Many accounting classes start with the “lemonade stand” model of business management. You want to sell lemonade, so you work through the process of buying supplies and selling products.

However, running a business becomes more complicated when you leave the private sector to start a nonprofit. Instead of selling lemonade, you’re now trying to collect funds so others can have lemonade. Or you’re selling lemonade to donate funds.

Nonprofits have their own accounting challenges and requirements, with specific documentation and legal guidelines for what they can accept and what they can do with their money. However, despite their complexity, the basic principles of accounting shine through. Nonprofits with clear records and organized financial categories have better odds of succeeding and bringing positive influence to whatever cause they support.

Learn more about nonprofit bookkeeping and its accounting process to better position your charity to apply for grants, win over big-money donors, and drive change.

What is nonprofit accounting?

Nonprofit accounting—also referred to as fund accounting—is a unique form of bookkeeping designed specifically for nonprofit organizations. Unlike profit-driven businesses, nonprofits aren't primarily focused on increasing wealth for shareholders. Instead, they're driven by a mission to serve a specific societal need, and their accounting practices reflect this difference.

Nonprofit accounting involves tracking donations, grants, and other forms of income, as well as ensuring these funds are used appropriately and efficiently towards the organization's mission. This form of accounting places a significant emphasis on transparency, accountability, and stewardship, making sure every dollar is accounted for and used responsibly.

Moreover, nonprofit accounting is regulated by a distinct set of legal and financial standards that require detailed reporting and compliance. Understanding these requirements is integral to the management and operation of any successful nonprofit organization.

How is nonprofit accounting different from for-profit accounting?

There are several key differences between nonprofit and for-profit accounting, primarily stemming from the distinct goals and operational structures of these two types of organizations. For-profit businesses aim to generate profits and increase shareholder value, whereas nonprofits exist to serve a specific social purpose and are tasked with demonstrating how they use their funds to further this mission.

In for-profit accounting, the focus is on revenues, expenses, and the resulting profits, with financial statements like the balance sheet and income statement detailing the company's financial health. On the other hand, nonprofit accounting centers around tracking and reporting on the use of funds, where financial statements such as the statement of financial position and statement of activities provide a transparent view of the organization's financial situation.

Moreover, nonprofits are held to a high degree of fiscal accountability and stewardship, requiring them to thoroughly document all income and expenditures. They are also subject to specific regulatory and reporting requirements, including filings like the IRS Form 990, which are not applicable to for-profit entities. These differences underscore the importance of understanding and effectively managing nonprofit accounting—it's not just about keeping the books, but ensuring the organization is taking the right steps towards fulfilling its mission.

How to navigate nonprofit accounting.

Navigating the world of nonprofit accounting can seem like a daunting task, with its unique regulatory guidelines, strict requirements for transparency, and the constant need for fiscal accountability. However, with the right knowledge and tools, it can be effectively managed to uphold your organization's mission and sustain its operations with confidence and ease.

Identify cash flow sources.

As your nonprofit grows, you may have multiple cash flow sources. Each source of income requires different levels of effort and spending.

However, you’re responsible for tracking every dollar your nonprofit receives—and accounting for what you do with it. A few common examples of income sources for nonprofits include:

- Cash donations from benefactors and supporters

- Local, state, and federal grants

- Legacy gifts from donors who passed away

- Fundraising partnerships from local businesses

- Ticket sales to events and your donor-facing locations

For example, an art museum or animal rehabilitation group can sell tickets to the general public. The art museum might also sell tickets for fundraising galas and summer camp activities for kids. Meanwhile, the animal rehabilitation center can fundraise through events like goat yoga, with the proceeds supporting the food and medication needed for their animals.

Not every nonprofit has a donor-facing experience, however. Many homeless shelters and child advocacy groups rely instead on grants and donations from benefactors and businesses. While every nonprofit is different, most charities rely on individual donations to stay open. It’s estimated that over 80% of income for nonprofits comes from individual giving.

Whenever you propose a new fundraising opportunity or activity, consider which category the development efforts fall under. This may determine how you can spend the money and the target ROI expected for your efforts.

Quantify in-kind donations.

Beyond money, there’s a whole different kind of donation that nonprofit organizations need to track and build into their budgets. In-kind donations refer to gifts that aren’t monetary but have a monetary value. A few examples of in-kind donations include:

- A local restaurant donating a $100 gift card for part of a charity auction

- A marketing agency offering its services pro bono on a monthly retainer basis

- Local high school students collecting soup cans or coats from their peers to donate

- A few retired volunteers spending a couple of hours each week filing paperwork and performing other administrative tasks

Each of these in-kind donations is specific and has value, but how can you track them in your accounting systems—and why do you need to?

There are 2 main reasons why you need to track your in-kind donations. First, you’re required to for tax reporting purposes. In some cases, businesses and individuals can claim charitable donations on their taxes to receive deductions. The in-kind donation that a business provides might be part of its core values, but the company also wants a tax break.

Next, you need to identify the sources of income and value to your business. For example, if a volunteer helps with administrative tasks for an average of 15 hours per week, they provide real monetary value to your business. If they suddenly stopped volunteering, how much would it cost to hire a temporary worker or part-time employee for those 15 hours of work? An administrative assistant earning $15 per hour for 15 hours per week over a year (50 weeks) earns $11,250. Just because that volunteer doesn’t give you cash doesn’t mean they aren’t one of your largest donors.

Any person who donates time to your organization provides value and income. By tracking volunteer hours and activities (whether they offer highly skilled IT support or low-skilled help), you can estimate the cost savings to your organization.

Once you quantify your in-kind donations, set up a system to accept and process them. You’ll need to report on your in-kind support and volunteer hours at the end of each year, both in your annual report and in your budgeting meetings. Each donor also needs to receive a thank you letter that explicitly details what they gave and its monetary value. This record is used for their tax purposes.

Choose between cash- vs. accrual-based accounting.

As you develop the financial policies and procedures of your nonprofit, you need to consider whether you will use cash- vs. accrual-based accounting. Every business has to choose between these 2 accounting models—and keep in mind that it isn’t easy to switch from one to the other.

Cash-based accounting means that you only record income when you receive it and expenses when you pay for them. For example, you would record a donation from a benefactor once their check hits your account.

The main benefit of cash-based accounting is that you always know what kind of money you have. There is less risk of overspending because you aren’t focused on future income that may or may not come. However, this format can make it hard to forecast upcoming expenses and future donations.

With accrual-based accounting, you record any income or expenses when they’re earned, not received. For example, if you call a plumber to fix your organization’s toilet, you will record the cost of the repair when the plumber completes the job—even if you don’t pay the invoice for another few weeks.

Accrual-based accounting is viewed as more comprehensive than cash-based models. Nonprofits can understand more clearly the money they currently owe and will soon receive.

So which model is best? In the nonprofit sector, most organizations use accrual-based systems. Yes, this process is more complex and time-consuming, but the system is believed to be more accurate and comprehensive.

In fact, some nonprofit types are legally required to use accrual-based reporting—for example, if you receive grants or have paid staff. This promotes financial transparency to organizational partners.

If you have a cash-based accounting system, you will need to create a disclaimer in your financial reports and year-end statements illustrating this and potentially explaining why.

Track the ROI of your fundraising efforts.

Nonprofit accounting doesn’t just provide transparency to donors and governing bodies—it also shines a spotlight on the efforts the organization works toward.

Over the past few years, there have been increased calls for nonprofits to serve as good stewards of the money they receive. Charity Navigator ranks nonprofits based on their transparency and their financial stewardship. If an organization mishandles money (e.g., through overinflated executive pay, overspending, and donation mismanagement), then donors are discouraged from contributing.

Every nonprofit has its own operating costs and financial challenges. However, the team at Charity Watch estimates that a responsible expense ratio is 35% or less. For every $100 you bring into your organization, it is reasonable to spend $35 to solicit the donation. Other nonprofits shoot for a 25% expense ratio or a 4:1 ROI.

Through your accounting processes, you should be able to track how much it costs each year to bring in donations to your organization. These expenses range from hiring a full-time donor coordinator to hosting fundraising events and galas each season.

Additionally, you should be able to track what percent of your total donations actually support your nonprofit’s mission—which reflects your stewardship and respect for donors.

These analyses can be performed on both a macro and micro level. While maintaining a high ROI for your fundraising efforts is important for your charity’s reputation, you may decide to prioritize some development efforts over others if they bring in higher donation amounts or cost less to implement. (If you come from the private sector, this is similar to adjusting your products to promote items with a higher gross margin.)

Know important nonprofit accounting documents.

Nonprofit accounting requires meticulous maintenance and management of numerous financial documents for transparency and compliance purposes. Here are several key documents that are integral to nonprofit accounting:

- Nonprofit budget - This vital financial document outlines the organization's expected income and expenses for a certain period of time, typically a fiscal year. It serves as a roadmap for spending and revenue generation, playing a crucial role in guiding strategic decision-making and ensuring financial sustainability. Some things to remember when creating your budget include identifying your cash flow sources and quantifying in-kind donations.

- Statement of financial position (SOP) - This document is the nonprofit equivalent of a balance sheet. It provides a snapshot of the organization's financial condition at a specific point in time, summarizing its assets, liabilities, and net assets. The assets are listed from most to least liquid—what could be spent the fastest—while the liabilities are listed in order of obligation. This document provides a high-level overview of the company’s finances and priorities.

- Statement of activities - Analogous to an income statement in for-profit businesses, this document details revenue, expenses, and changes in net assets over a given period. It provides a clear picture of how funds are being sourced and utilized.

- Statement of cash flows - This is a detailed record of the cash inflows and outflows experienced by the organization during a particular period, illustrating the liquidity and financial viability of the organization.

- Statement of functional expenses - This statement provides a breakdown of expenses by both nature (what was purchased) and function (why it was purchased). It is unique to nonprofits and helps demonstrate how funds are allocated between program services and supporting activities.

- IRS Form 990 - This is an annual reporting return that certain federally tax-exempt organizations must file with the IRS. It provides information on the filing organization's mission, programs, and finances.

Understanding and accurately maintaining these financial documents is crucial in nonprofit accounting, as they provide a comprehensive and transparent record of the organization's financial activities, ensuring compliance with regulatory requirements and fostering trust with donors, members, and the public.

Develop a clear operations budget.

Accounting serves two major purposes in business: looking back on past performance and planning for future income. While your nonprofit may use financial documents to report on the past quarter, you can also use this visibility to create fundraising goals and budget for future expenses.

For example, a nonprofit can review its operational expenses to predict how much it costs to run annually. The organization can then use this information to make cuts or take on new projects depending on whether they have a cash deficit or surplus.

On top of tracking operating expenses (OPEX), nonprofits often set goals to help the community and make an impact. These efforts come with their own version of cost of goods sold (COGS).

For example, if a nonprofit offers a mobile shower, shave, and haircut service to homeless individuals, the COGS required to offer that service might include towels, soap, the cost of hiring barbers, and care package items to give to those in need. A nonprofit that has a goal to offer 3,000 showers over the course of the year will have to budget for those items.

The challenge for nonprofits: the funds for these operating expenses aren’t always guaranteed. Development teams will review the operational goals for the year and set fundraising goals to bring in more money so the organization can expand its efforts.

While both the fundraising team and operations department might be on the same page during the year, both parties should meet quarterly to review their current finances to see if operations can get scaled up—or if they need to be pulled back. This is how a nonprofit balances its budget.

Set up a reporting system.

The world of finance and accounting can be stressful, especially for those who worry about recording every receipt and tracking numbers accurately—and there is some truth to this concern. If you let your sales receipts and donations pile up without recording them, then your accounting process will become beleaguered. You even risk creating inaccurate documents and making decisions based on outdated information because your books aren’t organized.

The easiest way to prevent this backlog of unrecorded transactions is to set up a system where you can record income and expenses quickly. Invest in software tools that let you categorize costs and even auto-categorize repeating charges.

Train your team members to reconcile their expenses immediately and report any new donations. By spending a few minutes each day reviewing your transactions, you can keep up with your finances and prevent the dreaded backlog.

Prepare to file taxes and submit annual reports.

All of your financial documents and accounting processes will help your nonprofit at the end of the year. Nonprofits still need to file taxes, even if they are tax-exempt (tax-exempt doesn’t mean you can skip filing, just that you won’t have to pay taxes).

One of the most important tax documents for a nonprofit is Form 990. This form covers the nonprofit’s mission, programs, and finances. There are multiple types of Form 990, with fields that vary based on your organization’s size and operations. For example:

- Nonprofits with less than $50,000 in gross receipts can fill out Form 990-N, an e-Postcard.

- Nonprofits with more than $50,000 in gross receipts can fill out Form 990 or 990-EZ.

- Private foundations fill out form 990-PF.

Some organizations are exempt from filling out Form 990. These include faith-based groups, government cooperatives, and subsidiaries of other nonprofits.

Along with your taxes, your organization may need to submit an annual report to the state or federal government. These reports are typically made public each year by nonprofits and live on their websites for potential donors to access.

Use your nonprofit accounting system as a marketing tool.

Nonprofits are constantly fighting to win over new donors and prove they deserve support. As your accounting system falls into place, promote it within your development materials to show donors that you care about the money they give.

- Highlight your target ROI and the steps you are taking to improve it.

- Share your impact goals for the year and the operating budget you need to hit them.

- Explain what your general fund does and why funding expenses like toilet paper and rent are important.

- Showcase your stewardship and transparency to prove you respect their donations.

You can’t talk about these aspects of your organization without clear proof. This proof comes in the form of financial documents and statistics highlighting your accounting efforts. You work so hard to serve your community and handle their money responsibly—it’s time you started bragging about it.

Create processes to manage your nonprofit accounts.

Establishing streamlined processes to manage your nonprofit accounts is essential for efficient and transparent operations. Begin by implementing a system that caters to your unique needs and ensures accurate record keeping. Regularly review your accounts to ensure compliance with regulations and maintain up-to-date records.

Opt for cloud-based accounting software tailored for nonprofits, as they can automate many tasks, improve accuracy, and save time. This includes generating financial reports, tracking donations, managing expenses, and even budgeting.

Develop an internal policy outlining how financial transactions should be handled, including approval processes for expenditures and proper documentation for all transactions. This can play a vital role in preventing misappropriation of funds and ensuring financial integrity.

Training staff and volunteers on the importance of financial management is crucial. Everyone involved should understand their role in maintaining the financial health of the organization. Regular training sessions can keep everyone up-to-date on best practices and changes in financial regulations.

By creating solid processes, you can manage your nonprofit accounts effectively, maintaining the trust of your donors, and ensuring the longevity of your organization.

Nonprofit accounting best practices.

Implementing best practices in nonprofit accounting can enhance your organization's operational efficiency, financial transparency, and overall accountability. Here are some key strategies to consider:

- Implement robust internal controls - Internal controls are essential for safeguarding your organization's assets, ensuring the accuracy of your financial records, and preventing fraud. These can include separation of financial responsibilities to prevent a single person from handling all financial tasks, regular audits, and comprehensive financial policies and procedures.

- Use nonprofit accounting software - Specialized nonprofit accounting software can simplify complex fund accounting, making it easier to track and report on different sources of income, categorize expenses, and ensure compliance with nonprofit-specific standards and regulations.

- Regularly review financial reports - Regular reviews of your financial statements can help identify trends, foresee potential issues, and make informed, strategic decisions. This includes closely examining your statement of financial position, statement of activities, statement of cash flows, and statement of functional expenses.

- Maintain a reserve fund - Having a reserve fund can provide financial stability in times of unexpected expenses or drops in funding. It also demonstrates to donors and stakeholders that your organization is financially responsible and prepared for unforeseen circumstances.

- Provide transparency - Nonprofits are held to high standards of accountability. Regularly share your financial reports with board members, stakeholders, and the public to maintain trust and demonstrate responsible stewardship of funds.

- Invest in financial training for non-finance staff - Everyone in your organization should have a basic understanding of your nonprofit's finances. Providing training can help staff understand the importance of their role in maintaining financial integrity and how their day-to-day actions impact the organization's overall financial health.

- Stay current with regulations - As regulations and standards can update, it's important to regularly check in with the regulatory bodies or consult with an accounting professional to avoid non-compliance.

- Plan overhead expenses carefully - Nonprofits, like any other organization, will have overhead costs, such as administrative expenses, salaries, utilities, and office supplies. It's important to budget and monitor these expenses carefully as they play a direct role in your organization's sustainability and efficiency. A well-planned overhead expense strategy ensures that the maximum amount of funding goes directly to your cause, enhancing trust among your donors and stakeholders.

- Reference your budget often - Regularly referring back to your budget is key to maintaining financial discipline and ensuring the organization stays on track with its financial goals. This practice encourages proactive adjustments to spending habits and allows for timely reallocation of resources, if necessary, to meet the changing needs and priorities of the organization.

By following these best practices, your nonprofit can maintain strong financial health and continue effectively serving your mission.

Implementing best practices in nonprofit accounting can enhance your organization's operational efficiency, financial transparency, and overall accountability. Here are some key strategies to consider:

- Implement robust internal controls - Internal controls are essential for safeguarding your organization's assets, ensuring the accuracy of your financial records, and preventing fraud. These can include separation of financial responsibilities to prevent a single person from handling all financial tasks, regular audits, and comprehensive financial policies and procedures.

- Use nonprofit accounting software - Specialized nonprofit accounting software can simplify complex fund accounting, making it easier to track and report on different sources of income, categorize expenses, and ensure compliance with nonprofit-specific standards and regulations.

- Regularly review financial reports - Regular reviews of your financial statements can help identify trends, foresee potential issues, and make informed, strategic decisions. This includes closely examining your statement of financial position, statement of activities, statement of cash flows, and statement of functional expenses.

- Maintain a reserve fund - Having a reserve fund can provide financial stability in times of unexpected expenses or drops in funding. It also demonstrates to donors and stakeholders that your organization is financially responsible and prepared for unforeseen circumstances.

- Provide transparency - Nonprofits are held to high standards of accountability. Regularly share your financial reports with board members, stakeholders, and the public to maintain trust and demonstrate responsible stewardship of funds.

- Invest in financial training for non-finance staff - Everyone in your organization should have a basic understanding of your nonprofit's finances. Providing training can help staff understand the importance of their role in maintaining financial integrity and how their day-to-day actions impact the organization's overall financial health.

- Stay current with regulations - As regulations and standards can update, it's important to regularly check in with the regulatory bodies or consult with an accounting professional to avoid non-compliance.

- Plan overhead expenses carefully - Nonprofits, like any other organization, will have overhead costs, such as administrative expenses, salaries, utilities, and office supplies. It's important to budget and monitor these expenses carefully as they play a direct role in your organization's sustainability and efficiency. A well-planned overhead expense strategy ensures that the maximum amount of funding goes directly to your cause, enhancing trust among your donors and stakeholders.

- Reference your budget often - Regularly referring back to your budget is key to maintaining financial discipline and ensuring the organization stays on track with its financial goals. This practice encourages proactive adjustments to spending habits and allows for timely reallocation of resources, if necessary, to meet the changing needs and priorities of the organization.

By following these best practices, your nonprofit can maintain strong financial health and continue effectively serving your mission.

Effective accounting is the backbone of any nonprofit's success. It not only ensures financial transparency and accountability, but also enables strategic planning for future growth.

By leveraging modern tools, establishing robust processes, and continually educating team members, a nonprofit can effectively manage its finances. As a result, it can prove its fiscal responsibility to its donors and governing bodies, ultimately helping to sustain its operations and further its mission. Remember, accounting is not just about crunching numbers—it's about telling a story of your nonprofit's stewardship, impact, and commitment to its cause.

Real estate agents deal with hundreds of tasks throughout the property buying and selling process. They have costs to market themselves, improve properties, pay a variety of fees, and split the commission.

By the time a property closes, there are dozens of transactions related to the realtor and their clients. This can be an accounting nightmare if you don’t have a clear system in place.

Fortunately, you don’t need an accounting background to be successful in real estate—but you should have a general understanding to help you make the best strategic decisions for your real estate business.

Keep reading to learn more about real estate accounting. Even if you’re just starting out, you can create processes that help you to scale—and to keep as much commission as you can.

What is real estate accounting?

Real estate accounting is a specialized branch of accounting that focuses on managing the financial transactions related to a real estate business. This includes tracking income from property sales or rentals, expenses such as maintenance costs, commission payouts, and property improvements, and any other transactions related to real estate activities.

A comprehensive real estate accounting system not only ensures compliance with tax and financial regulations, but also helps realtors make informed decisions to improve their profitability and growth. Whether you're a solo agent, a property manager, or a large real estate firm, understanding the basics of real estate accounting is integral to your financial success.

Why real estate accounting is important.

Understanding the importance of real estate accounting is crucial if you want to maintain financial health and propel your business forward. It not only helps track performance, but also aids in strategic planning and decision-making.

- Transparency - Real estate accounting gives a clear and transparent view of your financial situation, allowing you to understand your income, expenses, and profitability at a glance.

- Compliance - Real estate accounting ensures compliance with tax laws and financial regulations, preventing you from facing penalties or legal issues.

- Decision making - Real estate accounting aids in strategic decision making by providing vital financial data, facilitating operational improvements and expansion plans.

- Cash flow management - Real estate accounting helps in effective cash flow management, which is critical for the smooth operation of any real estate business.

- Cost management - With proper real estate accounting, you can identify areas of excessive spending and implement cost-saving measures.

- Investor confidence - Accurate and up-to-date accounting can increase investor confidence, which can be crucial if you're seeking external funding or partnerships.

- Profit maximization - Real estate accounting enables you to track and control your expenses, allowing for better budgeting and ultimately maximizing your profits.

Real estate accounting is an invaluable tool for anyone involved in the real estate industry. Its ability to provide a clear financial picture facilitates strategic planning, regulatory compliance, and ultimately, business growth. Ignoring its importance can lead to disorganization, legal issues, and missed opportunities for profit maximization.

Elements of real estate accounting.

Real estate accounting comprises several key elements that work together to provide a full picture of your business’ financial health.

- Revenue tracking - This includes all income generated from property sales, rentals, or other services offered. It's crucial to accurately record all revenue transactions to have a clear view of your business’ profitability.

- Expense management - These are costs incurred in the running of the business. They include maintenance costs, commission payouts, marketing expenses, and property improvements. Proper management of expenses helps to identify areas where costs can be reduced to increase profitability.

- Financial reporting - Regular financial reports help realtors monitor the business’ financial performance over a specific period. These reports include profit and loss statements, balance sheets, and cash flow statements.

- Tax preparation - A substantial part of real estate accounting involves managing tax-related matters. This includes determining taxable income, identifying tax deductions, and ensuring timely tax payments to avoid penalties.

- Budgeting and forecasting - This involves making financial projections for the future, based on past and current financial data. Budgeting and forecasting are essential for strategic planning and decision-making.

Understanding these elements of real estate accounting can help you navigate the financial landscape of your business, ensuring that you are making informed decisions to drive growth and profitability.

Real estate accounting basic steps.

The financial backbone of a real estate business revolves around effective accounting practices. These practices maintain the flow of funds, enabling the business to thrive even in fluctuating markets. Even though real estate accounting might seem intricate, a clear understanding of the basic steps can simplify the process dramatically.

Let's delve into the core steps of real estate accounting that can effectively manage your financial transactions and provide a clear picture of your business' financial health, regardless of the size of your real estate portfolio.

1. Choose an accounting method.

You can choose between cash-based and accrual-based accounting to track your expenses and income.

With cash-based accounting, you record income only when the cash hits your account. You also only record expenses when your business is billed for them. With this model, you can see clearly how much money you have within your organization.

With accrual-based accounting, you record income and expenses when they occur, not when money exchanges hands. For example, you can record the costs to stage a home, even if you don’t pay the stager until the following month. Accrual-based accounting is a better option if you want more visibility into the finances of your business, including future expenses and revenue streams.

However, many realtors prefer to use cash-based accounting for their firms. First, most expenses related to real estate are immediate. If you need to hire a photographer, you can cut a check for their services or request an invoice immediately. Because there isn’t a delay between the service and payment, the cash-based model works.

Many realtors also prefer the cash model because of their income sources. Sales fall through, contracts are renegotiated, and renters cancel their leases. All of these changes can harm your cash flow, especially if you already recorded the income through your accrual-based system. With a cash model, you can record the income when the sale closes or when the renter’s check hits your account. The payment is a sure thing—and the money is yours to spend.

Every business model is different, so consider your specific needs before selecting an accounting process.

2. Separate personal and business funds.

Blurring the lines between personal and business funds can lead to complicated tax issues and potential financial confusion. For transparency and accuracy, it is essential to set up separate bank accounts for your personal finances and your business transactions. This allows you to clearly track your real estate-related income and expenses separately from your personal expenses. Remember, mingling personal and business funds can raise red flags during audits and may impact your ability to accurately analyze your business’ financial performance. Keeping these funds separate is a best practice in real estate accounting that contributes to the overall financial health and integrity of your business.

3. Categorize your expenses and income.

Clear organization is the foundation of good bookkeeping. As your real estate business grows, you’ll need healthy bookkeeping habits to forecast growth and understand your financial opportunities. Consider a few of the different types of expenses that come with operating a real estate business, along with the different sources of income you can expect.

Expenses

- Realtor association fees

- Commission fees

- Marketing costs

- Administrative assistant services

- Staging expenses

- Photography and video costs for homes

- Gas and wear on your car

Income

- Commissions earned

- Commissions from realtors you add to your team

- Rental income or sales income from investment properties

- Property management fees (if applicable)

With growth comes complexity. You may bring on an assistant or purchase an investment property to flip for a profit. To prevent confusion, establish clear accounting codes related to your business. Each purchase will have a category and a code number associated with it.

If your real estate business has multiple arms (like an agent arm and an investment property arm), you may want to consider establishing multiple LLCs or keeping the books for each business channel separate. This delineation can prevent confusion, while helping you to manage each aspect of your business individually.

4. Understand your commission model.

If you’re working with a real estate brokerage to build up your business and brand name, make sure you have a clear idea of your commission fees and opportunities. Each brokerage charges its own commission structure and creates opportunities for real estate agents to negotiate their percentages, signing bonuses, and other earnings.

Consider the commission systems of a few of the largest real estate brokerages in the country:

- Keller Williams - This brokerage offers a 70/30 split with agents, where the brokerage takes a 30% cut of your commission. However, agents also pay a 6% franchise fee on their sales (up to $3,000). This means you actually have a 64/30/6 split until you pay $3,000 in fees. Additionally, each Keller Williams office has its own commission cap (typically around $28,000). Once you hit that cap in commission fees, you take home 100% of your commissions.

- RE/MAX - This company has multiple commission plans that you can choose from. First, they have a 95/5 plan where realtors take home 95% of their commissions, but pay a 5% desk fee each month. With this option, there’s no commission cap. Realtors at RE/MAX can also opt for a commission split range of 60/40 to 80/20 depending on their previous sales. Once they hit their commission cap, they move up to the 95/5 model.

If you’re still deciding which brokerage to work for, consider their commission structure and their brand name in your area. You may be able to earn more money by working for a specific firm—even if you pay them more commission than with another option.

A large part of real estate accounting is tracking what you earn in commissions and the fees you’re expected to pay over the course of the year. These numbers determine your take-home pay and your budget for marketing expenses and other investments.

5. Establish your operating costs.

The finances of a real estate professional can fluctuate significantly over the course of a year. You may experience a high number of expenses at the start of the year and then close multiple sales within a few weeks. This means that realtors need to balance their expenses so that they always have enough funds in the bank to cover basic expenses, regardless of the market.

As you establish your accounting systems, start with your operating costs. Operating expenses (OPEX) are costs that aren’t directly tied to your services. They differ from your cost of goods sold (COGS), which are costs directly related to your services.

For example, if you keep a marketing agency on a monthly retainer to maintain your real estate website, you will factor this expense into your OPEX. It doesn’t matter whether you sell a dozen houses this quarter or none—you’ll still need to pay the flat marketing fee. Additional OPEX listings include rent, a lease on a work vehicle, and utilities like internet fees or your electric bill.

Meanwhile, if you hire a photographer to help you market a house on a per-property basis, their services are part of your COGS. If 10 new listings are added within a month and you need to photograph each of their homes, then your photography expenses will be higher than if you have only two clients another month.

With the uncertain nature of the real estate business, you can use your OPEX to identify predictable costs related to your company. Your electric bill might fluctuate and gas prices might drive up your monthly bills, but you can anticipate costs related to those operating expenses every single month, regardless of your business.

6. Track all of your business expenses.

Once you have your operating costs sorted in your accounting system, you can take steps to track all of your business expenses.

Real estate agents have some of the most diverse expenses in business. They face costs ranging from landscaping services that improve curb appeal to lunches for clients and gifts for buyers. Realtors’ expenses can reach a few hundred dollars a month or into the thousands, depending on their listings, marketing strategies, and many other factors. Real estate agents also accrue these business expenses daily—which means you can easily get overwhelmed if you don’t have a system in place.

There are a few ways to keep your expenses in order as your real estate business grows. The first step is to get a business credit card. This card will separate your business expenses from your personal charges, while keeping your monthly costs all in one place. You can also get a business bank account to isolate your business transactions.

The next step is to look for software that can record your business expenses. With tools like BizXpense Tracker, you can upload receipts and track costs related to certain projects—even if you have to use your personal card. You can also download a gas mileage tracker to log how far your drive. This information will be essential when separating personal and professional gas costs, insurance payments, wear and tear, etc.

If you set aside a few minutes each day (or an hour or two weekly) to evaluate your charges and business expenses, you can keep your accounts clearly organized. This practice prevents an end-of-month scramble to reconcile your business costs with your bank account balance.

7. Set up double-entry accounting.

Regardless of whether you choose the cash or accrual model for your real estate bookkeeping, you’ll want to establish a double-entry system for your accounting materials.

A double-entry system is based on the idea that every credit has an equal and opposite debit. In accounting, a debit increases the value of accounts (a positive number) while a credit decreases the value of accounts (a negative number).

For example, let’s say you order business cards and other giveaways to market your business. These cost $500. With a double-entry bookkeeping system, you’ll credit your cash account $500, because that is how much you paid while debiting your marketing assets $500—because you now own cards, magnets, koozies, and other fun items.

The purchase of marketing materials is a simple example, but double-entry accounting also becomes valuable when you start adding assets to your real estate firm. For example, you can purchase a house to flip for $200,000. You now have $200,000 less in cash, but a significant asset worth that amount. If you flip the house for $350,000, then you can track your profits using the expense accounts in your double-entry recordings.

Double-entry bookkeeping also provides a series of checks to ensure that each entry is correct. If the two lines of credits and debits don’t align, then something was recorded incorrectly. While it might not seem like a big deal if you mistype your electric bill or are off a few dollars on your commission income, these errors can add up—and might affect your taxes and cash flow. Plus, you will have to return to your books and redo them to ensure that they’re error-free.

If double-entry accounting seems intimidating, keep in mind that many online systems will fill in the backup entry for you. Your accounting system will ask for a copy of the invoice and the expense category, then do the rest.

8. Reconcile your accounts.

Reconciliation is a crucial part of accounting that ensures all the transactions in your books accurately reflect the transactions in your bank statement. The process involves comparing your internal financial records against the monthly statements issued by your banks and credit card companies to check for discrepancies.

To execute this process, you should start by making sure the beginning balance of your records matches the beginning balance on your bank statement. Now, compare each individual transaction: the date, the recipient, and the amount. If you detect any discrepancies, such as missing transactions, double entries, or discrepancies in amounts, flag them immediately and investigate.

Remember, reconciliation should be performed regularly, preferably on a monthly basis. This is not just a good practice for keeping your books clean, but it's also an effective way to detect any potential fraud or errors early.

If you opt for financial software, most modern systems have an automatic reconciliation feature that simplifies this process. However, it's essential to understand the process and check the reconciliation report to ensure accuracy.

Remember, accurate bookkeeping is not just about compliance—it also gives you a clear picture of your financial health, thus aiding strategic planning and decision making.

9. Evaluate your performance monthly.

The purpose of bookkeeping in real estate provides two benefits: improving your future performance and forecasting your upcoming costs and income. In both cases, you’ll want to evaluate your accounts monthly to make sure your business is operating at its best.

First, review your expenses and income to understand your profit margins. For example, if you bought a property for $200,000 and sold it for $300,000, it looks like you made a nice profit. However, if you spent 12 months and $90,000 on renovations and marketing, then your $10,000 profit doesn’t seem as impressive.

Evaluating your profit margins can help you to understand how much money you really make on the sale of homes and renovations of properties. You may decide to adjust your fees or focus more on investment rentals in order to grow your profits.

Next, forecast your income and expenses for the future. This exercise isn’t always easy in the real estate field. Take your static expenses and OPEX estimates to get an idea of what you can expect to pay in the next few months. You can also use your pending listings to estimate your commissions and income. Depending on the market, you can also create forecasts for your COGS based on your average monthly leads.

Your forecast numbers aren’t meant to be exact figures. However, they serve as informed estimates on your future income and costs. These forecasts can help you understand whether the coming months will be ideal for making major investment purchases or if you’ll need to seek temporary funding sources to cover upcoming costs.

10. Organize your documents.

It's essential to maintain an organized record of your real estate business transactions, contracts, and other related documents. This includes documents related to property purchases, sales, rental agreements, and invoices for any expenses incurred.

Digitizing your documents can be highly beneficial, as it provides easy access, reduces the risk of loss, and allows for efficient categorization. Utilize document management software or cloud storage solutions for an organized, searchable collection of your important business documents. Regularly backing up these digital files can help prevent data loss.

Remember, a well-organized document system not only simplifies your business operations, but also streamlines the auditing process and ensures you comply with tax regulations.

11. Prepare early for tax season.

You can benefit from healthy accounting practices throughout the year, but one of the main time-savers for your real estate firm is having your books in order for tax season. There are multiple reasons why your taxes may be more complicated as a real estate professional:

- You will have to sort your business and personal expenses into two separate categories and may need to file taxes for both your business and personal arenas depending on your company’s structure.

- You will have multiple sources of income as you diversify your revenue streams. You’ll need to account for your commissions, any rental fees, and any profits from the sale of renovated houses that you flipped.

- You will need to record your deductions and relevant business expenses.

- You may have to pay real estate taxes on any properties you own during the renovation process. Buying and selling homes as a business can make your taxes more complicated.

If your business expenses aren’t clearly recorded and labeled, you may miss out on a significant amount of deductible income. If you lack clear balance sheets and P&L statements, it may take longer to file your business taxes. Good accounting habits can make the tax process easier and faster—while also optimizing your tax deductions.

If you want to streamline your tax filing, start reviewing your books in the fall. Make sure all expenses and sources of income are clearly recorded. Pull your receipts and relevant sales documents. Review your income statements. When your CPA or tax-prep service requests this information, you’ll already have it on hand.

Real estate accounting best practices.

Embracing accounting best practices can streamline your operations and simplify the financial management of your real estate business. Here are a few strategies to consider:

- Utilize real estate specific accounting software - Investing in a real estate-specific accounting software can automate your bookkeeping, making it easier for you to monitor income, expenses, and cash flow. It can also simplify your tax preparation and ensure your financial reports are accurate and up to date.

- Hire a professional accountant - If your budget allows, consider hiring a professional accountant who specializes in real estate. They’ll be able to navigate the unique financial challenges of the industry and can offer expert advice to optimize your financial management.

- Keep personal and business expenses separate - Always maintain a clear separation between your personal and business expenses. This not only simplifies your bookkeeping, but also ensures compliance during tax season.

- Regularly monitor your cash flow - Cash flow is crucial in the real estate business. Regularly monitor your income and expenses to avoid cash flow issues. This will help you make informed decisions about your business and can prevent financial difficulties down the line.

- Maintain accurate and timely records - Be diligent about recording all income, expenses, and financial transactions as they occur. This makes it easier to prepare accurate financial reports and will be invaluable come tax season.

Remember, effective real estate accounting isn't just about keeping books for tax purposes—it's about using financial information as a tool for strategic planning and decision-making in your business.

Common real estate accounting mistakes.

While handling the accounting side of real estate business, it's quite common to make a few slip-ups. Being aware of these mistakes can better equip you to avoid them. Here's a brief outline of the most common ones:

- Neglecting regular bookkeeping - Delaying or neglecting to update your books regularly can lead to inaccuracies and missed deductions, which can significantly impact your bottom line. Try to develop a habit of regular bookkeeping to maintain accurate and up-to-date records.

- Mixing personal and business expenses - It's crucial to keep your personal and business expenses separate. Mixing these can create confusion, make your bookkeeping more complicated, and potentially result in inaccurate tax filings.

- Inadequate record-keeping - Not maintaining comprehensive and accurate records of all transactions can lead to serious issues during tax filing or an audit. These records should include receipts, invoices, and cash flow statements.

- Not utilizing real estate specific accounting software - Real estate-specific accounting software can streamline your accounting process and significantly reduce the chances of errors. Choosing to do everything manually or using non-specialized software can increase your workload and the likelihood of mistakes.

- Failing to plan for taxes - Real estate professionals often overlook the importance of planning for tax season. Not setting aside funds for tax payments or failing to prepare your books in advance can lead to a frantic scramble during tax season.

- Neglecting to reconcile books with bank statements - Failing to regularly compare your bookkeeping records with your bank statements can mean missed discrepancies, leading to potential errors or fraud going unnoticed.

Remember, avoiding these common mistakes can save you from future headaches and ensure your real estate business runs smoothly and efficiently.

Streamlining your real estate accounting process is crucial not just for tax compliance, but also for accurately gauging the financial health of your business and making informed strategic decisions. Regular bookkeeping, vigilant record-keeping, and the use of industry-specific accounting software can greatly simplify this process and minimize the likelihood of errors.

Consider professional help if your budget allows fo it, and always keep business and personal expenses distinct. Remember, good accounting practices are not just about keeping the IRS satisfied—they provide valuable insights into your business, helping you strategize and grow. Avoiding common mistakes and implementing best practices in your accounting can set your real estate business up for lasting success.

As a small business owner, your cash flow is your lifeline. But what happens when the cash doesn't flow just when you need it? Imagine if there were a way to unlock the funds tied up in your unpaid invoices, instantly.

Welcome to the world of spot factoring, also known as single-invoice factoring. This financial tool is all about turning your invoices into immediate cash, enhancing your liquidity and keeping your business running smoothly. Let's delve into how spot factoring can support your business growth.

How spot factoring works.

Getting started with spot factoring involves a few steps which we've broken down for you:

- Identify the invoice - First things first, you need to identify the invoice you want to sell.

- Choose a factor - Next, you'll need to find a factoring company. You may want to consider different factors, such as their fee structure, the percentage of the invoice they'll advance, and their reputation.

- Sell the invoice - Once you've chosen a factor, you sell them the invoice. Typically, they'll advance you a large percentage of the invoice value, often between 70% and 90%, straightaway.

- Customer pays the factor - Now it's time for your customer to pay the invoice, but instead of paying you, they'll pay the factor.

- Receive the remaining balance - Once the factor has received the invoice payment from your customer, they'll give you the remaining balance of the invoice, minus their fee.

This process allows you to access the cash tied up in your invoices immediately, helping to maintain a healthy cash flow for your business.

Spot factoring rates and terms.

Spot factoring rates and terms can vary depending on the factor you choose, as well as factors such as your business' creditworthiness and the creditworthiness of your customers. Generally, the advance rate ranges from 70% to 90%, with a fee of around 1% to 5% for every month that the invoice is outstanding.

Qualification criteria for spot factoring.

To qualify for spot factoring, there are a few key criteria you'll need to meet. First, your business must issue invoices to customers on credit terms. The invoices you factor should be due and payable within 90 days. They need to be free of liens and encumbrances, meaning they aren't pledged as collateral in another financial arrangement.

Additionally, the customer you're invoicing must have a good credit history, as the factor will collect the money directly from them.

Lastly, the invoice must be for work that has been completed or goods that have been delivered.

Each factoring company may have its own specific requirements, so it's essential to review these before proceeding.

Pros and cons of spot factoring.

Like any financial tool, spot factoring has its pros and cons. Here are a few to consider:

| Pros | Cons |

| Immediate access to cash Flexible option, as it's done on an invoice-by-invoice basis No long-term contracts or commitment Allows business owners with low credit scores to qualify based on their customers' creditworthiness | Higher fees compared to traditional lending options Can impact customer relationships if they are required to pay the factor instead of you Might not be suitable for businesses with consistent cash flow issues |

Spot factoring vs. accounts receivable factoring.

Both of these methods are effective ways to improve cash flow. However, they have some key differences that make them more appropriate for different situations.

Spot factoring focuses on one invoice at a time. This type of factoring is ideal for businesses that occasionally need quick cash or want to control which invoices are factored.

Accounts receivable factoring involves selling a bulk of invoices to a factor. This is a more comprehensive solution that offers consistent cash flow. It's ideal for businesses that have a number of unpaid invoices and need a steady influx of cash. Unlike single-invoice factoring, accounts receivable factoring usually involves a long-term contract with the factoring company.

In both cases, the factoring company will handle the collection of payments, but the choice between spot factoring and accounts receivable factoring ultimately depends on your business' needs and cash flow situation. Make sure to thoroughly evaluate both options to figure out which one is the best fit for your company.

Is spot factoring right for your business?

Spot factoring can provide a much-needed boost for small businesses experiencing cash flow issues. However, it's not necessarily the best option for every business. Consider your specific needs and weigh the pros and cons before making a decision. And as always, it's important to consult with a financial advisor or expert before committing to any financial tool. But if you're looking for a way to turn your receivables into cash and keep your business running smoothly, spot factoring might just be the solution you've been searching for.

Ready to get started? See if you're eligible for accounts receivable financing.

The IRS announced an immediate moratorium on processing new Employee Retention Credit (ERC) claims on September 14, 2023. The moratorium will last through at least the end of the year in an effort to protect small business owners and taxpayers from scams and fraudulent claims.

As a small business owner, you may be wondering what this moratorium means for you and your business. Here’s everything we know and how you may still be able to apply for the ERC during the moratorium.

What we know.

We know that the IRS is continuing to process ERC applications that were received prior to the moratorium. However, processing times will be longer, the IRS advised in its Sept. 14, 2023 update — potentially going from a 90-day turnaround to 180 days or more. The agency has increasingly shifted its focus to review claims for compliance concerns and recently announced that thousands of ERC claims have been referred for audit. It is also working on hundreds of criminal cases on promoters and businesses filing suspicious claims.

Payouts for these previously filed claims will continue through the moratorium, but at a slower pace due to the more in-depth compliance reviews. This payout period will extend to 180 days from its previously standard processing goal of 90 days, according to the IRS. However, a payout may take even longer if its claim requires the IRS to further review or audit it.

The IRS is implementing this more scrutinous compliance review period to protect businesses from facing penalties or interest payments that stem from bad claims that aggressive marketers pushed.

For any business owners wanting to submit claims after September 14, 2023, while the IRS is not reviewing new applications until at least January 1, 2024, you can still submit an ERC claim during the moratorium.

Applying for the ERC.

Small business owners planning to submit an ERC claim after September 14, 2023 should ensure that their businesses are eligible for the tax credit prior to filling out the stringent application.

Pay qualified wages.

First, ensure that your business paid qualified wages to your employees. The definition of qualified wages varies depending on the amount of employees your business had on the payroll in tax years 2020 and 2021.

For tax year 2020, the IRS defined a small business as a business that averaged 100 or fewer full-time monthly employees in 2019. For tax year 2021, it expanded the definition to include businesses that averaged 500 or fewer full-time employees in 2019.

Larger employers can claim the ERC but only for wages and some healthcare costs paid to employees who did not work.

Small businesses can claim the credit for all employees, whether they worked during the period or not.

Government-mandated full or partial suspension.

Your business must have been impacted by either a government-mandated lockdown or decrease in revenue to be eligible for the ERC. You can qualify if your business was impacted by a full or partial suspension of operations due to a government COVID-19 order during any quarter (this includes restrictions on hours or capacity).

This area of eligibility criteria can be complex, so make sure to work with a vendor who is familiar with government orders, their impact, and the timeframe they were enacted.

Significant decline in gross receipts.

If your business experienced a “significant decline” in gross receipts as defined by the IRS, then it can be eligible for the ERC. For tax year 2020, a significant decline means that gross receipts for a quarter are less than 50% compared to the same period in 2019. For the first 3 quarters in 2021, a significant decline means quarterly receipts are less than 80% compared to the same period in 2019.

If your business did not see a 20% decline in gross receipts in the first 3 quarters of 2021 compared to 2019, you can also elect to use the immediately preceding quarter for comparison. This means that if a business’s Q2 of 2021 isn’t eligible compared to Q2 of 2019, it can instead use Q1 or 2021 and compare it to Q1 of 2019 to meet eligibility requirements.

Recovery startup business.

The ERC was amended in 2021 by The American Rescue Plan to let newer businesses gain access to the tax credit. A recovery startup business is defined as one that opened after February 15, 2020, and has annual gross receipts under $1 million. As long as you meet these two criteria and have one or more W2 employees, you don’t have to meet the other eligibility requirements. If your business qualifies as a “recovery startup business,” you can apply for the credit for Q3 and Q4 of 2021, and your business can receive a maximum of $50,000 in ERC per quarter.

If your business meets these requirements, then it may be eligible for the ERC. When applying, make sure that you have gathered thorough records proving wages paid, gross receipts, government orders, and other required documentation. Please note that businesses that improperly claim the ERC will be required to pay it back, potentially with penalties and interest.

Applying for the ERC during the moratorium period.

You should consult an accountant or tax professional prior to filling out any forms. They will help guide your business through this stringent and potentially confusing process.

You can apply for the ERC during the moratorium period through Lendio. We’ll help you identify what documents you need to claim the ERC. We’ve partnered with ERC and tax experts to aid you in the complex application process. They can help navigate you through tricky tax laws and avoid costly mistakes while calculating the full tax credit that you qualify for. After your application is complete, we’ll file your ERC claim with the IRS.

Please note that this process will be extended significantly due to the moratorium. While you will be able to submit your application to the IRS prior to January 1, 2024, it will not be reviewed until after that date (and with more stringent compliance review terms).

If you have additional questions regarding the ERC and/or the ERC moratorium period, check FAQ resources from the IRS and Lendio.

The Paycheck Protection Program (PPP) and Employee Retention Credit (ERC) were created to help businesses stay afloat during COVID-19. If the pandemic has had a negative impact on your small business, you might wonder whether you can take advantage of both of these programs. Keep reading to find out.

Key Points:

- The PPP was a forgivable loan. The ERC is a refundable tax credit.

- The PPP loan program is no longer available. The ERC can still be claimed retroactively.

- Businesses that received a PPP loan can still apply for the ERC.

- Employee wages used to receive PPP loan forgiveness cannot be used in your ERC claim.

What Is the Paycheck Protection Program?

Established by the CARES Act and administered by the U.S. Small Business Administration (SBA), the PPP offered loans of up to $10 million to small businesses that faced financial hardship as a result of COVID-19.

As long as you qualified, you could have received a loan for up to 2.5 times of your average monthly payroll costs. The loan can be forgiven completely if you file a forgiveness application and show you used the proceeds to cover rent, utilities, payroll costs, and other qualifying expenses.

What is the Employee Retention Credit?

The ERC is a refundable payroll tax credit for qualified wages paid to employees in 2020 and 2021. It was created under the CARES Act and administered by the Internal Revenue Service (IRS) to encourage businesses to retain their employees during the pandemic.

You may qualify if you experienced partial shutdowns due to government orders or significant declines in quarterly gross receipts due to COVID-19. If you meet certain eligibility criteria, you can claim as much as $5,000 per employee in 2020 and as much as $21,000 per employee in 2021.

Differences Between PPP and ERC

While the PPP and ERC were both designed to support businesses that have struggled financially as a result of the pandemic, there are several noteworthy differences between these two programs.

| PPP | ERC | |

| Type of funding | Forgivable loan | Tax credit |

| Funding time | 10 days | 3-6 months |

| Cost | Any funds you didn’t receive forgiveness for | None |

| Amount | 2.5x the average monthly payroll costs | Up to $26,000 per W-2 employee |

| Still available | No | Yes |

Type of Funding

The PPP offers a forgivable loan. If you used the funds on payroll, rent, and other qualifying expenses, you wouldn’t have to pay it back. In the event you used part of the loan for non-qualifying reasons, that portion won’t be forgiven. You’ll have to repay it with a fixed interest rate of 1% over a period of either two or five years. The ERC, on the other hand, is a tax credit you won’t have to repay.

Funding Time

If you qualified for the PPP loan, you would have received the funds via direct deposit, usually within ten days of approval. The ERC, however, will be distributed to you after you file Form 941-X and the IRS has reviewed your claim. The IRS will process the credit you’re owed and send you a check. The IRS can take anywhere from 3-6 months+ to process your credit. We highly recommend reserving your place in line now by filing the necessary paperwork with the IRS.

Cost

It was free to apply for the PPP loan. You would only incur a cost if you don’t use the loan proceeds on qualifying expenses and must pay it back. There’s no governmental fee to receive the ERC either. It’s a tax credit that you can receive by filing an amended payroll tax form for each of the tax periods that you qualify for. The only expense you may face will be service charges if you ask an accountant or tax professional to assist in preparing and filing your tax forms.

Eligibility

The eligibility requirements for the ERCwere updated in 2021.

2020 qualifications:

- Qualifying wages of up to 100 full-time employees

- A decrease in gross revenue of at least 50% compared to the corresponding quarter in 2019

- Or either a full or partial suspension of business operations created by a government mandate

2021 qualifications:

- Qualifying wages of up to 500 full-time employees

- A decrease in gross revenue of at least 20% compared to the corresponding quarter in 2019

- Or either a full or partial suspension of business operations created by a government mandate

PPP loan requirements included:

- A small business with 500 employees or less

- The business was operational before February 15, 2020

- For second-draw loans, the business must have used up previous loan funds and demonstrate a 25% or more reduction in gross revenue.

Can You Get Employee Retention Credit and PPP?

Initially, a business that received a PPP loan was not eligible for the ERC. Thanks to the Consolidated Appropriations Act of 2021, however, a business that received a PPP loan may also apply for the ERC retroactively back to 2020.

The caveat, however, is that you can’t use the wages that qualify you for PPP loan forgiveness to determine your ERC amount. You’ll need documentation that proves you’re not “double dipping” and using both programs to cover the same wages.

Let’s say you used your PPP funds to pay for $50,000 in wages and you expect to qualify for forgiveness. In this scenario, you can’t use those wages that have been forgiven to calculate your ERC.

How to Apply for PPP and ERC

You can no longer apply for a PPP loan, but you can still fill out an application for the ERC. If you’d like to claim the ERC, you can do so on Form 941-X. Don’t hesitate to consult a tax professional for assistance.

How to Maximize the PPP and ERC

There are a few ways you can maximize the benefits of both the PPP and ERC, including:

- If you included non-payroll costs in your PPP loan forgiveness application, show you used a minimum of 60% of the total loan on payroll. This way you’ll be eligible for full forgiveness.

- In the event you don’t list qualifying non-payroll costs on your application, you must prove that you used 100% of the loan amount on payroll to get your loan completely forgiven.

- Provide detailed explanations to help the tax professional you work with understand exactly how the government orders impacted your business. This will help them maximize the amount you qualify for.

- Don’t forget to separate the total payroll costs you used for the PPP loan from the total payroll costs you list with the ERC. This can help you avoid getting denied for using the same payroll costs for both programs.

- Use a tax professional vs. filing yourself. Though you may pay money, these professionals often understand the program much better than you ever could on your own. As a result, they often can help you qualify for more money than you would on your own. They also will help ensure that you file the credit correctly so that in the event of an audit all of your i’s are dotted and t’s are crossed.

Reap the Benefits of the PPP and ERC

If you previously applied for PPP, there’s no reason not to apply for the ERC. By doing so, you can mitigate the financial losses you may have incurred during the pandemic and set your business up for future success.

Have you heard of the Employee Retention Credit (ERC)? For business owners who endured the COVID-19 pandemic and the economic roller-coaster it brought, the ERC was meant to provide financial relief and keep their workforce employed. Now, even though the economic impacts of the pandemic have subsided, business owners like you can still take advantage of this tax credit. To find out if you qualify and how the Employee Retention Credit works, read our answers to the Employee Retention Credit FAQs below.

General overview questions

What is the Employee Retention Credit (ERC)?

The ERC is a tax credit. This means, when applied, the ERC will reduce the total amount of taxes a business owes to the Internal Revenue Service (IRS). The ERC was part of the Coronavirus Aid, Relief, and Economic Security Act (CARES Act) which was passed in March 2020 by the U.S. Congress. It was intended to lessen the pandemic's economic impact on businesses and encourage them to retain employees as much as possible.

The ERC is a fully refundable tax credit. This means, that if your business’ ERC is greater than your federal employment taxes, it could create a negative federal tax liability for a business and result in a tax refund. At the very least, it could lower the amount of taxes your business pays—at most, you could receive a refund check.

Am I eligible for the Employee Retention Credit?

To be eligible to receive the Employee Retention Credit, you must meet the following criteria:

- Your business is a private sector or tax-exempt organization that carried out business in 2020 and/or 2021.

- Your business paid qualified wages to employees in 2020 and/or 2021.

- Your business experienced hardship in one of the following areas:

- You were forced to suspend your business’s operations, including limiting commerce travel or group meetings, fully or partially due to COVID-19 government orders, or

- You experienced a significant decline in gross receipts beginning in the first quarter of 2020.

Since you’ll be required to prove your business’s eligibility, knowing the definitions of a partial business suspension or a significant decline in gross receipts is critical.

A partial business suspension is one in which total employee hours fall below 10% of the business’ typical total employee hours. An example of a partially suspended business would be a restaurant that could no longer welcome dine-in customers but continued to provide carry-out or delivery services. For more details on full vs. partial suspension of business, click here.

A significant decline in gross receipts is when a business’s gross receipts started dropping in the first quarter of 2020 to 50% or less of the gross receipts of the business in the first quarter of 2019. For more details on the definition of a decline in gross receipts, visit the IRS page on the topic.

Learn More: Employee Retention Tax Credit: is your small business eligible?

What exceptions or restrictions should I be aware of in the ERC?

A few other exceptions exist to the guidelines above. For example:

- Self-employed individuals may not claim the credit based on their earnings, but they can for wages paid to any employees they may have.

- Certain tribal government organizations or entities might be considered eligible.

- Businesses that received Paycheck Protection Program (PPP) loans from the government can claim the tax credit, but not for wages that were paid using a PPP loan.

- Businesses that receive tax credits under the Families First Coronavirus Response Act (FFCRA) employer-paid leave requirements can’t count qualified leave wages in their ERC calculations.

- Businesses cannot count wages they’ve attributed to the R&D tax credit in their ERC calculation.

For more information on these and other exceptions, visit the IRS page on this topic.

How is the Employee Retention Credit determined?

A business’ ERC amount is determined based on its qualified employee wages and the year in which those wages were paid. Here’s how it works:

- For wages paid from March 13 to December 31, 2020, the tax credit is worth 50% of qualified employee wages. The highest amount that would be considered qualified employee wages for any one employee is $10,000 for the entire year. Following that math, the maximum credit a business can get per qualified employee is $5,000 (i.e., 50% of $10,000).

- For wages paid in 2021, the tax credit is higher: 70% of qualified employee wages. The highest amount of qualified wages paid that would be considered for any one employee is also larger: $10,000 per month. Therefore, the maximum credit a business can receive for 2021 is considerably larger than for 2020. Important note: businesses can claim the credit for the first three quarters of 2021 only, not the fourth.

It’s worth noting here that qualified health plan expenses—defined as amounts paid or incurred by the business that are allocable to employees’ qualified wages to provide and maintain a group health plan, but only as they are excluded from employees’ gross income—are also factored into these wage figures.

To get the full details on how the ERC is determined, visit the IRS page on the topic.

Can I still take advantage of the ERC?

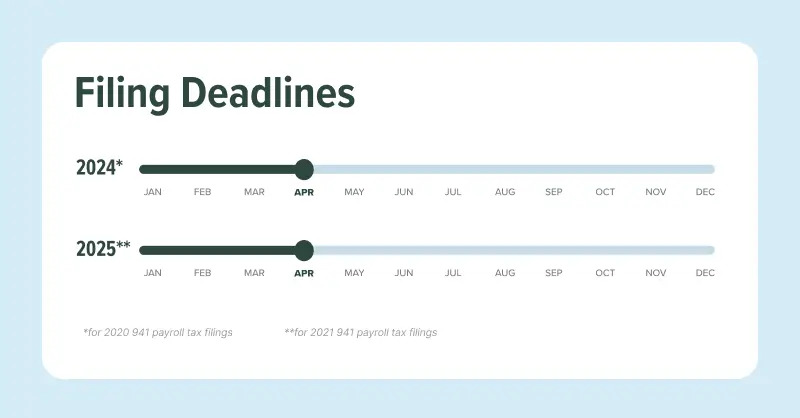

Yes. If you want to take advantage of the 2020 ERC, you can apply until April 15, 2024. Likewise, the 2022 ERC will not lapse until April 15, 2025.

How do I apply for the ERC?

To apply for the Employee Retention Credit, you should file an amended Form 941X as part of your quarterly federal tax return for any 2020 or 2021 quarter in which your business was eligible for the ERC.

Qualification questions

What is a recovery startup business?

Originally, the ERC was only available to established small businesses that experienced significant declines in revenues or operational shutdowns due to COVID-19. The American Rescue Plan (ARP) amended the ERC eligibility requirements to extend the credit to newer businesses. These are known as “recovery startup businesses.”

To claim the ERC as a recovery startup business, your operation must meet the following requirements:

- Started doing business after February 15, 2020