For many people, the American Dream is to take a great idea and turn it into a thriving business. Yet it’s rare that a great idea alone will convince an investor or lender to take a chance on you. Before a lender in particular will approve your application for a business loan, you typically need to prove that you and your business are good credit risks.

Some borrowers may have trouble satisfying the qualification requirements of traditional commercial lenders—especially startups and small business owners with less-than-perfect credit. This inability to access financing could be a key factor that drove 61% of small business owners to rely on personal funds to address financial challenges in their companies in 2021 (based on a Federal Reserve report).

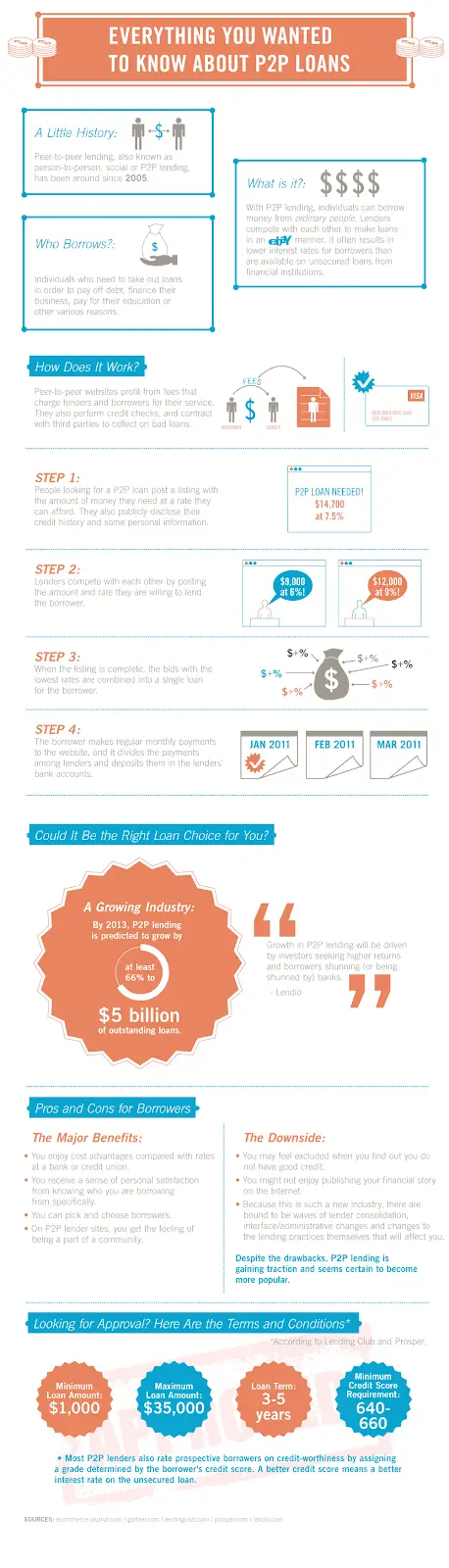

If you find yourself in a similar situation where you need business capital, but traditional financing doesn’t make sense, peer-to-peer (P2P) lending could be worth considering. Here’s what you need to know about how this alternative business loan solution works. You’ll also learn whether P2P loans are safe and how to determine if they are the right fit for your small business.

What is peer-to-peer lending?

Peer-to-peer lending is a method of borrowing money that allows you (aka the borrower) to access funds from multiple investors (aka peers), rather than a single lender or financial institution. Due to this unique borrowing structure, P2P lending is sometimes called person-to-person lending or social lending, as well.

P2P lending platforms utilize technology to bring different investors together to fund an individual loan. Some P2P platforms may even allow lenders to compete with one another to make loans—sometimes (though not always) resulting in more attractive interest rates and loan terms for borrowers than they might receive elsewhere. In other scenarios, borrowers may be able to qualify for financing that they might not otherwise have qualified to receive.

How does peer-to-peer lending work?

Peer-to-peer lending marketplaces use fintech (aka financial technology) to match would-be investors with would-be borrowers who are seeking various types of loans. It’s important to understand that P2P platforms are not lenders themselves. However, the online platform can help perform the following tasks:

- Collect and process a loan application from the prospective borrower

- Facilitate a credit history and credit score check

- Share your potential loan offer (including APR and fees) if you’re eligible for financing

- Move your loan to the funding stage, if you accept the offer

- Share your loan listing with investors to see if any are interested in funding it

- Service funded loans, process monthly payments, and divide payments among investors

- Contract with third-party debt collectors to collect defaulted debts

Is peer-to-peer lending safe?

The U.S. Small Business Administration (SBA) notes that peer-to-peer loans could be a practical alternative financing solution for small businesses. Yet the agency cautions that there are both benefits and drawbacks to consider before a business decides to move forward.

As a borrower, one of the first details you should understand about a P2P loan is the cost. In addition to the interest that the investors charge on your business loan, the P2P platform may charge supplemental fees. (Investors may pay fees to the P2P platform, as well.) Of course, any type of financing comes at a cost, but it’s always wise to do the math, so you know what you’re agreeing to pay for a business loan up front.

For investors, it’s important to know that P2P investments are not FDIC-insured. Therefore, you may face an added degree of risk with this type of investment compared with other options. At the same time, if the process goes smoothly, you might enjoy higher returns than you’d receive from FDIC-insured CDs or savings accounts. It’s up to you to determine your risk tolerance and how much of your portfolio you’re comfortable exposing to higher-risk investments.

Is a peer-to-peer loan right for you?

If you’re wondering whether a peer-to-peer loan could work for your business, there are a few details you’ll want to consider. First, it’s wise to review your credit reports and scores (from all three credit bureaus, if possible).

A lender will likely review one of your consumer credit reports and scores when you apply for a P2P loan. Therefore, it’s helpful to know the condition of your credit before you apply for financing. You can access a free credit report from Equifax, TransUnion, and Experian via AnnualCreditReport.com once every 12 months. Through the end of 2023, you can take advantage of free weekly credit report access through the same website.

Next, make sure you’re in a position to afford a new business loan. If you believe your company might struggle to afford a new monthly loan payment, now may not be the time to seek new financing.

Finally, shop around and compare P2P loan offers from multiple companies. You may also want to consider other types of small business loans. Comparing different financing offers can help you make sure you find the best deal available for your company.

Debt financing has long been a preferred financing option for small business owners. It’s true that the majority of entrepreneurs leverage their own money to start or run their business, but those funds often fall short of the ultimate need. In these cases, a business loan gives you more control than you’d get with other routes such as angel investors or borrowing from family members.

However, lenders reject the majority of business loan applications. Rather than letting this reality deter you, it should merely encourage you to put your best foot forward whenever submitting an application. There’s no shame in getting denied by a lender. It happens to everyone. What matters is that you try your hardest and put your business in the best position to succeed.

Here’s a closer look at common reasons loan applications are rejected. Some are easily remedied, while others take more effort. The important thing to note is that none of these factors is a death sentence. If you find that one of them contributed to a rejection, simply make a goal to improve it for your next application. With this focus on incremental improvement, anything is possible.

Here are some of the most likely reasons an application gets axed:

You Botched the Application

One of the biggest contributors to loan rejections is also among the most basic: the applicant didn’t handle the process correctly. This includes leaving sections of the application unfinished, entering incorrect information, or failing to include the required documentation.

You can reduce the risk of this fate by preparing your documents ahead of time. You’ll find it’s much easier to write a business plan or locate your tax returns when you don’t do it the night before the deadline.

Put yourself in a lender’s shoes and it’s understandable why they’re sticklers for details. Because lenders make informed decisions based on the contents of your application, forgetting to complete a section, including erroneous information, or neglecting to send the required documents makes their decision much easier. If you can’t be trusted to fill out an application correctly, how can you be trusted with a large sum of money?

Imagine if a friend asked you to borrow money but had no clear idea what they would be spending it on. That kind of disorganization would probably be met with a polite rejection from you. Most people only loan money to a friend if they trust them and have an idea of where the money is going.

Your Credit Score is Lacking

Credit scores result from an algorithm that lenders use to predict how likely you are to repay the money they might provide to you. The determinants of your score come down to relevant factors such as how promptly you pay your recurring bills and how much of your credit card balance you pay off each month.

Business owners have 2 types of credit to watch: personal and business. That’s right—your business has its very own credit report and credit score from Equifax, Experian, and Dun & Bradstreet, the 3 major business credit bureaus.

A low credit score can stem from a history of late payments, unpaid tax liens and judgments, or high use of available credit. But lenders can also ding you for not having established a long enough credit history.

Just because your score isn’t where it needs to be for one loan doesn’t mean you’re out of luck. Each lender has their own standards and they generally aren’t shy about broadcasting them. So when you see credit score requirements associated with a loan, take them seriously. You’ll save yourself a lot of time by not chasing loans you aren’t qualified to receive.

You can turn around a low score by paying down debt, paying your bills on time, and keeping your account balances low. If insufficient business credit is the issue, Credit Karma recommends taking the following actions to establish a credit history:

- Apply for and use a business credit card.

- Open a business bank account under your business name.

- Get a business phone under your business name.

- Apply for an employer identification number (EIN) from the IRS.

- Register your business with Dun & Bradstreet to get a free DUNS Number.

Taking these steps—and being consistent—can help you improve your business credit score so you can qualify for financing, maybe even at a better rate.

Your Business is Too Green

Every business needs to start somewhere, and there’s no shame in being a young company. It’s actually something to be proud of because it takes determination to turn your idea into a reality.

But many lenders will be understandably skittish when dealing with businesses that lack a track record. The success rates of a company over two years old are much higher and your banker, by his or her very nature, is highly risk-averse. They usually won’t take a risk on a very young company. You should also know that they will likely use your company tax returns to determine how long you’ve been in business. With that in mind, even if you don’t have much to report, file your returns starting with the first year to establish your company’s age right from the start. Your ability to repay your debt is substantially impacted by the amount of money your business brings in, so the more evidence of cash flow you can provide, the better. And for young businesses, this type of evidence is in short supply.

You Need More Collateral

Many small business loans are secured loans, meaning you need to offer something of value to protect the lender in case you aren’t able to make the necessary payments. Assets used for collateral include vehicles, homes, properties, equipment, and retained income.

Lenders prefer borrowers who have skin in the game—assets offered up as collateral, which the borrower would forfeit if they defaulted on their loan. Before you reapply for financing, document all of your personal and business assets, such as equipment, bank accounts, real estate, vehicles, and even accounts receivable, and then decide which you’d be willing to use to secure a loan. As you work through the list, consider your likelihood to default and what the consequences would be if you had to forfeit the assets.

When you lack an adequate asset to use as collateral, you’ll find that lenders are more likely to turn down your applications. While this can be frustrating for borrowers, it makes sense. If lenders always handed out money without guarantees, it wouldn’t be long before they’d run out of it.

Your Cash Flow is Lacking

When lenders want to quickly assess an applicant, they often start with cash flow. Not only does it show the strength of your business performance, but it provides a glimpse into your ability to manage details and stay on top of expenses.

If your business is new, it often lacks the track record needed to instill confidence. The good news is that certain loan options are ideal for newer businesses. Just make sure your business tenure lines up with the requirements for a specific loan before you apply. Some businesses experience seasonal slumps, which is understandable to lenders. What they’ll want to see is that you can balance your financial obligations year-round. Accounting software makes this easier to accomplish by tracking invoices so you can collect payments promptly. Also, this type of software can quickly create cash flow reports for loan applications.

You Went for the Wrong Loan

There are times when a borrower has all their ducks in a row, yet they’ve simply applied for a loan that isn’t a good match for their business. Perhaps your business doesn’t qualify due to its size or structure, or your business plan calls for using the money in ways the lender doesn’t approve.

The point is that your due diligence needs to take into account the nuances of each lender so you don’t waste time applying for a loan that will never be possible for your business.

Banks look at your debt-service ratio to determine whether you’ve got enough cash flow to make the loan payments. To calculate the ratio, take your annual net operating income and divide it by your annual debt payments. Higher numbers are better. You’ll need at least 1.15 for a Small Business Administration (SBA) loan guarantee, and lenders could require a stronger ratio. Next time you apply, run your anticipated loan amount through an online loan calculator to make sure you’re not overreaching.

At the other end, it’s just as much work for lenders to extend a large loan as a small one, but they make more money on the large one. If you’re finding yourself feeling pressured to apply for more than you need just to qualify, consider alternative sources of financing, such as crowdfunding, angel investors, or an SBA microloan.

Your Business Plan is Underwhelming

Many lenders ask for business plans as part of the application process. They’ll review your plan to see how you intend to spend their money, as well as to gauge your organizational and strategic abilities.

Writing a business plan speaks volumes about whether your company is a good investment, and it’s one of the primary tools lenders use to evaluate business loan applications. If yours wasn’t up to snuff the last time you applied for a loan, take the time now to whip it into shape. In addition to descriptions of your company and its structure, your product or service, and your sales and marketing plan, the SBA recommends that you present the following:

- A market analysis

- Financial projections based on your income and cash flow statements, balance sheets, and budgets

- An appendix with documentation supporting your application

Applying for a business loan is never easy, but it’s preferable to letting cash-flow issues keep your company from growing. By shoring up your credit, keeping your requested loan amount realistic, and wowing lenders with a business plan that shows you and your company in the best light, you’ll maximize your chances of getting the funding you need to take your business to the next level.

Never rush this stage of the application. Your business plan is your sales pitch, as well as your guiding light. If done correctly, it will sufficiently impress the lender so that you can obtain the financing you require. Once you have the money, it will then serve as your blueprint for spending it in the most effective way possible.

Your Financial Statement are Lacking

Not having accurate, informative, timely, accessible, and comparative financial data will hurt your chances if you need to raise money and get a business loan, underscoring just one of the reasons to make sure this part of your business is handled professionally. Here are the most common errors and pitfalls that will hinder your business from raising funds:

Revenue Recognition

Actually “earning” your revenue is almost never directly correlated to when you send an invoice to or receive money from your customers. Each industry has one right and many wrong ways to recognize revenue, and bankers and sophisticated investors will be familiar with each. If you are a software company and the banker does not see that you have an account called “Deferred Revenue” on your balance sheet, for example, they will lose confidence in your ability to run your business.

Gross Margin

There are two main expenses in a business, and they should be separated on your profit and loss statement. Specifically, all expenses directly related to the manufacturing of your products or the fulfillment of your services, also referred to as costs of goods sold or cost of sales, should be subtracted from your net revenue (correctly recognized as mentioned above) to determine your gross profit. Then divide your gross profit into your net revenue to find your gross margin. Many businesses fail to show this separate from the rest of their expenses and net profit before taxes, but it is a number bankers and investors want, and need, to know.

Balance Sheet Reconciliations

Every single account on your balance sheet should be reconciled every month, not just your bank and credit card accounts. This includes a thorough review of your accounts receivable, inventory, accounts payable, payroll liabilities, inter-company loans, and more. You need to be able to explain to a banker or investor what each account represents and even be able to provide documentation, upon their request, to validate the balance reflected on your balance sheet. Too many businesses pay little or no heed to their balance sheet, but investors and bankers know it drives the accuracy of everything you present in your financial statements.

Lack of Metric and Ratio Knowledge

You need to know your numbers, and, even more importantly, you need to know what they mean in the context of your past, future, and industry as well as the perspective of bankers and investors. Bankers care about current ratio, days sales outstanding, working capital days, inventory turnover, fixed charge coverage ratio, and other proofs of your liquidity, stability, sustainability, and wherewithal to pay them back. Investors care about EBITDA, free cash flow, burn rate, and other things dealing with the cash required to grow the business and the potential return their investment may garner.

Your Debt Utilization Raises Red Flags

Lenders will pay close attention to the credit currently available to your small business. If you’re using too much, it could mean you are already stretched thin and might not be able to handle your repayments consistently.

On the flip side, if you haven’t utilized credit in the past, you could be considered a risk because you won’t have a debt track record from which they can base their decision. If you have a healthy amount of credit available and are only using a moderate amount, that puts you in the safety zone. It shows you have responsibly borrowed money in the past and know how to handle the repayments.

You Don't Have Any Income

Unlike an equity investor who will reap the rewards of their investment when a business is either sold or goes public, the first loan payment will likely be due somewhere around 30 days after a business owner receives the proceeds. In other words, if there isn’t sufficient income to make the loan payments, it’s unlikely the lender will approve the loan.

Your Loan Isn't Cost-Effective for the Lender

Don’t forget that it costs money to lend money. So if you apply for a small loan from a larger lender, they might see it as more effort than it’s worth. There are plenty of financing options for small dollar amounts, but you need to make sure you’re approaching the right lenders.

The Best Way to Begin Your Loan Search

Many of the mistakes listed above involve carelessness on the borrower’s part. They didn’t research the lender well enough or they didn’t carefully prepare their application. So pump the brakes a bit and take the time to understand your financial needs and identify the exact amount of money you’ll need to borrow.

According to the SBA, the median small business loan in America is $140,000. And the majority of loans are for less than $250,000. These numbers don’t necessarily mean you should follow the trend and ask for $140,000, but it provides a helpful baseline as you decide on the best amount for your needs. Use our SBA loan calculator to estimate your monthly payment and how large of a loan you can afford.

Another crucial factor is when the funds will be in your account. If you need the money right away, you’ll need to look at a small selection of expedited loans. If you have a more generous timeline, you can probably seek out slower options such as SBA loans (which can take up to 3 months to fund).

How to Recover from a Rejected Loan Application

First of all, don’t get discouraged. Only about 1 in 10 applications for small business loans are approved. It’s incredible (in a bad way) that 9 out of 10 business loan applications are rejected.

Having your loan application rejected is a wake-up call that your credit or business health isn’t as strong as you thought (or hoped) it was. It can be a very demoralizing experience—especially if you were counting on that financing to sustain your business operations.

When a loan application is denied, it can usually be traced back to two explanations: bad credit or a high debt-to-income ratio. Fortunately, both of those things can be fixed with responsible practices and a little patience, making you more likely to get a “yes” the next time. Here are 6 things to do as soon as your loan application is denied.

1. Study your rejection letter

All lenders are required by law to send you a written notice confirming whether your application was accepted or rejected, as well as the reasons why you were turned down for the loan. According to the FTC:

“The creditor must tell you the specific reason for the rejection or that you are entitled to learn the reason if you ask within 60 days. An acceptable reason might be: ‘your income was too low’ or ‘you haven’t been employed long enough.’ An unacceptable reason might be ‘you didn’t meet our minimum standards.’ That information isn’t specific enough.”

Understanding the “why” of your rejection helps you know where to focus your efforts, whether that means paying down your existing debt or building more credit history. So, instead of balling up the letter and tossing it into the trash, turn your rejection letter into your new plan of action so that you can be more credit-worthy down the road.

2. Address any blind spots on your credit report

Ideally, you should check your credit report three times a year, looking for old accounts that should be closed or inaccuracies which could suggest identity theft. But with so much on your plate as a business owner, keeping up with your credit can sometimes fall by the wayside.

That becomes a real problem when your loan is rejected for reasons that take you by surprise. Credit reports don’t just summarize your active credit accounts and payment history; they also collect public record information like bankruptcy filings, foreclosures, tax liens, and financial judgments. If any of those things are misrepresented on your credit report, it can be tremendously damaging to your chances of securing credit.

Whether inaccuracies occur due to malicious act or accident, it’s ultimately up to you to stay on top of your own credit. Access your credit report for free on AnnualCreditReport.com, and file a dispute with the relevant credit bureau (either Experian, Equifax and TransUnion) if you see anything shady on the report they provide. As credit.com advises:

“If you see any accounts you don’t recognize or late payments you think were on time, highlight them. You’ll need to dispute each of those separately with the credit bureau who issued that report. Even if the same error appears on all three of your credit reports, you’ll need to file three separate disputes over the item.”

3. Pay down outstanding balances

One of the most common reasons for loan rejection is credit utilization—the ratio of your current credit balances to credit limits. This is slightly different than your debt-to-income ratio, which divides your monthly debt obligations by your monthly gross income. Both measurements reflect how much additional debt you can afford to take on, so the lower these ratios are, the better chance you have of being approved for a loan.

Being denied a loan due to your credit utilization or debt-to-income ratio means that lenders aren’t fully confident that you’ll be able to make your minimum payments. There’s nothing to do here except take your medicine: put your new financing plans on hold and focus on paying down your balances until your debt-to-income ratio is below 36.

4. Beware of desperate measures

If you applied for a loan to stave off financial hardship, being turned down can create panic that can lead to some very bad choices. Predatory lenders make their living on that kind of panic, and their risky, high-interest loans almost always leave you worse off than before.

Predatory lenders offer financing that is intentionally difficult to repay. Through their extremely high interest rates, unreasonable terms, and deceptive practices, these lenders force desperate borrowers into a “debt cycle,” in which borrowers are trapped in a loan due to ongoing late fees and penalties. Two of the most common predatory loans are:

Payday loans: These are short-term loans with interest rates typically starting at 390%. (No, that’s not a typo.) A borrower provides the lender with a post-dated check for the amount of the loan plus interest and fees, and the lender cashes the check on that date. If the borrower doesn’t have enough money to repay, additional fees and interest are added to the debt.

Title loans: The borrower provides the title to their vehicle in exchange for a cash loan for a fraction of what the vehicle is worth. If the borrower is unable to repay, the lender takes ownership of the vehicle and sells it.

Please don’t go this route. If your loan rejection has left you desperate for money, swallow your pride and try to borrow from friends and family instead.

5. For thin credit, start small

Being turned down for an “insufficient credit file” doesn’t mean you’re irresponsible—it simply means you don’t have a long enough history of credit maintenance and payments for a lender to make a confident decision about your creditworthiness.

While this situation is very rare for established business owners (who generally have years of credit card and vendor account payments under their belts), young entrepreneurs might not have a long enough credit history to secure the financing they need. If that’s the case, you’ll have to go through the motions for a while: Opening a couple of small credit accounts with easy-to-manage payments will prove to lenders that you have your finances under control.

The Consumer Financial Protection Bureau recommends two low-risk options to build up your credit file: Secured credit cards, in which you put down a cash deposit and the bank provides you with a credit line matching that amount, and credit builder loans, in which a financial institution deposits a small amount of money into a locked savings amount, and you make small payments until you come to the end of the loan term and receive the accumulated money.

6. Wait for the right moment

When you authorize a financial institution to check your credit for a loan application, it typically creates a “hard inquiry” (or “hard pull”) that stays on your credit report for two years. This is different from a “soft inquiry,” which is more commonly used in background checks and pre-qualification decisions, and has no impact on your credit. (Some alternative lenders only use soft inquiries during your application and funding process, so it’s important to find out up front if your lender will be performing a hard credit pull, a soft pull, or both.)

Each hard inquiry won’t affect your credit score much on its own, but multiple hard inquiries in a short period of time can be a major red flag for lenders, who may interpret those inquiries as a sign of financial instability or desperation.

When you’re turned down for a loan, your first instinct might be to immediately apply for a loan elsewhere, in order to get a “second opinion.” The problem is, you may be even less likely to be approved for that next application because you’re racking up hard inquiries on your credit report.

Our advice? Don’t apply for another loan until you’ve made significant improvements to your credit and financial health—a process that can take a year or more. The longer you can wait, the better.

Where to Go When the Bank Says No to a Small Business Loan

After you’ve improved your credit and financial health, you’ll be ready to look for financing options again. When looking for a small business loan, whether for expansion, short-term expenses, or any other, you have more options than just checking with your local bank. Banks and other conventional loan providers have certain criteria when approving your loan. They take into consideration many factors such as the time for which you have been in operation, credit scores, the monthly revenue you earn, your business plan, and the collateral you can provide, among others. If you’re unable to meet their conditions, they may not offer you the finance you need. In such a situation, your best bet is to look to alternative or innovative lending institutions such as Lendio to obtain the funds. Here are some of the best options out there.

SBA or Small Business Administration Loan Programs

The SBA has several small business loan programs for small enterprises, intended to meet their finance requirements. While the government does not lend directly to the companies, it works with microloan providers, banks, and other community development institutions. It supports entrepreneurs by laying down certain regulations for the lending procedures.

- SBA 7(a) Loan Program: A very versatile program, it allows start-ups and small businesses to use these funds for buying machinery, tools, furniture, and other equipment, working finances, buying and renovating fixed assets like structures and other property, among others.

- Real Estate and Equipment Loans: You can use the financing provided under this program only for expansion purposes and to buy land, existing structures, developing, renovating, and constructing buildings, and machinery for use on a long-term basis.

- Microloan Program: By way of this program, small business owners cannot buy fixed assets or pay off loans. They can only use the funds as working capital or to purchase small machinery, tools, and other fixtures. You can also buy inventory, furniture, and other supplies you need.

- Disaster Loans: If you’ve lost property and real estate, inventory, machinery, equipment, or any other supplies in a declared disaster, you can use the business loans provided under this program to replace them. This program offers finance at low interest rates.

Alternative Finance Sources

Aside from banks and the SBA, there are many other sources for getting the funding you need. Look around for the many lending institutions that offer you a small business loan without the strict criteria that banks have. They may be open to providing you business loans despite low credit scores, lack of collateral, or insufficient monthly revenues. However, you might have to pay much higher rates of interest and typically, small business loan terms are shorter than those offered by the SBA. Here are some of them:

- Lending Club: You can borrow funds of up to $35,000 from the other members if you have a credit score of a minimum of 650. Other members lend you the finance you need and can earn up to 9% in interest.

- Prosper: The maximum loan amount offered is $25,000 and borrowers with credit scores of a minimum of 640 can access funds. Lenders can provide loans in smaller denominations until the total amount is raised.

- OnDeck Capital: You can access funds from this source if you can prove that you have been in business for a minimum period of a year and have an annual revenue of $100,000. Apply for the business credit you need over the phone or by filling an application form online. OnDeck makes the loan amount available to you within a day or more.

- Communities At Work Fund: if you can meet their criteria and run a non-profit undertaking, this finance institution extends the funding you need. They direct their support to businesses with low-income and communities in the lower wealth category.

- Accion: Depending on certain conditions, you can get financing of a maximum of $50,000 if you have a credit score of at least 525. At the same time, you must prove that in the last one year, you have not declared bankruptcy and have enough monthly earnings to clear your bills and make payments towards your loan.

Crowdfunding Loans

Crowdfunding loans are similar to microloans, and small business owners that cannot access bank finance can make use of them. However, like microloans, you won’t need to pay back the loan amount in cash. Instead, you’ll need to honor the loan obligation in other ways.

- Kickstarter: This institution issues loan products to companies or creative entrepreneurs for expansion purposes. While you’ll remain the owner of the products you create, you’ll need to prove that your enterprise has the total funding to get started. In lieu of the loan amount, you’ll pay in the form of a product or service your company offers. For instance, if you’re planning to open an art academy, you might have to submit saleable art to pay for the loan.

- Indiegogo: The terms and conditions for accessing this funding are similar to that of Kickstarter. However, you don’t need to have the complete start-up finance in hand to qualify for the business credit.

Entrepreneurs and owners of startup companies no longer need to rely on banks to get the business loans they need. Nor do they need to wait for long processing times and submit elaborate paperwork to get approved. Instead, they can contact many other lending institutions and get the small business loan products they need at terms and conditions that are more suitable for their enterprise and its unique needs.

Lendio is a free marketplace for small business loans. Simply answer a few questions about your business and the amount of capital you are seeking. Lendio will instantly match you with loan options from our network of over 50 lenders. Lendio makes it possible to shop for the best business loan options and rates available without having to submit your information to multiple banks and organizations.

With all of these strategies, it’s helpful to put yourself in the lender’s shoes. Their job is to simultaneously fund small businesses and also safeguard their money. It’s a difficult balancing act, and they likely take no pleasure in rejecting applications. You can make things easier for both them and you by carefully preparing each application and ensuring that you’re giving them ample reasons to give you the green light.

If your loan is approved, throw a little party with your friends. If your application is denied, don’t despair. Remember, the majority of loans are met with a hard no. Take positives from the experience by learning from your mistakes and submitting an even stronger application the next time around. This approach ensures you’ll always be progressing and you’ll eventually get the financing your business requires.

When you review financing options for your business, you’ll likely discover that some lenders want you to sign a personal guarantee. A personal guarantee can help reduce a lender’s risk when it loans money to a business. Yet as a borrower, that same arrangement can put your personal finances in a vulnerable position.

It’s important to understand how personal guarantees work and the risks you’re agreeing to accept before you sign on the dotted line. This small business owner’s guide to personal guarantees will show you the basic details you need to know on the topic. Once you have more information, you’ll be better equipped to make an informed decision about your business financing options.

What is a personal guarantee?

A personal guarantee is a special provision you might find in a business financing agreement like a small business loan, a business line of credit, etc. The provision states that the business owner (or owners) agree to accept personal liability for their company’s debt.

If your business borrows money and fails to repay those funds (plus interest and fees), a personal guarantee allows the lender to go after your personal assets to recuperate its investment. So, at least in some ways, providing a personal guarantee is like agreeing to be a co-signer for your business.

Why do lenders require personal guarantees?

You won’t face personal guarantee requirements with every type of business financing. But many business lenders do ask small business owners for personal guarantees when their companies apply to borrow money. The reason lenders make such requests has to do with risk.

Thanks to how business loans work, there’s a level of risk involved anytime a lender loans money to a borrower. There’s a chance the borrower will fail to repay the debt as promised and that the lender could lose money in the process.

A lender can try to offset this risk and remain as profitable as possible in a few different ways. For example, lenders will review your creditworthiness when you apply for financing. If you or your business have good credit, you might find it easier to qualify for a loan.

Another way lenders can manage risk is by asking business borrowers to provide collateral to “secure” the loan, line of credit, or business credit card they are seeking. And, of course, some lenders ask for personal guarantees to encourage business borrowers to repay their debts (and to provide additional resources for collections if they don’t).

Pros and cons of signing a personal guarantee.

There are benefits and drawbacks to signing a personal guarantee. Here are some of the pros and cons you should consider before you agree to put your name (and personal assets) on the line for your business.

Pros

- There may be more financing options available to your business if you sign a personal guarantee—especially if you have good personal credit.

- You might have better approval odds if you’re willing to sign a personal guarantee.

- Signing a personal guarantee might help you lock in a better interest rate for small business financing.

- Your business might be able to get a loan without collateral if you provide a personal guarantee.

Cons

- You risk losing your personal savings, home, vehicles, and more if your business defaults on its debt.

- Your personal credit score and credit history could be damaged if the business falls behind on its credit obligation—and your business credit might suffer, too.

- Even if you sell the business (or sell your interest in the business), your personal guarantee on a debt will likely carry on until the account is closed and satisfied in full.

No one can predict the future. Should your business be unable to repay its credit obligations for any reason, you could pay the price with your personal wealth, if you agreed to sign a personal guarantee. If that risk makes you uncomfortable, you should probably search for other ways to finance your business.

Ways to avoid personal guarantees.

Many lenders ask for personal guarantees when you apply for business loans—especially if your business is still in the startup phase. But if you’re wondering how to get a business loan without signing a personal guarantee, there may be other options available to you.

- Work on establishing good business credit. Building business credit is a process. So, the sooner you can start, the better.

- Search for loans without personal guarantee requirements. With certain types of business loans, like SBA loans, personal guarantees are not negotiable. Yet a few lenders may be willing to loan your business money without requiring a personal guarantee in return. However, every lender is different. So, if you prefer a business financing option that you can obtain in your company’s name—instead of your own name—be sure to do your homework.

- Supply collateral. If your business has collateral that it can pledge to secure a loan, those assets could reduce the risk involved for the lender. As a result, your company might find it easier to find secured financing options without a personal guarantee than unsecured financing.

- Consider a blanket business lien. Another way to reduce a lender’s risk when you borrow money is to sign a blanket business lien. A blanket lien gives the lender permission to take possession of all of your company’s assets and resell them in the event of a default. Agreeing to a loan offer that includes a blanket lien is also a high-risk way to secure financing, but it’s the business—rather than the business owner—that’s absorbing most of the risk in this scenario.

- Be aware of a confession of judgment. A confession of judgment is an additional document provided as part of your loan contract package that waives the business owner’s right to a legal defense before a court and allows a lender to go after a business’s assets if the business defaults on the loan. Including this clause is illegal in some states and Lendio does not work with lenders that include one.

It can be difficult to borrow money for your business or even establish business credit without accepting some personal liability in the process. Lenders tend to be more comfortable working with companies when business owners are willing to put some “skin in the game.”

However, it’s not impossible to find alternative financing solutions that do not require personal guarantees, if this is the borrowing approach you prefer.

Consider the benefits and drawbacks of accepting personal liability for business debts up front. Some business owners are comfortable with taking on personal risk in exchange for more attractive financing options. Others are not. Only you can decide whether a personal guarantee is something that you’re willing to chance for the sake of your company.

There are numerous ways to secure business capital, and debt financing is at the top of that list. With debt financing, your business borrows money from a lender—often in the form of a short term loan or business line of credit—and agrees to repay those funds plus interest in the future.

The right business loan or line of credit can come with many benefits. Business financing might enhance your cash flow, provide you with working capital, or give your company the financial flexibility it needs to expand.

Yet it’s also important to understand what your business will be agreeing to repay when it borrows money, and how that new debt relates to what your business already owes. Therefore, it’s wise to calculate the cost of debt before you seek new business financing.

What Is Cost of Debt?

When a lender or debt holder extends credit to a business, it’s making an investment on a future return. In other words, the lender expects to receive compensation for the risk it’s taking at some point in the future.

Cost of debt is the term that describes how companies repay the lenders and creditors from which they borrow money. Cost of debt is the effective interest rate a company pays to creditors—also known as debt holders or lenders.

Others may want to know your company’s cost of debt figures, because it can help them assess the risk of doing business with your company. For example, if your business is trying to attract new investments or apply for certain types of financing, investors or lenders may want to know your company’s cost of debt to assess the financial stability of your business.

As a business owner, you may want to calculate cost of debt as well. Knowing your cost of debt can help you make sure your current business debts aren’t putting your company under too much pressure and can help you to determine whether or not it’s wise to borrow additional money for your business.

How to Calculate Cost of Debt

Before you calculate the cost of debt for your company, you will need to gather some information. Here’s what you need to get started:

- A list of the outstanding debts your business owes.

- The APRs your business owes on each of its debts.

You may have to estimate some of the figures above, since the debt your business carries throughout the year may fluctuate. This may be especially true if you have business lines of credit or business credit cards with revolving balances. Your overall debt figures may also experience some variations depending on whether you have fixed or variable interest rates.

Next, it’s important to understand that there are multiple ways to calculate cost of debt. Two of the most common approaches to the cost of debt formula are to calculate the after-tax cost of debt and the pre-tax cost of debt. Below is a closer look at the cost of debt formula for each option.

Pre-Tax Cost of Debt

To figure the pre-tax cost of debt for your business, start by adding your total interest expenses for the year. Then, divide that figure by your total number of business debts.

| Total Annual Interest Expense / Total Debts = Pre-Tax Cost of Debt |

Here is an example.

Imagine your business has three debts:

- Business Loan A: $50,000 at 4% APR

- Business Loan B: $50,000 at 7% APR

- Business Loan C: $100,000 at 5% APR

In this scenario, then, your total debts would equal $200,000.

Next, assuming the loans above all have fixed interest rates, you would calculate the total annual interest expense as follows.

- $50,000 X 4% = $2,000

- $50,000 X 7% = $3,500

- $100,000 X 5% = $5,000

Add up the three interest amounts for the debts and your total annual interest expense would equal $10,500.

Finally, you input all of the figures above into the cost of debt formula.

| Total Annual Interest Expense ($10,500) / Total Debts ($200,000) = Pre-Tax Cost of Debt (0.0525 or 5.25%) |

In the example above, the pre-tax cost of debt—also known as the effective interest rate—that your business is paying to service all of its debts throughout the year would equal 5.25%.

After-Tax Cost of Debt

Now let’s consider the after-tax cost of debt. The after-tax cost of debt is how much your business pays for its debts after you factor in the cost of taxes.

Many interest charges are tax deductible for businesses. (Note: You should talk to a reputable tax advisor for advice on any specific tax-related matters.) So the after-tax cost of debt calculation is the more common figure that business owners, lenders, and would-be investors will likely want to review.

To calculate the after-tax cost of debt, you will need to use the following formula.

| Effective Interest Rate X (1 - Tax Rate) = After-Tax Cost of Debt |

As you can see, this formula picks up where the pre-tax cost of debt formula left off. In other words, you must use the first formula to calculate the effective interest rate before determining the after-tax cost of debt.

Below is an example of an after-tax cost of debt calculation to help you visualize how the process works.

Building on the example above, let’s still assume that your business has an effective interest rate of 5.25%. Since tax rates vary for different businesses, for the sake of this exercise, let’s also just assume that your business is paying a 9% corporate tax rate.

Now, let’s take a look at how the numbers align in this hypothetical after-tax cost of debt calculation.

| Effective Interest Rate (5.25%) X (1 - Tax Rate) (1 - 9%) = After Tax Cost of Debt (0.0477 or 4.77%) |

So, in the example above the after-tax cost of debt is 4.77%.

Why Does Cost of Debt Matter?

Choosing the right financing solutions for your company can have a meaningful impact on its bottom line. Avoiding financing can stall business growth and cause you to miss out on valuable opportunities for growth and expansion. Yet, if you overextend your business financially and its cost of debt grows too high, that can create problems of its own. Therefore, it is important to take the time to do some careful research before you seek financing and find the right balance that works for you.

A commercial loan is a type of financing available to businesses. General commercial loans can be used for any business-related expense, from payroll costs to expanding to a new location. There are also specialized loans used for specific purposes, like buying equipment or acquiring another business.

Read on to learn more about how commercial loans work and how to choose a financing structure that best meets your business needs.

Commercial Loan Definition

So what is commercial financing? It's when a business borrows money from a financial institution. Here's how commercial loans work. The business receives a lump sum to be used at the owner's discretion. The funds are then repaid over time according to the conditions of the loan agreement. The lender charges interest that is added to the loan balance and included in the payments. Depending on the type of commercial loan, payments could be made daily, weekly, or monthly.

In order to qualify for a commercial loan, businesses apply using their credit scores (often including the owner's personal credit score), revenue, and time in business. Different lenders may have different requirements and request additional types of documentation. They may also request that you offer some type of asset as collateral for the loan.

4 Types of Commercial Loans

These are four of the most common types of commercial loans to consider as a starting point for your business financing needs.

SBA Loans

Government-backed SBA loans help connect businesses with financing opportunities for a number of different purposes. These types of loans are notorious for their lengthy application review periods, which can stretch out several months. Loan amounts go as high as $5 million, with competitive interest rates and repayment terms that can last anywhere between 10 and 30 years. Most SBA loan programs also require a 20% down payment on the loan so that you're heavily invested in the success of the business.

There are several different types of SBA loans to consider. A 7(a) loan is the most common one and the funds can be used for general purposes. Smaller 7(a) loans (under $25,000) don't require any collateral. SBA 504 loans are used to purchase a specific asset, like a building or machinery.

Term Loan

Term loans can either be short-term (lasting less than two years) or long-term (lasting as long as 25 years). In most cases, these loans come with a fixed interest rate and consistent monthly payments so you know exactly what you'll pay back each month. If you use an online lender, you can often get approved and funded in just a couple of business days, making these an attractive option for businesses needing fast cash. A term loan can also help you better predict cash flow since the payments are consistent each month.

The application process varies depending on the lender. A traditional financial institution, like a bank, may have a longer review process compared to an online lender. Also find out how long it takes to receive funds after your application is approved.

Commercial Real Estate Loan

Also called a commercial mortgage, a commercial real estate loan is designed to help your business purchase property. This could be an office building, retail store, warehouse, manufacturing facility, restaurant space, or other type of real estate. Loan amounts are typically large and the term length is extended to make payments more affordable.

In addition to purchasing a property for your business, you can also use a commercial real estate loan to refinance the terms of an existing commercial mortgage or renovate a property you already own. If you dream of owning or expanding space for your company, a commercial real estate loan can help you do that.

Business Line of Credit

Rather than giving your business a one-time injection of capital, a business line of credit gives you access to credit when you need it over a period of one to two years. It acts like a credit card in that you can draw on your credit line as needed and pay interest on your balance, rather than the entire available amount.

A business line of credit can be an ideal type of commercial financing in a number of scenarios. For starters, a line of credit can be used for financial emergencies, like broken equipment that needs to be replaced. It can also help cover ongoing expenses, like payroll, especially if your revenue is inconsistent throughout the year. Finally, a line of credit gives you agility to act on opportunities as they arise, without having to apply and wait for financing in the future.

Pros of Using a Commercial Loan

Business loans can be a great way to manage and grow your company. Here are some of the primary benefits of using a commercial loan.

Access to capital: When your business’ current cash flow is not enough to get through slow periods or ramp up for busy seasons, getting a commercial loan gives them access to the capital to do so. And because there are so many different types of business loans out there, you can find one that's structured for your business needs.

Faster growth: Taking on debt doesn't automatically mean your business is in trouble. In fact, many businesses often use debt to accelerate growth and take advantage of new opportunities to expand.

Retain full ownership: There are many ways to raise funds for your company, including taking on external investors. But with a commercial loan, you get to retain full ownership of your company.

Cons of Using a Commercial Loan

There are downsides to consider as well before you decide to apply for a commercial loan.

Application process: The application process can be intimidating, and there's no guarantee you'll get approved. Be prepared to put in a little elbow grease. But if your business financials are already in order, then you may not have much to worry about.

Interest and Fees: There's no such thing as free money, and you'll have to pay interest and fees on your borrowed funds. Weigh the benefits you expect to receive and make sure you can afford the payment terms, even in a worst-case scenario.

Cash flow crunch: Making loan payments can be tough on your cash flow. Consider all the obstacles your business may face and how well you could maintain those payments before making a decision on your business loan.

Does commercial financing sound like a good fit for your business?

Apply for a small business loan and compare offers with Lendio.

Re-entering the workforce can be difficult after serving jail time as a convicted felon. Not only do felons lose their ability to vote and serve on a jury, they can also have difficulty finding a job to support a new positive lifestyle. Starting a business may be an opportunity to start fresh, but there may be some roadblocks when it comes to scaling growth. Understanding small business loan opportunities for felons can make the path to successful financing much easier.

Small business loans for felons.

Felons will have a harder time finding loans they are eligible for, but there are still some limited options available through the SBA.

SBA loans

SBA loans are backed by the Small Business Administration, which incentivizes lenders to work with qualified borrowers. Felons aren’t automatically denied, but there is an additional form you’ll have to fill out to be evaluated by your lender. Keep in mind that not all lenders who offer SBA loans will work with felons, and those who do will have very strict requirements.

Qualification questions include if the applicant is currently facing charges (an automatic disqualification), if they have been arrested in the past six months, convicted of or pled guilty or no contest to a crime, or are currently on parole or probation. The applicant is then required to provide details regarding the charges and sentencing along with documentation that all fines and court conditions have been met.

There are a variety of SBA loans to explore, which can be used for things like purchasing real estate, buying equipment, or expanding or purchasing a new business. Most SBA loans are designed for established businesses rather than start-ups.

Grants & other financial resources for felons.

In addition to taking out a business loan, it’s also worth exploring alternative options to raise capital for your company, including grants, investors, and crowdfunding.

Federal grants

Businesses owned by convicted felons are eligible for federal grants from Grants.gov. That’s because eligibility is based on the business’s background and proposals, not personal finances or history. Business grants are different from loans in that they don’t need to be repaid. Grants are listed on behalf of federal agencies, like the National Institutes of Health or the Environmental Protection Agency, to perform work or research on their behalf.

State grants

There are a number of state resources available through individual states. Most states have an economic development administration that receives federal grant funding to pass on to small business owners. Some of these may be specific to regional areas; for instance, you may find funding opportunities if your company operates in a designated rural region.

Entrepreneurship programs

Large corporations often sponsor programs to help launch and scale emerging businesses. They might provide grant funding or provide free products and services. FedEx, for example, hosts an annual program in which the winners are awarded a cash grant, plus services from FedEx.

Angel investors

Angel investors are private individuals who use their own wealth to fund companies, often in exchange for equity. They’re currently the largest source of business capital in the U.S. And while you may need to disclose your criminal history as part of your pitch, they’re typically more focused on your business concept and growth opportunities than your background. There are several online platforms that connect entrepreneurs with angel investors, and of course, it’s also good to network locally.

Crowdfunding

Two of the most common types of crowdfunding campaigns are rewards-based crowdfunding and equity crowdfunding. With the first option, you post a business idea and seek funding from individuals in exchange for a tiered system of rewards. With equity crowdfunding, you take money in exchange for partial ownership of the company. Most crowdfunding platforms require you to set a financial goal and won’t release any funds unless contributions reach that amount.

Resources for felons

HelpforFelons.org

HelpforFelons provides information and resources on how to find a job, housing, or start your own business when you have a criminal record.

Inmates to Entrepreneurs

Inmates to Entrepreneurs offers a free eight-week course to anyone with a criminal background who is interested in starting their own business.

freegrantsforfelons.org

This online resource provides information on housing, education, and jobs for felons.

Note: Lendio itself does not offer or issue small business grants. Instead, Lendio is a lending marketplace that connects business owners with 75+ lenders for business loans, SBA loans, lines of credit, and more. The grant resources in this article are external resources for business owners.

If you’re looking to make a significant investment in your business, you might consider applying for a long-term business loan. These loans come with low interest rates and fixed repayment terms, so they’re a stable form of financing for companies of all sizes.

However, it’s important to understand the different types of long-term loans and long term financing available and the pros and cons of taking one out. This article will serve as a guide to finding and applying for a long-term business loan.

What Are Long-Term Business Loans?

A long-term business loan is a loan you’ll repay over a specific period of time. The average repayment term lasts between 5 and 7 years, but some loans come with terms up to 25 years.

Long-term loans are typically used to finance a major investment in the company—for example, for the purchase of real estate or equipment, or the hiring of additional employees. When you take out a long-term business loan, you’ll receive the money for such a purchase in one lump-sum payment, which you’ll then repay over time.

These loans are usually best for established businesses with good credit history. And the application process can be quite lengthy—when you apply, you can expect to submit the following documentation:

- Social Security Number

- Personal and business tax returns

- Personal and business bank statements

- Employer Identification Number (EIN)

- Proof of business registration

- Business plan

- Profit and loss statement

- Cash flow statement

- Balance sheet

Long-Term vs. Short-Term Business Loans

| Long-term business loans | Short-term business loans |

| Interest rates are usually low. | Interest rates are typically higher than those of long-term loans. |

| Repayment terms are typically between 5 and 7 years. | Repayment terms are usually less than a year. |

| Required documentation is usually extensive. | Application process is less intensive, because the loan amounts are smaller. |

| Only established businesses with excellent credit tend to qualify. | Startups and individuals with poor credit are more likely to qualify than with long-term loans. |

Occasionally, your business may need a quick infusion of cash to help you get through payroll or manage your working capital needs. In this scenario, it may make sense to apply for a short-term business loan.

The biggest difference between short-term and long-term business loans is that long-term loans are designed for long-term investments. In comparison, short-term loans can help you meet your immediate financial needs.

Short-term business loans are usually available in smaller amounts and have to be repaid in less than a year. These loans also typically come with higher interest rates than long-term business loans.

However, the application and approval process is less extensive than that of long-term loans. And it may be easier for startups and borrowers with poor credit to qualify for a short-term business loan.

Types of Long-Term Business Loans

There are several different types of long-term small business loans available depending on your business’s needs. Here are four different loan types you can choose from.

SBA loans

An SBA loan is a business loan that’s backed by the Small Business Administration (SBA). Since the SBA partially guarantees the loan, this lowers some of the risk to lenders.

And these loans often come with low interest rates and lengthy repayment terms. SBA loans come in all shapes and sizes, with loan amounts between $500 and $5.5 million and repayment terms between 5 and 25 years.

However, SBA loans can be difficult to qualify for and the approval process can take a long time. If you decide to go this route, you should expect to provide your lender with extensive paperwork. And it may take several months for you to receive the funding for your loan.

Bank Loans

Another option is to apply for a term loan through a bank. Like SBA loans, bank loans come with low interest rates and lengthy repayment terms, making them an affordable way for small businesses to get access to financing.

However, these loans are best for established businesses with excellent credit history. You can expect to provide a lot of documentation when you apply, and the approval process will take longer than other types of loans.

Equipment Financing

Equipment financing is a form of business financing that’s used to purchase business-related equipment or machinery. These loans can be a good option for heavy equipment needs, like restaurants and manufacturing and construction firms.

This business financing allows you to purchase the expensive equipment you need, and break the cost into manageable monthly payments. And since the equipment serves as collateral for the loan, equipment financing may be easier to qualify for.

Commercial Real Estate Loans

A commercial real estate loan is a loan used to purchase property for your business, like an office, warehouse, or retail location. These loans are offered by the SBA, banks, credit unions, and online lenders.

Commercial real estate loans can be used to purchase new property, renovate an existing location, or even refinance your real estate debt. These loans are available up to $2 million, and usually come with repayment terms between 5 and 20 years.

Pros and Cons of Long-Term Business Loans

A long-term business loan can help you finance a major business investment, but it isn’t the best choice for everyone. It’s important to understand the pros and cons of these loans before applying.

Pros

- These loans typically come with lower interest rates and fixed payment terms.

- Long-term business loans come with low fees compared to other types of loans.

- Most lenders don’t put any restrictions on how you can spend the funds.

- These loans can help you build your business credit.

Cons

- These loans come with a lengthy approval process, especially if you apply for an SBA loan.

- It may be hard for borrowers with poor credit to qualify for a long-term business loan.

- Lenders usually prefer to give long-term business loans to established businesses.

- You may be required to put down some type of collateral to secure the loan.

How to Qualify for a Long-Term Business Loan

Here are the four steps you’ll take to apply for a small business loan.

Decide Which Type of Loan You Need

There are several types of long-term business loans you can choose from. The one that’s best for you will depend on where you’re at in your business and what you plan to use the funds for.

For instance, if you’re an established business and are looking for low rates and flexible repayment terms, you may want to consider a bank or SBA loan. If you need to purchase equipment or large machinery, then equipment financing may be the right choice for you.

Start the Application Process

Once you know what type of loan you need, you can start the application process. Depending on the type of lender you work with, you’ll either complete this online or in-person.

When you apply, the lender will ask for some basic information about you and your business. They will also check your credit score to determine how risky you are as a borrower. A low credit score doesn’t necessarily rule you out from qualifying for a business loan, but you may receive a higher interest rate.

Provide the Necessary Documentation

Next, you’ll have to go through the approval process and provide the necessary documentation. The exact documents required and timeline for approval will depend on the lender you’re working with.

For instance, online lenders tend to offer a shorter approval process and faster funding. Whereas if you’re applying with a bank or the SBA, you can expect the approval and funding process to take much longer.

Compare Your Options

And finally, you don’t want to just take the first business loan that’s offered to you—it’s a good idea to compare loan offers from several different lenders. Comparing your options will help you find the loan with the best rates and terms. You should also consider any fees those lenders charge, like origination fees, late fees, and prepayment penalties.

Comparing your loan offers is easier when you use a service like Lendio. With Lendio, you apply for a loan once and receive offers from multiple lenders.

The Bottom Line

A long-term business loan is a loan that’s repaid over a specific period of time. You’ll receive a one-time lump sum payment, which you can use to invest in long-term business growth.

If you’re looking for a way to compare small business loan options, you may want to consider using Lendio. We offer a variety of small business loans, including SBA loans, term loans, cash advances, and much more.

We offer a secure online application process, and you’ll receive loan options from our network of over 75 lenders. This will help you find the right business loan for your situation.

What about your credit score? Whether you apply for financing for your small business or for a personal purchase, lenders will probably want to check your credit score before determining financing options. If this seems a little off-putting to you, don't be too concerned. The more you know about how your personal and business credit scores are used, the more prepared you’ll be for this sometimes stressful step.

What is a personal credit score?

A personal credit score is a number intended to serve as an indicator of how likely you are to pay what you owe. It’s based on a number of factors including:

- how long you’ve maintained a credit-based product (like financing or a credit card)

- how often you use your credit

- how quickly you pay back what you owe

- how many times you’ve been late in paying back what you owe

Your personal credit score is expressed as a three-digit number between 350 and 800. The higher the number, the better your credit score is.

What is a business credit score?

A business credit score is calculated using roughly the same criteria as a personal credit score calculation, but with a few more factors:

- how long you’ve maintained a credit-based product (like a business loan or a credit card)

- how often you use your credit, how quickly you pay it back and how many times you pay late

- how many times you were late paying your rent or your mortgage, your vendor bills or your staff

- your personal credit score

Your business credit score is expressed as a two-digit number between 00 and 99. Again, the higher the number, the better your credit score is.

And note that personal credit score is a factor in calculating your business credit score. This isn’t the case the other way around, and the reason it’s a factor is because lenders will want to know that the person they’re trusting with their money has a personal history of responsible debt service.

Who determine your personal and business credit scores?

| Personal | Business | |

| Agencies involved | Equifax, Experian, and TransUnion | Equifax, Experian, and Dun & Broadstreet |

| Where info comes from | Public and court records, credit card issuers, lenders, and collection agencies | Public records, lenders, vendors, and personal credit reports of the owners |

| Impact of late payments | Payments more than 30 days late appear on the report | Both late and early payments are recorded, regardless of how late or early |

Why will business loan providers look at both personal and business credit scores?

Lenders and financiers may be looking for a number of things when checking credit scores, but at the heart of their research is the fact that they're attempting to assess the perceived risk of lending money to the applicant. Credit scores were developed as a fast means of identifying the risk. Note that different lenders may assess risk uniquely — credit scores are not the only factor consider by most lenders.

How do good and bad credit scores positively or negatively affect a business?

The major benefit of a good credit score is an easier path to securing financing you might need for your business. Frequently, a higher credit score is assigned a lower interest rate because the risk of the applicant is considered lower low risk. It may also be a factor in how much financing your offered and the type of financing, too, while a not-so-perfect credit score is perceived as a greater risk.

Can a bad credit score get better?

Yes, a bad credit score isn’t like a scarlet letter. Try these tips for improving your business credit score. For personal credit, paying bills on time, paying down credit cards and any outstanding loans, and not applying for credit for a year are just some of the strategies that will have a positive impact on your credit score.

Can a company with a bad business credit score still get financing?

Whether or not your credit score will allow you to borrow money often depends on the lender and the type of financing offered. Since lender requirements vary, the best way to find out if you're eligible is to apply to see what's available. A financing marketplace like Lendio simplifies the process by starting with a 15-minute online application that doesn't negatively impact the applicant's credit score. Additionally, Lendio's system works with more than 75 lenders and 10+ financing options, so you can find out quickly (and painlessly) what's available to your business.

Disclaimer: The views and opinions expressed in this blog are those of the authors and do not necessarily reflect the official policy or position of Lendio. Any content provided by our authors are of their opinion and are not intended to malign any religion, ethnic group, club, organization, company, individual or anyone or anything.The information provided in this post does not, and is not intended to, constitute business, legal, tax, or accounting advice and is provided for general informational purposes only. Readers should contact their attorney, business advisor, or tax advisor to obtain advice on any particular matter.