiting commerce travel or group meetings, fully or partially due to COVID-19 government orders, or

- You experienced a significant decline in gross receipts beginning in the first quarter of 2020.

Since you’ll be required to prove your business’s eligibility, knowing the definitions of a partial business suspension or a significant decline in gross receipts is critical.

A partial business suspension is one in which total employee hours fall below 10% of the business’ typical total employee hours. An example of a partially suspended business would be a restaurant that could no longer welcome dine-in customers but continued to provide carry-out or delivery services. For more details on full vs. partial suspension of business, click here.

A significant decline in gross receipts is when a business’s gross receipts started dropping in the first quarter of 2020 to 50% or less of the gross receipts of the business in the first quarter of 2019. For more details on the definition of a decline in gross receipts, visit the IRS page on the topic.

Learn More: Employee Retention Tax Credit: is your small business eligible?

What exceptions or restrictions should I be aware of in the ERC?

A few other exceptions exist to the guidelines above. For example:

- Self-employed individuals may not claim the credit based on their earnings, but they can for wages paid to any employees they may have.

- Certain tribal government organizations or entities might be considered eligible.

- Businesses that received Paycheck Protection Program (PPP) loans from the government can claim the tax credit, but not for wages that were paid using a PPP loan.

- Businesses that receive tax credits under the Families First Coronavirus Response Act (FFCRA) employer-paid leave requirements can’t count qualified leave wages in their ERC calculations.

- Businesses cannot count wages they’ve attributed to the R&D tax credit in their ERC calculation.

For more information on these and other exceptions, visit the IRS page on this topic.

How is the Employee Retention Credit determined?

A business’ ERC amount is determined based on its qualified employee wages and the year in which those wages were paid. Here’s how it works:

- For wages paid from March 13 to December 31, 2020, the tax credit is worth 50% of qualified employee wages. The highest amount that would be considered qualified employee wages for any one employee is $10,000 for the entire year. Following that math, the maximum credit a business can get per qualified employee is $5,000 (i.e., 50% of $10,000).

- For wages paid in 2021, the tax credit is higher: 70% of qualified employee wages. The highest amount of qualified wages paid that would be considered for any one employee is also larger: $10,000 per month. Therefore, the maximum credit a business can receive for 2021 is considerably larger than for 2020. Important note: businesses can claim the credit for the first three quarters of 2021 only, not the fourth.

It’s worth noting here that qualified health plan expenses—defined as amounts paid or incurred by the business that are allocable to employees’ qualified wages to provide and maintain a group health plan, but only as they are excluded from employees’ gross income—are also factored into these wage figures.

To get the full details on how the ERC is determined, visit the IRS page on the topic.

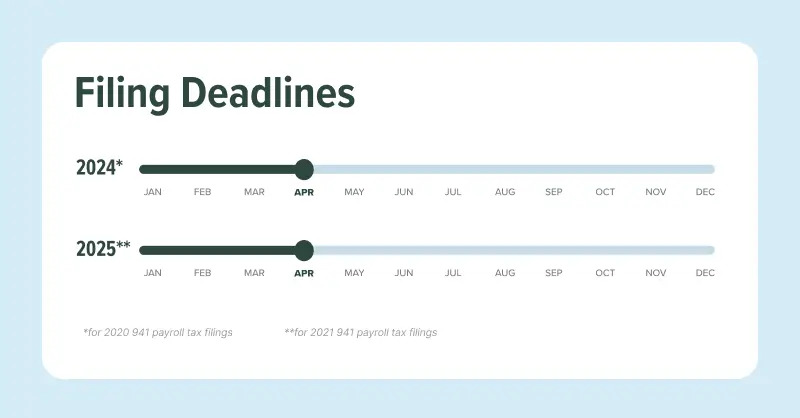

Can I still take advantage of the ERC?

Yes. If you want to take advantage of the 2020 ERC, you can apply until April 15, 2024. Likewise, the 2022 ERC will not lapse until April 15, 2025.

How do I apply for the ERC?

To apply for the Employee Retention Credit, you should file an amended Form 941X as part of your quarterly federal tax return for any 2020 or 2021 quarter in which your business was eligible for the ERC.

Qualification questions

What is a recovery startup business?

Originally, the ERC was only available to established small businesses that experienced significant declines in revenues or operational shutdowns due to COVID-19. The American Rescue Plan (ARP) amended the ERC eligibility requirements to extend the credit to newer businesses. These are known as “recovery startup businesses.”

To claim the ERC as a recovery startup business, your operation must meet the following requirements:

- Started doing business after February 15, 2020

- Averaged less than $1 million in annual gross receipts during the three-year period ending before the quarter

- Not be otherwise eligible for the ERC through a decline in gross receipts or an operational shutdown

Recovery startup businesses with one or more W-2 employees on the payroll can claim the ERC and receive up to $50,000 in total credits per quarter for the third and fourth quarters of 2021.

Learn More: How to qualify as a recovery startup business for ERC in 2023

What qualifies as a government shutdown for Employee Retention Credit?

Businesses that experienced a full or partial suspension of their operations due to an order from a governmental authority may be eligible for the ERC. If a business faced a direct order to fully suspend their business, then they qualify under the ERC. If a business or portion of a business was deemed essential, but was limited in hours and service capacity, they may still qualify as a partial suspension depending on the level of reduction in capacity or reduction in hours.

Learn More: Navigating the Employee Retention Credit (ERC) shutdown test

What are qualified wages for the ERC?

Qualified wages include full or part-time W-2 employee salaries as well as certain health plan expenses. For "small employers" with less than 100 employees in 2020 and less than 500 employees in 2021, all wages paid to your workers qualify. For "large employers" who fall above those thresholds, only wages paid to employees who weren't working qualify.

Learn More: Qualified wages for the Employee Retention Credit

Are tips qualified wages for Employee Retention Credit?

In Notice 2021-49, the IRS confirmed that the definition of qualified wages for the ERC includes cash tips received by an employee in a calendar month that amount to $20 or more, assuming all other requirements to treat them as qualified wages are satisfied.

Cash tips include tips employees receive directly from customers, tips from other employees under tip-sharing arrangements, and tips charged to credit and debit cards distributed to employees.

Learn More: Tips and the Employee Retention Credit

Are owner’s wages considered qualified wages?

The IRS has stated that wages paid to employees related to their employers aren’t qualified wages for the ERC. When the employer is a corporation, related employees are those who have one of the following relationships with a majority owner:

- A child or a descendant of a child

- A brother, sister, stepbrother, or stepsister

- The father or mother, or an ancestor of either

- A stepfather or stepmother

- A niece or nephew

- An aunt or uncle

- A son-in-law, daughter-in-law, father-in-law, mother-in-law, brother-in-law, or sister-in-law

In Notice 2021-49, the IRS clarified further that constructive ownership and familial attribution rules apply when determining related parties. As a result, ancestors, whole or half-siblings, and lineal descendants of majority owners are also considered majority owners for purposes of the ERC.

The notice concludes that majority owners with living relatives are, therefore, effectively related to majority owners, and their wages aren’t qualified for the ERC. In other words, majority owner wages can't be qualified wages unless they have no living ancestors, siblings, or descendants.

Minority owner wages can qualify for the ERC, assuming they own less than 50% of the company after accounting for the attribution laws.

Learn More: Are owner's wages considered qualified wages?

Can I still qualify for the ERC if my business was profitable?

You can still claim the ERC if your business generated a profit during the 2020 and 2021 tax years. However, you must have experienced a substantial decline in gross receipts or suspended operations due to a government order to be eligible unless you’re a recovery startup business.

An employer experienced a significant decline in gross receipts for 2020 if its quarterly revenues dropped below 50% of the revenues earned in the same quarter in 2019. It remains eligible for the ERC until the end of 2020 or the 2020 quarter after gross receipts reach 80% of the gross receipts for the same quarter in 2019.

For 2021, an employer has a significant decline in gross receipts for each quarter in which gross receipts were less than 80% of the same quarter in 2019.

Can I still qualify for the ERC if I didn’t pay income taxes?

The ERC is a refundable payroll tax credit designed to offset employment taxes. As a result, the status of your income tax return generally doesn’t affect your ability to qualify for it. If you didn’t pay income taxes for 2020 or 2021 because your business earned a net loss for the tax year, you can still claim the ERC for any eligible quarters.

Because it’s a refundable credit, not paying payroll taxes doesn’t prevent you from claiming the ERC, either. If the ERC reduces your liability below or further below zero, you’ll receive a refund from the IRS.

Do nonprofits qualify for the ERC?

Nonprofits can qualify for the ERC. Like for-profit businesses, they generally must show that they experienced a significant decline in gross receipts or suspended their operations due to a government order to be eligible.

Tax and logistics questions

Is the Employee Retention Credit taxable income?

No, the ERC is not taxable income. It’s a refundable payroll tax credit that directly offsets your payroll taxes. In many cases, the credit will exceed your total payroll tax liability, resulting in a refund. Regardless, you should not include the ERC amount in your gross income for tax purposes.

However, an IRS notice confirms that the ERC is subject to deduction disallowance rules. That prevents you from taking a deduction on your income tax return for wages used to claim the ERC. If you claim the ERC, you must reduce your wages expense for the qualifying period by the credit amount, effectively increasing your taxable income.

For example, say you paid $80,000 in qualified wages during 2020. In 2023, you retroactively claim a $30,000 ERC for the year, resulting in a refund. You would amend your 2020 income tax return and reduce your wages expense to $50,000, increasing your taxable income for that year. However, the refund wouldn’t be taxable.

Learn More: Is the Employee Retention Credit taxable income?

Is there a deadline to claim the Employee Retention Credit?

Because the period to earn the ERC is passed, businesses must now claim the credit retroactively by filing a Form 941-X for each eligible quarter. The deadline to file 941-X is three years from the filing date of the original Form 941.

Fortunately, the IRS considers all Forms 941 for a calendar year to be filed on April 15 of the subsequent year, even if you filed it before that date. As a result, the deadline to claim the ERC for quarters in 2020 is April 15, 2024. For quarters in 2021, the deadline is April 15, 2025.

Are ERC and ERTC the same thing?

ERC and ERTC are abbreviations for the same thing. ERC is short for Employee Retention Credit, while ERTC is an abbreviation for Employee Retention Tax Credit. They’re both references to the refundable payroll tax credit implemented by the CARES Act to reward businesses for continuing to pay employees’ wages during COVID-19.

How will I receive my Employee Retention Credit refund?

You should receive a separate check in the mail from the IRS for each quarter in which you claimed the ERC and generated a refund.

Does the Employee Retention Credit have to be paid back?

Unlike funds from the Paycheck Protection Program (PPP), the ERC is not a loan. It’s a refundable tax credit, and you don’t have to pay it back. There’s no need to apply for forgiveness, either. If it generates a refund, it’s automatically yours to keep.

Does the IRS audit ERC credits?

The IRS has already begun auditing ERC claims. The passage of the American Rescue Plan in 2021 extended its window to review the ERC from three years after filing to five. There’s an additional focus on the tax credit due to elevated fraud risks.

Though you may not be subject to an ERC audit, it’s best to assume that you will and prepare accordingly. Consider consulting a Certified Public Accountant (CPA) or another tax professional for help.

When should I expect my ERC refund?

On average, you can expect your refund within three to six months of filing. However, some taxpayers may wait a year or more to receive their checks, depending on their filing date and credit size.

Unfortunately, there’s no way to know for sure. The IRS is still experiencing delays in processing claims due to a backlog caused by its shutdowns during the pandemic.

Can I still apply for the ERC during the moratorium?

You can still apply for the ERC during the moratorium period, however, please note that your application will not be reviewed until at least January 1, 2024.

How do I avoid ERC scams?

A common ERC scam charges an upfront fee to see what you qualify for through the ERC. Legitimate vendors won't charge you just to see if you qualify. Other red flags include promising that everyone can qualify, promising more money than other filers and not doing thorough research, calculations and due diligence.

The Employment Retention Credit is a potential financial benefit that no business owner can afford to pass up. However, to ensure that your business qualifies for this tax credit and secures the full credit amount it’s entitled to, we strongly recommend working with ERC experts, such as Lendio's ERC partners.

If you had employees on the payroll during the COVID-19 pandemic, you could claim up to $26,000 in tax credits for each one, using the Employee Retention Credit (ERC). However, your credit amount depends on the qualified wages paid to your workers.

To help you determine how much you can claim, let’s explore what counts as qualified wages for the Employee Retention Credit.

What are Qualified Wages For the Employee Retention Credit?

The Employee Retention Credit is a refundable payroll tax credit designed to provide relief to businesses that paid their employees despite facing economic strain from the COVID-19 pandemic.

You must meet a hardship requirement to claim the credit unless you’re a recovery startup business. That means experiencing economic strain in the form of a decline in your gross receipts or a suspension of your operations.

If you’re eligible, you can claim the ERC for a portion of the qualified wages you paid each employee in 2020 and 2021. More specifically, you can claim 50% of their first $10,000 in 2020 and 70% of their first $10,000 in each quarter of 2021, excluding the fourth. That’s a total of $26,000 each.

In addition to employee salaries, qualified wages include certain health plan expenses you incurred to maintain their group health plan, plus whatever costs they covered through pre-tax salary reduction contributions.

There may also be limitations on which employees qualify for the credit. If you meet the criteria to be a “large employer,” you can claim only the credit for the qualified wages you paid to those not providing services in 2020 and 2021. Here’s how it works:

If you had less than 100 employees on average in 2019, then the wages you paid to all your employees are qualified for 2020. If you averaged more than 100 employees, then only the wages you paid to employees who weren’t working are qualified that year.

For the 2021 tax year, the threshold increased to 500 employees. Wages paid to all your workers are qualified, if you averaged less than 500 in 2019. Otherwise, only non-working employee wages are qualified for 2021.

Examples of Qualified Wages

Like many aspects of the Employee Retention Credit, the qualified wages rules are complicated and challenging to grasp in the abstract. To help you understand how they work, let’s look at a few practical examples.

Qualified Wages for Small Employers

Say you own a cleaning business that’s had ten employees on the payroll since 2015. Each receives a $35,000 salary and costs you $5,000 in qualified health plan expenses annually. Three stopped providing services between September 31, 2020, and March 31, 2021, but you kept them all on the payroll.

In 2020 and the first three quarters of 2021, you have a significant enough decline in gross receipts to be eligible for the ERC. And because you only had ten employees on average in 2019, you’re considered a small employer in both years.

As a result, you can claim the ERC for the qualified wages you paid to all your employees. Fortunately, with $35,000 in salaries and $5,000 in health plan expenses, each earns $10,000 in eligible compensation per quarter, just enough to maximize your credit.

In 2020, you can claim 50% of the first $10,000 for ten employees, which is $50,000. In 2021, you can claim 70% of the first $10,000 for ten employees each quarter. That’s $21,000 for each employee in 2021, which is $210,000.

Qualified Wages For Large Employers

This time, say you own a cleaning business that’s grown large enough to operate across the state, with a whopping 750 employees on the payroll. However, 250 of your workers provided no services between September 31, 2020, and June 30, 2020.

For simplicity's sake, we’ll assume that they each have $40,000 in qualified compensation per year, and you experience a decline in gross receipts that makes you eligible for the ERC in all periods.

Because you averaged 750 employees in 2019, you’re considered a large employer for 2020 and 2021. As a result, you can only consider qualified wages paid to workers not providing services when calculating your tax credit amount.

In 2020, you can claim 50% of the first $10,000 paid to the 250 workers that stopped working on September 31. All would have earned $10,000 apiece in that final quarter of 2020, so you could claim $1.25 million in tax credits that year.

In 2021, you can claim 70% of the first $10,000 paid to those same workers in each of the two quarters they weren’t providing services. As a result, you can claim $14,000 for 250 employees that year, which is $3.5 million.

Can Owner Wages Qualify For the ERC?

If you structure your business as a corporation, you can pay yourself an annual salary. That raises the question of whether or not owner wages qualify for the Employee Retention Credit.

Unfortunately, the answer is probably not. It isn’t strictly forbidden, but it’s unlikely that you’ll meet the requirements to be able to do so. If you’re a majority owner with more than 50% of the stock, you’d need to have no living ancestors, siblings, or descendants.

If you’re a minority owner with less than 50% of the stock, your wages should be eligible if you don’t share ownership with your relatives. That all seems a little arbitrary, so let’s explore the reasoning.

The Internal Revenue Service (IRS) ruled that wages you pay to employees related to majority owners of your company don’t qualify for the ERC. A majority owner of a corporation owns at least 50% of the company’s stock. Their relatives are people with whom they have one of the following relationships:

- Child or a descendant of a child

- Brother, sister, stepbrother, or stepsister

- Father or mother, or an ancestor of either

- Stepfather or stepmother

- Niece or nephew

- Aunt or uncle

- Son-in-law, daughter-in-law, father-in-law, mother-in-law, brother-in-law, or sister-in-law

The IRS has also ruled that “constructive ownership and familial attribution” rules apply to this situation. These state that people own the stock of their living ancestors, siblings, and descendants, by extension.

As a result, through slightly circular reasoning, any majority owner with at least one of these relatives is technically related to someone with majority ownership by extension. Therefore, their wages are ineligible for the ERC.

Example of Ineligible Majority Owner Wages

Say that you own 100% of Corporation A. You also have a big family, including a daughter. Because she has a qualifying relationship with you, a majority owner, the IRS also considers her a majority owner of Corporation A by extension.

Unfortunately, as her father, you have a qualifying relationship with her, too. And because she’s a majority owner, any wages paid to you are ineligible for the ERC.

Example of Ineligible Minority Owner Wages

This time, say you own 34% of Corporation A. However, you share ownership of the company with your two siblings. Each owns half the remaining shares, with 33% ownership each.

Because you’re all siblings, the IRS treats you all as if you own each other’s shares for the sake of the ERC. That means each of you effectively owns 100% of the company due to family attribution rules, making you all majority owners by extension.

As a result, each of you has a qualifying relationship with a majority owner, and none of the wages paid to you qualify for the ERC.

Apply For the Employee Retention Credit

Eligible employers who paid qualified wages to their employees during 2020 and 2021 can claim thousands of dollars through the ERC. While the period to earn the credit has passed, you still have time to claim them retroactively before the deadline.

Learn More: If you have more questions about the Employee Retention Credit or qualified wages, our other resources may be able to help:

The Employee Retention Credit is among the most lucrative tax credits available to small business owners in 2023. However, it can be pretty tough to navigate, especially the credit calculation.

Let’s discuss how to calculate the Employee Retention Credit in detail, walk through a few practical examples, and explore some background information to help put everything into context.

How Does the Employee Retention Credit Work?

The Employee Retention Credit (ERC) is a refundable payroll tax credit designed to lessen the financial strain on small business owners who kept their employees on the payroll during the COVID-19 pandemic.

The credit’s main eligibility requirement is an economic hardship test. To clear it, you must demonstrate that your business experienced a sufficient decline in gross receipts or suspended a more than nominal portion of its operations due to a government order.

Determining whether you satisfy one of those requirements is a fairly involved process. But if you do, then you should be able to claim a tax credit for a percentage of the wages your business paid in 2020 and 2021.

How to Calculate the Employee Retention Credit

Under the regular ERC rules, you can claim a credit for 50% of the first $10,000 in qualified wagesyou paid each employee during 2020. In 2021, you can claim 70% of each employee’s first $10,000 in qualified wages per quarter. That means you can claim up to $26,000 in refundable tax credits per employee between both years.

To calculate your ERC amount, you must determine which wages qualify under the credit. That primarily depends on the number of full-time employees you had on the payroll during the 2019 calendar year.

If you had less than 100 employees on average during 2019, then you can treat the wages paid to all your employees as qualified in 2020. If you exceeded that threshold, only the wages you paid to employees not providing services qualify for the ERC that year.

In 2021, the maximum number of employees for the determination increased to 500, but you still base it on your 2019 staff count. In other words, all your wages are qualified in 2021 if you had less than 500 people on the payroll in 2019. Otherwise, only the wages paid to your inactive employees qualify for the credit.

When calculating the qualified wages paid to your employees, you can also add your group health plan expenses. That includes your portion of the costs as the employer and any pre-tax salary reduction contributions from your employees.

How to Calculate the ERC as a Recovery Startup Business

If you started your business during the pandemic, you probably won’t be able to qualify for the ERC through the regular method. After all, most of the default qualification requirements involve analyzing a business’ activities in 2019.

However, you may still be able to qualify for the ERC as a recovery startup business. These are organizations that started doing business after February 15, 2020, average less than $1 million in annual gross receipts, and fail both versions of the economic hardship test in at least the third quarter of 2021.

If you meet these requirements, you can claim the ERC for 70% of the first $10,000 in qualified wages paid to each employee in the third and fourth quarters of 2021. In fact, only recovery startups can claim the credit for wages paid after September 30, 2021.

However, they also have a $50,000 quarterly limit. As a result, you can claim only $100,000 in total for those two quarters as a recovery startup.

ERC Calculation Examples

Now that we’ve covered how to calculate the Employee Retention Credit in theory, let’s walk through a few examples to demonstrate how it works in practice.

Small Employer in 2020

Say you own a restaurant with ten employees on the payroll in 2019 and 2020, each earning a $40,000 annual salary. You continued to pay them all throughout 2020, even though five employees didn’t work after March because you shut down dine-in services to comply with federal social distancing mandates.

Let’s assume that qualifies as a partial suspension of your operation, making you eligible to claim the ERC that year. Because you had less than 100 employees on average in 2019, the wages you paid to all your employees were qualified.

For 2020, you can claim a credit for 50% of each employee’s first $10,000 in qualified wages that year. All your employees reached that limit, so you can claim $5,000 for each one. Because you have 10 eligible employees, you can take a $50,000 ERC that year.

Large Employer in 2021

Say you own a nonprofit organization with 600 employees on the payroll in 2019, 2020, and 2021. Each of them had a base annual salary of $50,000. However, 200 workers stopped providing services from January 1, 2021, to June 30, 2021, during which you paid them only half their usual salaries.

Because you averaged more than 500 employees in 2019, only the wages you paid to those 200 employees who weren’t working are qualified. Let’s also assume you saw a decline in gross receipts during those months that was sufficient for the hardship test.

You can claim 70% of the first $10,000 in qualified wages paid to each non-working employee in the first two quarters of 2021. With 200 employees, that gives you $1.4 million each quarter, resulting in a $2.8 million total ERC.

Recovery Startup Business

Finally, say you start a landscaping business with 10 employees on May 1, 2020. It has less than $1 million in average annual gross receipts and fails the economic hardship test in all periods, making it a recovery startup business.

You pay each of your employees $80,000 in wages yearly. As a recovery startup business owner, you can claim a tax credit for 70% of their first $10,000 in qualified wages for the third and fourth quarters of 2021.

Because all of your workers reached the $10,000 limit each quarter, you can claim $7,000 for each one. With 10 employees, you should be able to take a $70,000 ERC each quarter and a $140,000 credit for the year.

However, your organization is a recovery startup business, so your credit amount can’t exceed $50,000 in a single quarter. As a result, you can claim only $100,000 for the 2021 calendar year.

Apply For the Employee Retention Credit

As these calculations demonstrate, the Employee Retention Credit is an incredibly lucrative opportunity for business owners. If you qualify, you could reduce your federal tax liability by thousands of dollars, potentially resulting in a refund.

It’s too late to earn the ERC, but you still have time to claim the credit retroactively by filing Form 941-X with the Internal Revenue Service for each eligible quarter. The deadline is April 15, 2024, for quarters in 2020 and April 15, 2025, for quarters in 2021.

If you’d like help determining whether you qualify for the ERC, let our convenient application tool walk you through everything. Once you confirm your eligibility, it can also streamline the filing process for you. Give it a try today.

Learn More: If you want to know more about the Employee Retention Credit before you move forward, our other resources may be able to help:

The Employee Retention Credit (ERC) is one of the most lucrative tax credits for small business owners. Fortunately, if you had employees on the payroll during the COVID-19 pandemic, you can still claim it retroactively.

To help you understand how you might qualify, let’s review how the ERC works and walk through some practical examples of eligible businesses.

How Does the Employee Retention Credit Work?

The Coronavirus Aid, Relief, and Economic Security (CARES) Act created the Employee Retention Credit in 2020. Its goal was to provide financial relief to small businesses and encourage them to retain their employees.

The ERC works as a refundable tax credit. You can deduct it from your payroll tax liability and pocket any excess amounts. As a result, it’s even more beneficial than a tax deduction, which can only reduce your taxable income.

To be eligible for the ERC during 2020 or 2021, you must pass the following three tests during the period for which you want to claim the credit:

- Your business was a private sector or tax-exempt organization.

- Your business paid qualified wages to employees.

- Your business experienced hardship in one of the following areas:

- You were forced to suspend your business’ operations, including limiting commerce travel or group meetings, fully or partially due to COVID-19 government orders, or

- You experienced a sufficient decline in gross receipts.

Businesses that pass these tests can claim a tax credit for a portion of each employee’s qualified wages. The 2020 limit is 50% of their first $10,000 that year. The 2021 limit is 70% of their first $10,000 per quarter until September 31, 2021, unless you’re a recovery startup business. That’s a maximum credit of $26,000 per employee.

While you can no longer earn the ERC, you still have time to claim it by filing Form 941-X for each eligible quarter. For quarters in 2020, you have until April 15, 2024. For quarters in 2021, the deadline is April 15, 2025.

What are Qualified Wages?

The definition of qualified wages under the ERC is surprisingly complex and deserves additional clarification. Most notably, your average number of employees in 2019 determines which wages qualify for the credit.

If you had 100 or fewer employees on average during 2019, wages paid to all employees in 2020 are qualified. If you averaged more than 100 employees during 2019, only wages paid to employees who weren’t providing services are qualified.

In 2021, the threshold increased to 500 employees. In other words, if you averaged 500 employees or less in 2019, all wages in each 2021 quarter are qualified. If you averaged more than 500 employees in 2019, only those paid to workers not providing services qualify in 2021 quarters.

What is a Suspension Due to a Government Order?

You must also understand what constitutes a full or partial suspension of operations due to a government order. Let’s look at the suspension of operations aspect first. To pass this test, “more than a nominal portion” of your operations must shut down.

For an aspect of your business to be more than nominal in a given quarter of 2020 or 2021, it must meet one of the following tests in the corresponding 2019 quarter:

- Its gross receipts constituted 10% or more of your total gross receipts.

- Hours worked by the portion’s employees were 10% or more of all hours worked.

Finally, a governmental order refers to official proclamations or decrees from the federal, state, or local government that "limit your commerce, travel, or group meetings due to COVID-19.”

What is a Sufficient Decline in Gross Receipts?

Finally, let’s expand upon what constitutes an eligible decline in gross receipts. Unfortunately, the rules are a little different between 2020 and 2021.

In 2020, you can show a sufficient decline in gross receipts for only one continuous period. It starts in the first calendar quarter that your receipts fall below 50% of receipts in the same quarter of 2019. It ends in the quarter after they first rise to 80% of 2019 receipts.

In 2021, you can test for an eligible decline in gross receipts on a quarterly basis. You can claim the ERC for each quarter that your gross receipts are below 80% of receipts for the same quarter in 2019, even if they’re discontinuous.

Employee Retention Credit Examples

As you can see, the ERC eligibility requirements are complicated. To help you understand them, let’s look at some in-depth examples of eligible employers, explain why they qualify for the ERC, and calculate their credit amounts.

Example 1: Partial Suspension

A restaurant had 20 employees on the payroll in 2019, 2020, and 2021. It paid everyone a $40,000 salary each year, even though half of the workers provided no services between April 1, 2020, and December 31, 2020.

The restaurant closed dine-in services to comply with federal social distancing mandates on March 15, 2020, but remained open for take-out. The government order ended on March 30, 2021. Throughout 2019, dine-in services generated 65% of the restaurant’s gross receipts.

As a for-profit business that operated in 2020 and 2021, the restaurant passed the first test for the ERC in both years. Because it continued to pay its workers during the pandemic, it also cleared the second.

Dine-in services generated 65% of the restaurant’s gross receipts in 2019, making it a more than nominal portion of operations. Because the social distancing mandate came from the federal government, it was a qualified government order. That means the restaurant passed the hardship test from March 15, 2020, until March 30, 2021.

Now we can calculate the restaurant's ERC amount. Because it averaged less than 100 employees in 2019, all wages were qualified in 2020. Since everyone had a $40,000 salary, each earned more than $10,000 during the eligible period.

With the ERC limit being 50% of their first $10,000, the restaurant's 2020 ERC is $5,000 for 20 employees, which equals $100,000.

Now, let’s calculate the amount for 2021. Since the restaurant averaged less than 500 employees in 2019, all employee wages qualified in 2021. However, the 2021 ERC limit is 70% of the first $10,000 per eligible quarter. Because the government order ended on March 31, 2021, only the first quarter is eligible in 2021.

With $40,000 salaries, each worker earned $10,000 per quarter, so they all reached the cap during the first quarter of 2021. As a result, the restaurant could claim 70% of $10,000 for 20 workers for that year, giving it a $140,000 credit.

Ultimately, the restaurant could claim a $240,000 ERC.

Example 2: Significant Decline in Gross Receipts

A 501(c)(3) charitable organization had 550 employees on the payroll from 2019 to 2021. Each employee had a $60,000 annual salary for all three years.

The charity had 250 employees stop providing services from April 1, 2020, to the end of the year. It put 125 of them back to work on January 1, 2021. The rest resumed working on March 31, 2021.

The organization received the following donations during that three-year period, which were its only gross receipts:

| Year | Quarter 1 | Quarter 2 | Quarter 3 | Quarter 4 | Total |

| 2019 | $25,000,000 | $25,000,000 | $25,000,000 | $25,000,000 | $100,000,000 |

| 2020 | $15,000,000 | $12,000,000 | $15,500,000 | $17,500,000 | $60,000,000 |

| 2021 | $18,500,000 | $21,500,000 | $19,500,000 | $22,500,000 | $85,000,000 |

As a nonprofit organization that continued to operate during 2020 and 2021, this charity satisfied the first requirement for both years. Because it continued to pay wages to its full-time employees in 2020 and 2021, it also met the second one.

The charity also passed the hardship test in both years. It experienced a significant decline in gross receipts starting in the second quarter of 2020. $12 million in gross receipts is less than 50% of the $25 million received in the equivalent quarter of 2019.

The decline continued through 2020 because gross receipts in the remaining quarters never exceeded 80% of the gross receipts in the corresponding 2019 quarters.

In 2021, the charity saw a decline in gross receipts in the first and third quarters. $18.5 million and $19.5 million are less than 80% of the $25 million received each quarter in 2019.

Now we can calculate the ERC amount, starting with 2020. Because the charity averaged more than 100 employees in 2019, only wages paid to workers not providing services were qualified.

The 2020 eligible period was the second quarter through the end of the year. During that time, 250 workers were not providing services. With $60,000 annual salaries, they all earned $10,000 in that period. As a result, the charity could claim $5,000 for each of them, equaling a $1.25 million ERC in 2020.

In 2021, the first and third quarters were eligible for the ERC. However, 125 workers resumed working on January 1, 2021, and everyone else did so by March 31, 2021. Because the charity averaged more than 500 employees in 2019, only wages paid to those not providing services were qualified for the year.

As a result, the charity can claim the ERC for only 70% of the first $10,000 paid to the 125 employees not working in the first quarter. Since they all earned more than $10,000 during that time, the charity’s ERC for the year would be 70% of $10,000 for 125 employees, which equals $875,000.

That puts the charity’s total ERC at $2,125,000.

Apply For the Employee Retention Credit

As you can see, the ERC can be incredibly lucrative. If you qualify but fail to claim your tax credit, you could leave thousands of dollars on the table. Fortunately, it’s not too late to apply, and our easy-to-use application tool can guide you through the process from start to finish. Give it a try today.

Learn More: If you have further questions about the ERC due to unusual business circumstances, our other ERC resources may be able to help:

Setting up a business isn’t an easy feat. Even more difficult is finding and maintaining funding and cash flow to support day-to-day operations.

According to a study by the U.S. Bank, as quoted in this Business Insider article, 82% of businesses fail mainly because of poor cash management. Cash is the lifeblood of your business, and no matter what your profits are, your actual cash will be the thing that keeps your business up and running.

Perhaps you can find funding through personal borrowings from friends or family, but not every entrepreneur has the luxury or opportunity to do the same. At this point, most businesses can only turn to business credit to secure funding from lenders and banks.

The catch?

Lenders and banks generally consider your business credit before offering help—and for good reason. This article will dive into everything about building business credit in 30 days.

What is Business Credit, and Why is It Important?

Think of business credit as your personal credit score.

A better business credit score gives a company more access to funds from lenders and banks because of a good track record in availing and repaying debt.

Like your own personal credit score range companies with good business credit scores can access more cash with lower interest rates than companies with bad credit scores. The latter group are definite red flags to lenders, as they are the ones who are most likely to repay loans late or just not pay at all.

How to Build Business Credit

Building business credit is a process, not an end goal. Good business credit is built upon years and years of good repayment track records.

If you’re looking into building your business credit, it should start from the moment you create your business plan. Here are steps on how to start building your business credit:

1. Identify the Right Structure For Your Business

To build a business credit, it is important to identify the kind of structure you would want for your business. There are three primary business structures you may want to consider:

- Sole proprietorship

- Partnership

- LLC/Corporation

The disadvantage of being a sole proprietor or a partnership in determining your business credit is that business credit is closely tied to the personal credit standing of the owner or partners.

Why? Because, in a sole proprietorship and partnership, owners and partners are personally liable for all the gains and losses of the business—including its debts. Therefore, when a sole owner has terrible credit standing, creditors are less likely to extend loans for your business, as well.

On the other hand, businesses established as corporations create a separate legal entity from its managers and directors, so the company's credit standing is separated from its owners and directors.

“There is a term called ‘corporate veil’ for businesses established as corporations,” says Andrew Pierce, Founder of Real Estate Holding Company. “This corporate veil protects the management and the shareholders wherein they are only liable to the extent of their shareholdings, and their identities and financial standing does not legally affect the organization.”

There are some exceptions to the corporate veil, such as a personal guarantee for a business loan or if personal and business accounts are mixed.

2. Maintain a Separate Bank Account For Your Business

Business owners should establish that the company is independent of the owners when trying to build good business credit.

Creditors will look at your business' financial records, including the inflow and outflow of cash, and having a separate bank account solely for your operations will make the job easy for you and your creditors.

The better and the easier they see that your financial standing is positive and you have good cash flow management, the more trustworthy your credit standing looks and the more access you’ll have to funds.

Jim Pendergast, senior vice-president at altLINE Sobanco, states, “Even for sole proprietors, it is discouraged to keep personal and business finances in one account. Some credit investigators look at things at face value, and mixing personal and business accounts is a red flag for blurring the lines between personal and business liability.”

In addition, mixing your personal and business accounts puts you in danger of mishandling your cash, spending personal finances on business expenses, and vice versa, and eventually puts you in a pinch regarding future legal documentation, money trail, and managing business tax computations.

3. Establish Trade Lines

The most popular form of trade line to build your business credit is net-30s, which can also be called supplier or trade credits.

The idea behind it is simple: businesses negotiate with their vendors to give them a 30-day term for payment upon delivery of goods or performance of service. When these vendors report to one of the three credit bureaus—Dun and Bradstreet, Experian, or Equifax—this will help start businesses and build business credit.

“Net-30 terms aren’t only beneficial for buyers, but for suppliers as well,” says Gerald Lombardo, CEO of cauZmik. “Offering flexible terms, together with discounts for early payments, like 2/10 net 30 terms, gives a strong incentive for customers and also helps expand your brand and market,”

The catch, though, is that signing up for a net-30 account requires filling out an application form and paying a small sign-up fee. Nonetheless, net-30 is similar to vendors extending you a 30-day interest-free loan, which will significantly help improve business credit when paid on time.

4. Keep Your Bills Paid in Full and On Time

This remains true for personal and business credit integrity. Still, many people don’t realize how vital it is to regularly pay your bills and dues on time and in full. It prevents you from having bad business credit and saves you costs from interest and surcharges from late or nonpayment of account.

“While many factors go into your credit score, your payment history has the biggest impact on it, accounting for 30% to 40% of the total score in the formula,” says Anthony Martin, Founder and CEO of Choice Mutual. “Paying on time and in full will not necessarily magically bump up your scores, but leaving them unpaid and delinquent will negatively affect your record.”

5. Keep Your Personal Credit Score in Check

Unfortunate as it may seem, yes, your personal credit score affects your business credit, especially for sole proprietors and small businesses. Vice versa, bad business credit can also negatively affect your personal credit.

You can keep your personal credit score in check by making timely and full payments and increasing your credit utilization rate. However, there are still remedies in which you can separate personal and business credit:

- Get a separate business credit card to use for all business expenses.

- Incorporate your business.

- Create a separate receipt for your business.

- Carefully separate personal and business transactions.

6. Regularly Check Business Credit Agencies

Credit bureaus are only as good as the data being fed to them, so it is essential for businesses to regularly check with the credit bureaus for any discrepancies and misreporting that may have been incorrectly attributed to calculating their business credit score.

According to Experian, checking business credit reports will give you the following:

- Financial information

- Credit score and risk factors

- Banking, trade, and collection history

- Liens, judgment, and bankruptcies

While this data can help those extending credit, this will also help businesses monitor credit standing and contest incorrect credit report information through a Data Dispute form, which can be settled in as little as 30 days or longer for complex cases.

Personal credit bureaus are different from business credit bureaus. For business credit bureaus in the United States, you can refer to Dun & Bradstreet, Experian, and Equifax as the three major providers of business credit reports.

According to Stephan Baldwin, Founder of Assisted Living, “Many people find communicating with credit bureaus daunting. However, to avoid erroneous records reflected on your account—bankruptcies, foreclosures, or late payments—which negatively impact your credit score, it is best to make sure to reach out to credit bureaus and regularly check your credit score and related information therein.”

Wrapping Up

Not all debts are bad, especially when these debts or loans are leveraged to the advantage of the business. Building your company’s business credit in 30 days starts from the moment you create a business plan, followed by availing of trade credits, getting separate credit cards, and making sure these accounts are paid on time.

Building business credit is not a short-term process, but rather an accumulation of good business practices that would make you a credible and trustworthy organization to be extended access to more funding.

If you qualify for the Employee Retention Credit (ERC), you could receive thousands of dollars in refundable tax credits for each employee on your payroll during the COVID-19 pandemic. Fortunately, there’s still time for you to claim those funds.

Let’s break down the qualification requirements to help you determine whether your small business is eligible.

What are the ERC Eligibility Requirements?

The Employee Retention Credit eligibility requirements include three primary tests. Regular employers that pass all of them can potentially claim the tax credit for 2020 and the first three quarters of 2021. Here’s what you should know about how they work.

Eligible Organization

The first ERC eligibility requirement is the most straightforward and easiest to clear. You must be an employer that operated a trade, business, or tax-exempt organization during 2020 or 2021.

If you're a small business owner running a company that’s been around since before the pandemic, then you generally don’t have to worry about this test. It primarily prevents governmental entities from claiming the ERC.

Pay Qualified Wages

The second ERC eligibility requirement is where things start to get more complicated. To pass this test, you must have paid qualified wages to your employees. That sounds simple, but the definition of qualified wages varies depending on how many employees your business had on the payroll in 2019.

If your average number of employees in 2019 was below certain thresholds, then the wages you paid to all employees in 2020 and 2021 can qualify for the ERC. If it was above those thresholds, only the wages you paid to workers not providing services are eligible.

For 2020, the threshold is 100 employees. For 2021, the cutoff increased to 500 employees. Note that you should calculate your average number of employees in 2019 on an annual basis, not a quarterly one.

For example, say you had an average of 150 employees on the payroll in 2019. That puts you above the threshold for 2020, and only wages paid to workers not providing services would qualify for the ERC that year. However, you’re below the threshold for 2021, so wages paid to all employees would qualify that year.

Experience Economic Hardship

The third ERC eligibility requirement is the most complex and usually the one that ultimately determines whether or not you can claim the tax credit. To pass this test, you must have experienced economic hardship due to the COVID-19 pandemic in one of the following ways:

- You were forced to suspend your business’ operations, including limiting commerce travel or group meetings, fully or partially due to COVID-19 government orders, or

- You experienced a significant decline in gross receipts.

Let’s take a closer look at what each of these tests mean.

Suspension of Operations

There are two parts to this test that you must understand. Let’s start with the government order aspect since it’s the most straightforward. It refers to mandates from federal, state, or local regulators that limit your commerce, travel, or group meetings due to COVID-19.

This does not include unofficial recommendations from public servants or self-imposed restrictions. If you’re not subject to a specific government order, you can’t satisfy the hardship requirement through this method.

The second aspect of this test is to have a “full or partial suspension of operations,” which is a bit more complicated. To clear it, you must shut down a “more than nominal portion” of your business.

Upon the initial passage of the Coronavirus Aid, Relief, and Economic Security (CARES) Act, there was a lot of controversy over what this term meant. However, the Internal Revenue Service (IRS) eventually confirmed that a portion of your business must pass one of the following tests to be considered nominal:

- Its gross receipts equaled 10% or more of your total gross receipts

- Its employees worked 10% or more of your workforce’s total hours worked

Once again, these requirements are based on the 2019 calendar year. For example, say you own a restaurant that offers dine-in and takeout services. In 2019, dine-in services generated between 60% and 75% of your annual gross receipts.

Because that aspect of your operation generated more than 10% of your total gross receipts in 2019, it constitutes a more-than-nominal portion of your business. If you stopped offering dine-in services to comply with a government order during 2020 or 2021, you’d be eligible to claim the ERC in that period.

Sufficient Decline in Gross Receipts

As an alternative to showing a suspension of operations, you can prove that you experienced economic hardship through a sufficient decline in gross receipts. This is another complex test, and the rules differ between the 2020 and 2021 calendar years.

In 2020, you can have a decline in gross receipts for only one continuous period. It can cover multiple quarters, but they must be uninterrupted. For example, you couldn’t qualify in the first and third quarters without the second.

An eligible decline begins in the first quarter that your gross receipts fall below 50% of receipts in the same 2019 quarter. It ends in the quarter after your receipts rise above 80% of receipts in the corresponding 2019 quarter.

Meanwhile, in 2021, you can test for a sufficient decline on a quarterly basis. Each one passes the test when its gross receipts are below 80% of gross receipts in the same 2019 quarter. For example, say your business had the following gross receipts:

| Year | Quarter 1 | Quarter 2 | Quarter 3 | Quarter 4 |

| 2019 | $100,000 | $100,000 | $100,000 | $100,000 |

| 2020 | $45,000 | $65,000 | $82,000 | $84,000 |

| 2021 | $78,000 | $81,000 | $75,000 | $85,000 |

In 2020, an eligible decline in gross receipts starts in the second quarter—as $45,000 is less than 50% of $100,000—and continues through quarter three. Quarter four is the only ineligible one that year, as it’s the first quarter after receipts rise above 80% of 2019 numbers.

In 2021, any quarter with receipts below 80% of the receipts in the same quarter from 2019 passes this test. As a result, you’d qualify for the ERC in the first and third quarters, but the second and fourth would be ineligible.

Recovery Startup Businesses

The default ERC eligibility requirements generally apply to organizations established before the COVID-19 pandemic. That’s why so many of them involve comparing 2020 and 2021 numbers to those from corresponding periods in 2019.

However, the American Rescue Plan (ARP) was enacted in 2021 to extend ERC benefits to certain businesses that began their operations in the middle of the pandemic. These companies are known as recovery startup businesses.

If you’re a recovery startup business, the eligibility requirements for the ERC are substantially different than those for regular employers. Here are the requirements your operation must meet to claim the ERC as a recovery startup for a given quarter:

- Start doing business after February 15, 2020

- Have at least one W-2 employee on the payroll

- Average less than $1 million in annual gross receipts during the three-year period ending in the tax year before the quarter

An additional eligibility requirement applies to the third quarter. Namely, you can't pass the decline in gross receipts or suspension of operations tests. If you do, you must claim the credit for that quarter as a regular employer, not a recovery startup business.

To clarify, filing as a recovery startup business in either of these quarters will not prevent you from doing so in the earlier quarters as a regular employer.

Recovery Startup Business ERC Example

Like the regular ERC qualification rules, the recovery startup eligibility requirements are complicated. Let’s look at an example to help you understand how they work.

Say you opened a digital marketing agency on June 1, 2020. You have five full-time employees on the payroll taking home $50,000 salaries, and your new business generated $400,000 in gross receipts by the end of the year.

You started doing business after February 15, 2020, and had multiple W-2 employees on the payroll, so you meet the first two requirements for a recovery startup business. All that’s left is to confirm that you meet the $1-million gross receipts test.

Since you weren’t in business before the 2020 tax year, that’s the only year you must consider here. But because you were only open for part of the year, you have to annualize your numbers.

To do so, divide the $400,000 received in 2020 by the number of months you were open that year, then multiply the result by 12. Since you started doing business on June 1, divide $400,000 by seven and multiply it by 12 to get $685,714. Fortunately, that’s well below the $1 million threshold.

Assuming you don’t pass the decline in gross receipts or suspension of operations tests for the third quarter of the year, you can file as a recovery startup for the third and fourth quarters of 2021.

Apply for the Employee Retention Credit

The ERC is a refundable payroll tax credit. That means you can subtract it directly from your annual payroll tax liability, and if there’s any left, you can take it to the bank. That makes the ERC significantly more impactful than a tax deduction and too valuable an opportunity to miss.

If you think you satisfy the Employee Retention Credit qualification requirements, there’s still time to claim your funds by filing IRS Form 941-X for each eligible quarter. The deadline is April 15, 2024, for quarters in 2020 and April 15, 2025, for those in 2021.

Fortunately, our ERC application guide can walk you through confirming your eligibility, filing the necessary forms, and securing your funds. Don’t wait–get started today.

Learn More: If you have additional questions about your business’ ERC eligibility due to unusual circumstances, our other resources may be able to help: