As a small business owner, financing backed by the U.S. Small Business Administration (SBA) represents some of the most affordable types of business loans available. SBA loans are a popular option for both startups and established businesses alike. These loans tend to feature low interest rates, higher loan amounts, and generous repayment terms compared to other business loan options.

At the same time, understanding how to apply for an SBA loan and qualify for this type of financing can be complicated. The SBA loan application process can be tedious, and if you don’t complete it properly, you could hurt your chances of getting a loan approval.

That’s why Lendio has put together a complete guide to applying for an SBA loan, including types, requirements, the application process, and how to improve your chances of approval.

Step 1: Decide which type of SBA loan you need.

There are several different types of SBA loans available to small businesses. With SBA loans, your business may be able to borrow up to $5 million and repay those loans over a period of 10 to 30 years. (Repayment terms can vary.)

You can find SBA loans to help you finance many different aspects of your business needs. Whether you need startup funding, working capital, equipment financing, inventory financing, or funding for some other type of business need, you may be able to find an SBA loan to support your goals.

First, Ask yourself a few key questions about your business needs to find the right SBA loan program for your needs, like:

- How much funding do I need?

- What will I use the funding for?

- What is the minimum repayment term I need to work with?

Once you figure out the type of SBA loan you want, you can determine if your business is eligible for the loan program.

Step 2: Check eligibility requirements

The specific eligibility requirements that your business needs to meet in order to qualify for an SBA loan will vary based on a few factors. First, each SBA loan program has unique requirements you must meet to qualify. In addition, you may need to satisfy additional loan requirements that your SBA-approved lender requires from small business borrowers.

The minimum requirements for most SBA loans are as follows.

- Be an operating business

- Operate for profit

- Be located in the U.S. or in U.S. territories

- Can meet SBA “small business” size requirements

- Not be a type of ineligible business

- Be creditworthy and demonstrate reasonable ability to repay the loan

- Collateral to secure a large percentage of the loan

- Unable to access business financing through non-government means (not including personal funds)

If you meet these requirements, then the next step is confirming that you qualify with an SBA lender, and this is where it can get complicated. Let’s go over some major eligibility requirements with most SBA-approved intermediary lenders as lender standards vary.

Creditworthiness Requirements

SBA 7(a) loans and SBA 504 loans are issued by traditional lenders, so they will have more stringent credit criteria than other loans, like microloans.

Most lenders for these loans will want to see a FICO® credit score of 650 or above.

On the other hand, SBA microloans have less strict credit criteria, and you may be able to qualify with limited credit history.

Time in Business Requirements

Like credit criteria, SBA 7(a) loans and SBA 504 loans will require more time in business and proof of revenue than microloans.

Most lenders will want to see at least two years in business for 7(a) and 504 loan applicants. In contrast, lenders may not require as much time in business for the microloan program, with some lenders only requiring six months in business.

If you meet these eligibility requirements, the next step is to gather all the documentation you will need for the application process.

Step 3: Prepare documentation for SBA loan application

Before you apply for an SBA loan, it’s important to gather the documentation your lender will request on your application. The time it takes to move through the SBA process from application to funding will vary.

While it might take 30 to 90 days with your local bank, Lendio, on average, can close an SBA 7(a) small loan in less than 30 days. Having your documents prepared ahead of time may help improve your chances of approval and could help you move forward through the SBA loan process at a faster pace.

Below is a list of the documents you should prepare for your SBA loan application:

- Six months of business bank statements (connect account or manually upload images)

- Copy of your driver’s license or state ID

- Voided check from your business account

- Month-to-date transactions

- Two years of business and personal tax returns (for all business principals with 20% or more ownership)

- Debt schedule

- Year-to-date profit and loss statement

- Year-to-date balance sheet

- Cash flow projections

- List of collateral

- Business certificates or licenses

- Loan application history

- Business owner resume(s)

- Business plan

- Business lease, if applicable

Additional SBA loan application requirements.

In addition to the documents listed above, you should be prepared to include more information on your SBA loan application. Details you may need to provide include:

- The amount of money you want to borrow.

- The purpose of the loan and how you plan to use the proceeds if approved.

- Assets you need to purchase and the name of your business suppliers.

- When your business started.

- General information about your business (owners, affiliations, etc.).

- Your birthday and your Social Security number

- Details regarding other business debts and your creditors.

Anyone who owns 20% or more of the business will generally need to fill out an SBA loan application form, as the SBA requires that anyone with 20% or more ownership in the business provide an unlimited personal guarantee.

Owners with less than 20% ownership can provide full or limited guarantee. Owners will also need to complete a personal financial statement, called SBA Form 413. SBA uses the personal financial statement to assess risk and help determine an applicant’s ability to repay as promised.

Here's a list of SBA-specific forms to include in your application package:

- SBA Form 1919 - Borrower Information Form

- SBA Form 912 - Statement of Personal History

- SBA Form 413 - Personal Financial Statement

- SBA Form 148 - Unconditional Guarantee (or lender’s equivalent to this form.)

- SBA Form 148L - Limited Guarantee (or lender’s equivalent) for owners with less than 20% ownership

Step 4: Find an SBA-approved lender

You can use an SBA loan to support your small business in many different ways. Once you feel ready to begin your SBA loan application, you can start by choosing an SBA lender to guide you through the process.

Depending on the type of SBA loan program you are applying for, you might have a few different options for finding an intermediary lender. Since SBA 7(a) loans and SBA 504 loans lenders are more traditional financial institutions, you can try reaching out to a bank you have a previous relationship with.

The SBA also offers a few resources for finding active certified development companies (cdcs) and active microlenders on their website.

If you would like to connect with lenders directly, you can use the SBA’s lender match system. You’ll fill out a questionnaire about your business, and in two days, you’ll receive an email with possible lender matches.

Lendio offers a convenient SBA loan application process. Potential borrowers can complete an application and get a preapproval within 24 hours, and after providing the documentation listed above, can get funded with a 7(a) small loan in less than 30 days.

Step 5: Submit your SBA Loan Application Package

Once you’ve prepared your loan application package, it’s time to submit it to the lender. Don’t be surprised if they may follow up with questions, or request for additional documents. Every lender has different requirements, so work with your contact to provide everything they need to begin the initial underwriting process to review your application.

If your lender decides to move forward, you can expect a “loan proposal” or “letter of intent” to follow. This document will detail your request, loan terms, and deposits, fees and/ or closing details.

If you accept and sign the proposal, you’re not out of the woods yet. Your lender will begin a formal underwriting process, in which both the lender and the SBA review your application, documentation and credit history thoroughly.

If you are approved after this process, you will be notified and provided a letter of commitment. You must accept it in order to receive closing documents and start the closing process. Once everything is signed and the process is complete, your money will be disbursed.

What to do if your SBA Loan application is denied

Although it's not the outcome you want, only about one-third of SBA loan applicants were fully approved in 2023. A decline is not uncommon, so knowing your options if this happens will help you plan for your next steps.

If your application is denied, your lender will provide you with a letter explaining the reason you were denied, and may provide some options for you after that. You may be able to appeal the decision, for example, and your lender can provide insight.

Read our guide on common reasons why your SBA loan application may have been declined, and what to do next.

Alternatives to SBA Loans

If you aren’t able to find a workaround in the event that your SBA loan was declined, or if you aren’t confident you meet the eligibility requirements, here are some other alternatives to consider:

- Equipment financing- if new equipment upgrades, repair or replacement is what you need, consider exploring term loans or leases for equipment.

- Term business loans - If you don’t qualify for an SBA loan, you may still be able to obtain a business loan paid off with equal payments at a fixed rate through other lenders.

- Business lines of credit- Opening a line of credit enables you access to funds that you can borrow anytime up to your credit limit.

Business loans are crucial for helping small businesses thrive by providing the necessary capital to cover startup costs, invest in inventory, or upgrade equipment. For many small business owners, these loans are not just a means to an end; they are a lifeline that enables them to seize growth opportunities and navigate the challenges that come their way. Therefore, it is vital to understand the current lending landscape that small businesses are facing.

Key stats.

- 68% of small business owners say access to financing is the most important factor in the growth of their businesses.

- 67% of small business owners have no preference about which type of lender they get a loan from.

- 85% of small business owners said that speed to loan approval is important when selecting a lender.

- 77% of small business owners surveyed stated that they prefer to apply for a loan online or via a mobile app.

- 50% of small businesses say they don't know if the bank they use for checking has the right loan options for them.

- Only 24% of small business owners apply through the bank they already work with.

- The average small business loan is $38,000.

- 59% of SBA loans are approved.

High-level overview.

Lendio recently surveyed 1000+ small business owners to better understand how financing affects the success of their business, their experience in today's lending environment, and how they view the future of small business lending. Of those small business owners, 68% said that access to financing is the most important factor in the growth of their businesses. Additionally, 46% of those 1000+ small business owners said they would see anywhere from 30-100% revenue growth if they had access to financing their business needs.

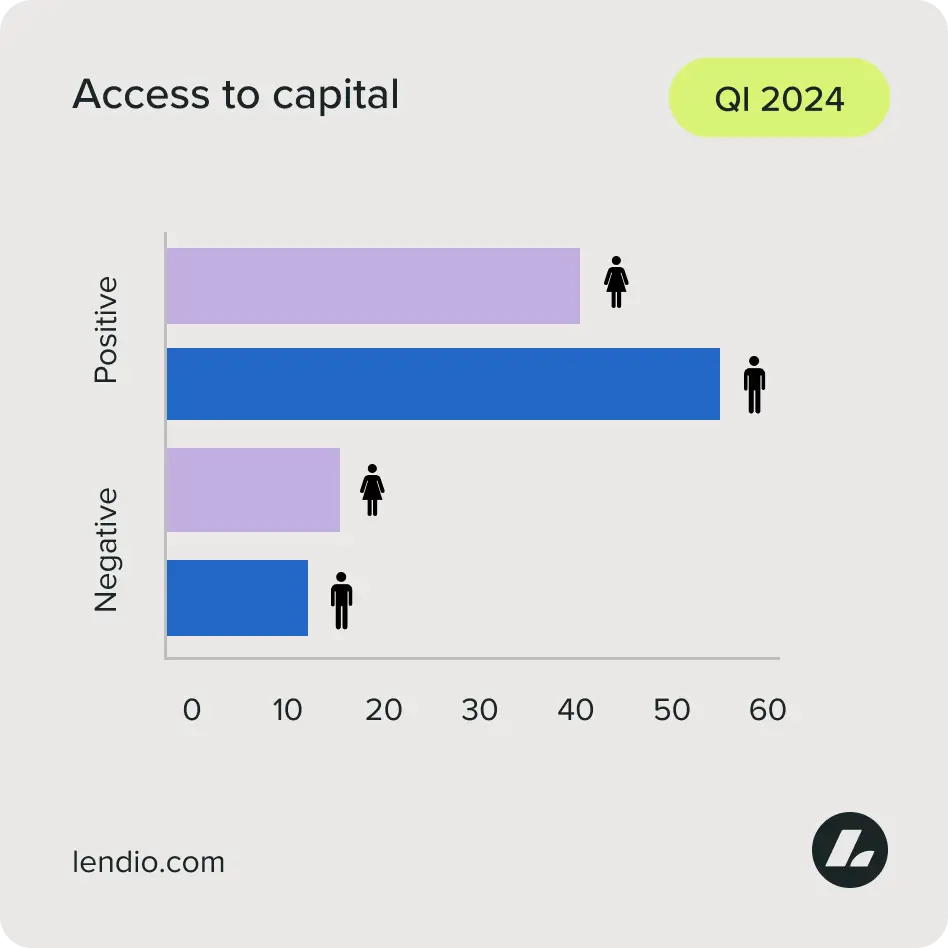

Lendio found that 78% of the small businesses it interviewed have a positive outlook on their ability to access capital in the next year. Perceptions vary based on how well-qualified the small business is for a loan. Only 12% of the most qualified borrowers stated that the majority of small businesses don't have access to the capital they need while 21% of the least qualified borrowers said the same.

Lendio found that while small business owners generally have a positive outlook on their ability to access capital, they have a fairly neutral perception of the loan application process. When asked which type of lender they'd prefer 67% of small business owners said they have no preference.

The takeaway:

85%

of small business owners say speed to loan approval is important when selecting a lender.

While larger enterprises are willing to experience lengthy loan approval and funding processes, small business owners behave more like consumers--they prefer a quick and easy loan process.

- 85% of small business owners said that speed to loan approval is important when selecting a lender.

- 77% of small business owners surveyed stated that they prefer to apply for a loan online or via a mobile app.

Lendio also found a general lack of awareness of the small business loan process.

- 50% of small businesses say they don't know if the bank they use for checking has the right loan options for them.

- Only 24% of small business owners apply through the bank they already work with.

- Lendio found that 22% of small business owners either don’t know or don’t have a preference for their preferred type of business financing.

These findings point toward a need for more education about the lending landscape for small business owners.

Average business loan amount.

Understanding the average loan amounts small businesses receive is critical for entrepreneurs seeking to plan their financial strategies effectively. Businesses should be aware of not only the amounts they might qualify for but also how these figures align with their growth aspirations and operational needs.

- The average amount a small business receives through Lendio’s marketplace is $38,000.

- The average SBA loan amount in 2023 was $479,685.

- On average, small businesses are offered 50% of the loan amount they initially asked for.

SBA loan approval rates.

The Small Business Administration (SBA) plays a vital role in supporting small businesses by providing access to loans with favorable terms. In 2023, approximately 59% of SBA loans were approved (34% received full approval, 25% received partial approval), indicating that over half of small business owners successfully navigate the application process. This is particularly encouraging for entrepreneurs who might face challenges securing traditional financing, as SBA loans often come with lower interest rates and longer repayment terms.

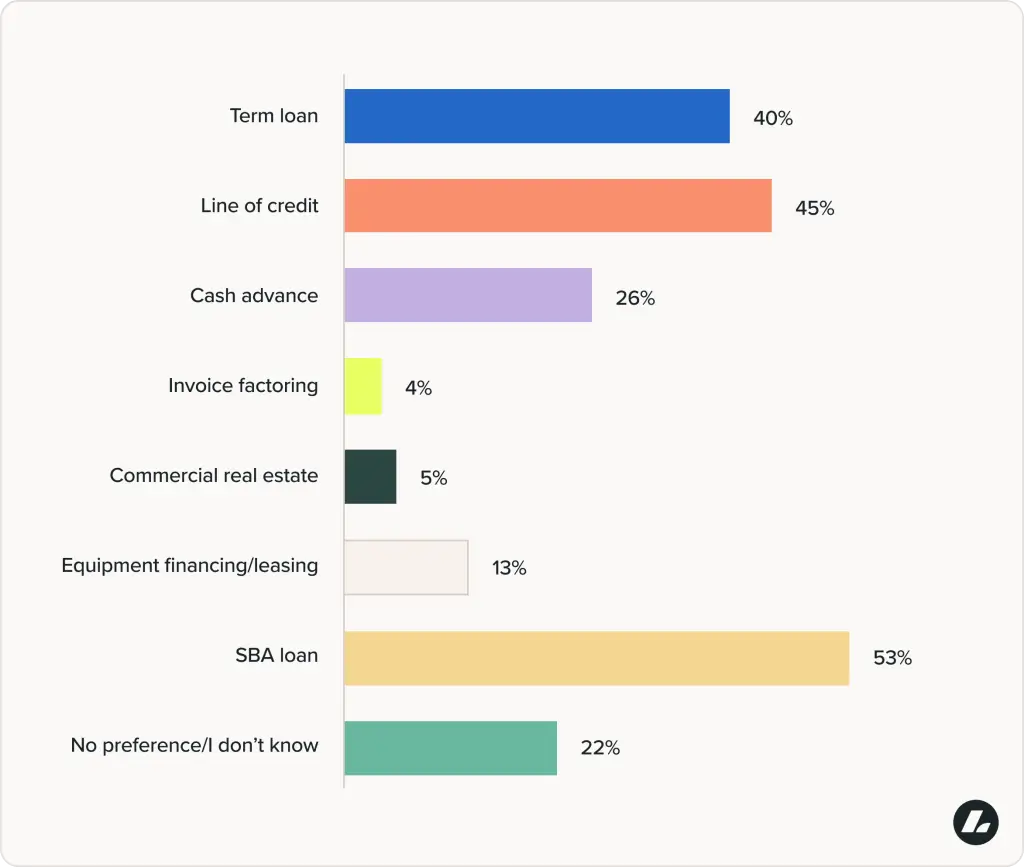

Reasons for a business loan.

Lendio found that the majority of small businesses pursue loans for a variety of essential reasons, primarily to secure working capital (33%) to support daily operations and manage cash flow. Additionally, small businesses often seek financing for crucial investments like equipment purchases (19%), expansion efforts (15%), starting a business (14%), payroll (6%), real estate (4%), or for other purposes (9%). Each of these reasons highlights the integral role that loans play in facilitating growth and sustainability in the competitive business landscape.

Gender insights

Men and women generally had similar responses to Lendio's survey questions, but a few differences stood out.

Only 46% of women are positive or very positive that they can access the capital they need compared to 55.8% of men who said the same. 13% of women also rated their ability to access the capital they need as "very poor" compared to 9% of men.

Another key insight points to a need for education surrounding the business lending landscape, especially for women. 53.3% of women and 41.7% of men are unsure of their primary bank's loan options. More women business owners stated that they would like education on the business loan application process across the board except interest rates (this was equal). This includes lender types, loan agreements, and loan types.

Women-owned businesses received just 32.6% of approvals and 28.4% of the dollars offered in SBA 7(a) and 504 loans in the 2024 fiscal year. Across the lending landscape as a whole, women are less likely to receive the full amount of funds requested. In 2023, 45% of women-owned businesses were approved for the full amount of capital requested vs. 55% of men-owned businesses.

Additionally, 25% of women are denied a business loan compared to 19% of men.

Minority insights

When it comes to accessing business loans and receiving funding, entrepreneurs of color can face significant challenges.

- 84% of businesses started by a person of color relied on personal savings or funding from friends or family to fund their businesses.

- 28% of employer businesses started by a person of color have obtained a business loan compared to 48% of white-owned business startups.

- Nearly half of black business owners who apply for a loan are denied.

Conclusion

Understanding the lending landscape for small businesses is crucial for their growth and success. The statistics presented highlight the significant role that access to financing plays in empowering entrepreneurs across the United States. While optimism prevails among small business owners regarding their ability to secure capital, challenges persist, particularly for women, minority, and veteran entrepreneurs.

Even though the acronym UCC sounds like a college of some sort, it stands for the Uniform Commercial Code (UCC). And rather than hand out diplomas, the UCC was developed to regulate how commercial transactions operate.

OK—But what's a UCC filing?

UCC filings are how lenders establish their right to the assets you, the borrower, use to secure a loan. The filing serves as a lien, so that there's public record of your efforts to take out a loan.

UCC filings are made up of UCC-1 and UCC-3 filings, explained in more detail below.

What is a UCC-1 filing?

A UCC-1 is the official original UCC filing that gets made by a lender, referring to the UCC1 form that's needed in order to do so. It's effectively a public announcement lenders make that either a borrower has taken out a loan with them or is looking to take out a loan with them.

This filing defines the collateral the borrower puts up to secure financing, which prevents a borrower from using the same collateral for multiple loans (a move that would put the lenders at much higher risk).

You could think of it as the financial version of “going public” on social media with a new relationship. Once you change that relationship status, other people who might be interested can see you’re already committed to someone else. They allow lenders to see how you’ve treated other loans in the past.

What is a UCC-3 filing?

A UCC-3 filing is simply an amendment to the original UCC-1 filing.

This might be used to update the information of the borrower or lender, add or change collateral, terminate a filing, or reassign or terminate creditor interest.

What is the difference between a lien and a UCC filing?

Put simply, a UCC filing serves as a lien, whereas a lien may not always be a UCC filing.

Liens can span everything from personal property, to real estate, to tax liens, child support, and much more. UCC liens fall within this list as another subcategory.

Oftentimes, liens arise from legal issues, and can be created involuntarily—for instance, with a property lien. UCC liens are intentionally created by creditors to establish a security interest.

When does UCC filing happen?

This step depends on the lender and the loan product.

Some UCC filings happen after you’ve secured funding. Others are actually filed when you apply for funding so lenders can protect themselves from borrowers trying to get multiple loans at the same time without the lenders knowing about it.

SBA UCC filings

As a security measure, the SBA will file a UCC lien on EIDL loans of more than $25,000. In this case, the SBA establishes the right to any assets you use to secure your EIDL loan, in the case that the loan goes unpaid.

Is a UCC filing bad?

No. UCC filings aren’t bad, nor are they good. They are used as a safety blanket for lenders to secure loans they provide to borrowers. If you take out a loan that goes unpaid, the fact that there is a filing can become a bad thing, but the UCC filing itself does not impact your credit or ability to obtain future loans.

How do you know if you have a UCC filing?

To find if you have a UCC filing, or simply search UCC liens in general, you can use a public record lien search tool, which are usually available on a State-level.

Most states provide public databases of UCC filings. Click below to learn more about accessing UCC filings in your state:

(Note: In some cases, a subscription might be required for access.)

- Alabama UCC Search

- Alaska UCC Search

- Arizona UCC Search

- Arkansas UCC Search

- California UCC Search

- Colorado UCC Search

- Connecticut UCC Search

- Delaware UCC Search

- Florida UCC Search

- Georgia UCC Search

- Hawaii UCC Search

- Idaho UCC Search

- Illinois UCC Search

- Indiana UCC Search

- Iowa UCC Search

- Kansas UCC Search

- Kentucky UCC Search

- Louisiana UCC Search

- Maine UCC Search

- Maryland UCC Search

- Massachusetts UCC Search

- Michigan UCC Search

- Minnesota UCC Search

- Mississippi UCC Search

- Missouri UCC Search

- Montana UCC Search

- Nebraska UCC Search

- Nevada UCC Search

- New Hampshire UCC Search

- New Jersey UCC Search

- New Mexico UCC Search

- New York UCC Search

- North Carolina UCC Search

- North Dakota UCC Search

- Ohio UCC Search

- Oklahoma (individual counties keep UCC records)

- Oregon UCC Search

- Pennsylvania UCC Search

- Rhode Island UCC Search

- South Carolina UCC Search

- South Dakota UCC Search

- Tennessee UCC Search

- Texas UCC Search

- Utah UCC Search

- Vermont UCC Search

- Virginia UCC Search

- Washington UCC Search

- Washington, DC UCC Search

- West Virginia UCC Search

- Wisconsin UCC Search

- Wyoming UCC Search

How can you remove a UCC filing?

A UCC termination filing requires an amendment be made to the original UCC-1 filing, completed using the UCC-3 form.

Thing is, a UCC-3 form can only be submitted by the lender. To get a UCC lien removed, you must ask your lender to file a UCC-3 form, which then comes at their discretion.

In most cases, liens are not removed until you’ve fully repaid a loan.

In the end, UCC filings typically serve purely as an informational guideline—a “just in case” stipulation. It helps to be aware of any UCC filings you might have, but in general, if you’re paying your debts, UCC liens should not bring you any harm.

While some debt is considered good debt for small business owners—debt that ultimately helps the borrower net more in savings or income—other debt is deemed “bad debt.”

The latter includes debt that can directly and negatively impact a business owner’s credit score, or that costs money or potentially limits their ability to secure financing in the future. Past-due debt, sometimes referred to as “delinquent debt,” falls into this category.

What is past due debt?

Past-due debt is the money owed on a missed debt payment.

For example, let’s say you receive a credit card bill of $1,000 with a minimum monthly payment of $50. If you don’t make that $50 payment on time (usually within a month), it will become past due.

This debt payment will often accrue late fees and additional interest if not paid—and continue to accrue fees for as long as it remains unpaid.

You don’t necessarily need to pay the full $1,000 at once—but you missed the required minimum payment, which caused a debt payment to become past due.

Past-due debt can arise from anything that requires regular payments—utilities, rent, credit cards, business loans, and invoices. Any required payment that goes unpaid becomes past due.

What is the difference between past due debt and delinquent debt?

The difference between past due debt and delinquent debt is simply semantics. Debt that is past-due is also considered delinquent.

However, while any unpaid payment is past due, there are differing levels of delinquency. Each level has its own penalties and risks to your financial reputation. Here are a few examples:

- Within 10 days: Many lenders have a grace period of a couple of weeks during which you can pay off the debt. During this time, there aren’t late fees or penalties as long as you pay off your debt. (This grace window varies by the lender—some will charge a fee if you miss the payment date by even a day.)

- After 10 days: You may receive a late fee for your delayed payment, but the lender won’t take any action against your account.

- After 30 days: If you skip a full billing cycle, your creditors will likely report this missed payment to the national credit bureaus. This report can impact your credit score and add delinquency to your credit history.

- After 90 days: If you continue to miss payments, you’ll likely accrue more penalty fees and interest. Your interest rates may increase, and your credit will keep dropping. Eventually, your creditor will send your account to collections and freeze any services you receive.

The impact of past due debt on your business

If you’re contending with multiple sources of debt, start with your past-due accounts. Late payments and delinquent debt can linger on your credit report and negatively impact your credit score.

With a poor credit score, loans (of any kind) will become harder to get—you’ll have to battle less favorable terms and higher interest rates, assuming you can get a loan at all. Paying off your overdue debts first could prevent your account from going into collections and affecting your credit score.

If possible, make the minimum payments on all of your accounts—even if you can’t pay off the full balance. Hitting these minimum payments proves to creditors that you’re still willing to pay what you owe and aren’t going to fall into delinquency.

If you are ever in a situation where you’re unable to make the minimum payment, contact your creditor ASAP. Some credit card companies offer hardship programs where you can pause payments for a few months. Your other lenders may be willing to accept partial payments in the short run.

How long do late payments stay on your credit report?

Payment history is one of the biggest factors of your credit score. Your history lets lenders know how likely you are to miss a payment or become delinquent on the account.

Because of its high value, a missed payment will stay on your credit report for 7 years, whether the missed payment is 30- or 90-days late.

However, a missed payment might not affect your credit score for the full 7 years. If you only miss a few payments, then your credit score might rebound in a couple of years. Multiple factors contribute to your credit score, and maintaining a good payment history is one of the best ways to keep it strong.

How to solve your past due debt

If you have an upcoming loan payment that you can’t afford, don’t panic. Below, we’ll show you a few tactics to keep your lenders satisfied and your cash flow flowing when paying off your debts isn't a readily available option.

Find short-term financing

It’s always scary to fight debt with debt, but sometimes it’s necessary. If you’re struggling to make your loan payments, consider one of these short-term financing options:

- Business Lines of Credit: Use a line of credit to cover practically any business expense: payroll, rent, debt payments, supplies—you name it! You can get funds in as little as 1 to 2 weeks, and then you’ll get immediate access to any funds you use as soon as you repay the amount used.

- Business Credit Cards: If you don't qualify for a line of credit, a business credit card is another great short-term financing option. You can make your necessary loan payments on your credit card and earn cashback and travel rewards while you're at it. Plus, you can score a card with a 0% interest period (sometimes as long as 18 months), meaning you can make lower monthly payments with fewer consequences.

Negotiate with your lenders

Your lenders don’t want you to default.

If you’re struggling to make payments, they may be willing to temporarily restructure your loan. This act could mean lower interest rates, payment deferments, and extended terms.

For example, Bank of America allows businesses to request deferments on loan payments without negative credit reporting.

Funding Circle provides forbearance, repayment flexibility, and even late fee forgiveness.

Talk to your lender and see what help they’re willing to provide. It doesn’t hurt to ask, and you might be surprised with their leniency.

Set reminders for your minimum payments

While your lenders will likely remind you about upcoming bills, you can also set payment reminders to ensure that you at least make your minimum payments.

These reminders will help you avoid past-due debt, even if you still need time to pay off your full balance. Making these small payments will help to protect your credit and your future financial opportunities.

If you’re too busy to remember to make payments, you can also set up autopay options to draft from your account. Just make sure you have enough money to avoid overdraft fees.

Boost your cash flow

Improving your cash flow is probably one of the harder options, but it’s still possible. To boost your cash flow, you’ll need to increase sales or decrease expenses (or both).

Consider areas where you can cut spending. Every dollar counts. And then look for where you can grow your sales. With the digital world as your oyster, there are endless possibilities for making revenue online.

Don't give up

If you can’t make your loan payments, don’t give up. There’s a way out—you’ll make it through this. Hold your head up high and fight for your business’s survival.

A variety of reasons support buying a commercial property for your business. One is that it can give you the flexibility to adapt the building to your needs or expand your operations. Another compelling argument in favor of purchasing a commercial property is that doing so can help you build equity, which is an obvious disadvantage to renting.

Considering whether to buy or rent a commercial space can be difficult, and it is worth noting that those who rent will always, in a sense (and cents), be at the mercy of their landlord. If you have an opportunity to buy commercial real estate with a fixed-rate loan, however, you can make your expenses easier to manage and avoid the risk of either having to pay more in rent or move your business elsewhere.

Purchasing a commercial property for your business could also offer you an array of potential tax benefits and deductions. This includes depreciation and the chance to deduct the interest portion of the mortgage payment. In addition, when you locate your business in the commercial real estate investment, you could potentially deduct the maintenance expenses from the business income. Also, there is a chance you could pay rent to yourself as the property owner, and the rent would be a deduction.

What is commercial real estate?

Commercial real estate refers to properties that are used for business purposes. This type of real estate includes spaces where businesses operate, whether they're retail stores, offices, warehouses, or other types of buildings that generate profit.

Types of commercial real estate.

- Multifamily - As the name implies, this refers to residential investment properties housing multiple families, such as apartment complexes, duplexes, triplexes, and even assisted living communities.

- Office - This refers to large, small, or medium-sized buildings capable of supporting a variety of businesses with a need for space, such as medical providers, attorneys, or accountants.

- Retail - This type of commercial real estate refers to a space that a consumer-facing business may be interested in, such as a coffee house, department store, or a suite in a strip mall.

- Industrial - This term refers to warehouses, production facilities, and distribution centers—basically any type of building a manufacturer may need.

- Hospitality - This area generally covers buildings that are either the current or former home of businesses in the service industry, such as restaurants, hotels, bars, or resorts.

- Special Purpose: Properties specifically designed for a particular business, like hotels, schools, or self-storage facilities.

Within the confines of commercial office real estate, there are three different types.

- Class A refers to commercial real estate of the highest possible quality. These are usually newer buildings in a prime location and in good condition.

- Class B refers to middle-range commercial properties that may be older and lower in price compared to Class A, making them a good target for renovation or restoration.

- Class C commercial real estate refers to older properties in a less-than-optimal location with extensive wear and tear.

How to buy commercial real estate for your business.

Consider the following elements when beginning the purchase process.

1. Identify property requirements.

Understanding your personal goals as a commercial real estate investor is essential, as your goals will influence the property requirements. Are you looking to build a brand or a retail establishment? How much foot traffic are you hoping to attract?

When looking into commercial real estate, consider the following:

- Budget: Know what you can afford before you start looking.

- Zoning Laws: Ensure the property is zoned for your type of business.

- Accessibility: Make sure the location is easily accessible for your customers and employees.

- Future Growth: Think about your future needs and whether the property can accommodate them.

2. Secure financing.

There are a variety of commercial real estate loans available with different terms and commercial mortgage rates. Bear in mind that, unlike a personal mortgage that may be able to cover up to 100% of the cost of the property, a commercial mortgage will typically cover only up to 75% to 80% of the cost of the property.

Commercial mortgage

This refers to any sort of financing where the loan is secured by the value of the underlying commercial asset, which could include a warehouse, apartment complex, office building, shopping center, etc.

SBA 504 loan

The SBA 504 loan is a loan program administered by the Small Business Administration (SBA), in which small business owners partner with Certified Development Companies (CDCs) to secure financing. Usually, a 504 loan will include a first mortgage for around 50% of the cost, from a third-party lender. The SBA will back a second mortgage, up to 40%. This would only leave the remaining 10% to the small business owner, allowing that individual to free up capital. The loan can be used to expand, buy real estate, or purchase equipment.

Hard money loan

This type of financing originates from private individuals or businesses, instead of traditional financial institutions. Generally, a hard money loan refers to a nonconforming loan that can be used to purchase a commercial or investment property, often with a much shorter duration and a higher interest rate compared to other options. A physical asset or property is usually required to serve as collateral for this type of loan.

3. Enlist an experienced team.

Buying commercial real estate can be a complex process, so it's essential to have a team of experienced professionals to guide you. Here are the key people you should consider involving:

- Real Estate Agent/Broker: Specializes in commercial properties and helps you find suitable options. They can negotiate on your behalf and provide market insights.

- Attorney: A lawyer with expertise in commercial real estate can help you with contracts, zoning issues, and legal due diligence.

- Commercial Lender/Mortgage Broker: They can assist in exploring financing options and securing a commercial real estate loan that fits your needs.

- Accountant: Provides financial advice, helps with tax considerations, and aids in determining the property's financial viability.

- Property Inspector: Conducts a thorough inspection of the property to identify any structural or maintenance issues that need to be addressed.

- Appraiser: Offers an independent assessment of the property's value to ensure you're making a sound investment.

- Contractor: If the property requires renovations or modifications, a reputable contractor can estimate costs and manage the construction process.

4. Evaluate the value of the property.

Determining the value of a commercial property is a critical step in the purchasing process. Here's how you can approach it:

- Comparable sales (Comps): Look at recent sales of similar properties in the same area. These comps provide a benchmark for the current market value.

- Income approach: Evaluate the potential rental income the property could generate. This method involves calculating the net operating income (NOI) and dividing it by the capitalization rate to estimate value.

- Cost approach: Consider the cost of replacing the building with a similar one, including the value of the land and the depreciation of the current property.

- Professional appraisal: Hire a certified appraiser who specializes in commercial real estate. An appraisal will give you a detailed report on the property's value based on various factors, including location, condition, and market trends.

- Future potential: Assess the property's potential for appreciation. Investigate local economic growth, infrastructure projects, and zoning changes that might affect the property's value over time.

- Physical condition: Conduct a thorough inspection to identify maintenance or structural issues. Properties in better condition typically command higher prices.

- Market conditions: Stay informed about the current real estate market trends and cycles. The value of commercial properties can fluctuate based on supply and demand dynamics.

5. Make an offer.

Once you've researched the property you'd like to purchase, you can begin the offer process.

- Determine your offer price: Based on your evaluation of the property's value and your budget, decide on an initial offer price. Keep in mind that this price should be competitive but also leave room for negotiation.

- Prepare a letter of intent (LOI): Draft a Letter of Intent outlining your proposed terms and conditions. The LOI should include the offer price, payment terms, due diligence period, and any contingencies such as financing or inspection results.

- Submit the LOI: Present the Letter of Intent to the seller through your real estate agent or broker. This document serves as a formal expression of your interest and opens the door for negotiations.

- Negotiate terms: Be prepared to negotiate with the seller. This may involve several rounds of counteroffers until both parties agree on the final terms. Your real estate agent or broker can be invaluable in guiding you through this process.

- Draft the purchase agreement: Once both parties agree to the terms, have your attorney draft a formal purchase agreement. This legal document will outline all the specific details of the transaction, including contingencies, closing date, and any special conditions.

- Due diligence period: After the offer is accepted, you'll enter the due diligence period. During this time, conduct thorough inspections, review financial records, verify zoning laws, and ensure there are no hidden issues with the property. This period allows you to confirm that the property meets your expectations before finalizing the purchase.

- Secure financing: Work with your commercial lender or mortgage broker to finalize your financing arrangements. Ensure all necessary documents and approvals are in place to secure the loan.

- Close the deal: If everything checks out during the due diligence period and your financing is secured, proceed to the closing. This stage involves signing all required documents, transferring funds, and obtaining the keys to the property.

Ready to start looking into financing for a commercial property? Learn more about commercial mortgages.

As a small business owner, you’re probably familiar with at least a few of the many loan products available. Many lenders require you to offer an asset to secure a debt. As time goes by, you might find yourself securing multiple loans with the same asset—a process called cross-collateralization.

Cross-collateralization is fairly common—“second mortgages” are a popular form of cross-collateralization, for example. There can be many benefits to taking advantage of cross-collateralization, but this process also increases the risk of losing assets, so it’s important to understand how cross-collateralization works before making any formal arrangement.

What to know about collateral.

There are two main types of loans: secured loans and unsecured loans. These loans differ in regard to collateral requirements. Collateral is an asset that a borrower offers up as a way to guarantee the amount of a loan. Common forms of collateral include cash deposits, real estate, or vehicles.

Secured loans require collateral, while unsecured loans do not. If you default on secured loans, the lender can seize the collateral as repayment for the loan amount. Lenders of unsecured loans, like credit cards, have no such recourse, but this usually causes the repayment terms of unsecured loans to be less favorable for the borrower.

In many cases, a lender uses an asset to secure the loan for that very asset. This is common with home mortgages, car loans, and equipment financing. If you have a mortgage, your house is the collateral—so if you default on your mortgage, the lender can then collect the collateral and repossess your house.

What is cross-collateralization?

Cross collateralization refers to a situation where multiple loans are secured with the same asset.

In a second mortgage situation, your home serves as collateral for a mortgage. As you pay down your mortgage, you own more of your home. You can then use your home as collateral for a second loan, i.e., a second mortgage.

Cross collateralization also occurs if different types of financing are secured with the same asset. If you’re paying off a car loan, the car becomes collateral for this loan. If you use the car as collateral for another type of financing, like a credit card, this is cross-collateralization.

“Cross-collateral refers to a method that lenders use to utilize the collateral of a loan such as a car to secure a second loan that an individual may have with the lender,” explains Jason Gordon at The Business Professor. “When an asset is cross-collateralized, it brings up issues as to which secured party has priority to the asset in the event of default.”

Less commonly, cross-collateralization also refers to a situation when a lender requires multiple forms of collateral for a single loan.

How cross-collateralization works.

Understanding the workings of cross-collateralization is crucial for any business owner considering this route. Essentially, this process ties the value and security of one or more loans to the same collateral. This is advantageous in situations where you may not have enough separate assets to secure multiple loans. For example, if you have equity in your property, you can leverage it to secure not just a primary mortgage but also a business loan or line of credit.

When you enter into a cross-collateralization agreement, it's like you're giving the lender a broader safety net. In the event of a default on any of the loans secured by the same asset, the lender has the right to seize and sell that asset to cover your debt. This means the stakes are higher for you because failing to repay one loan could jeopardize the asset tied to all the loans.

One critical aspect to monitor with cross-collateralized loans is the loan-to-value (LTV) ratio. This ratio measures the loan amount against the value of the collateral securing it. A higher LTV ratio indicates more borrowing against the asset, which can be risky if the market value of the collateral decreases.

For businesses, cross-collateralization can open doors to additional funding that might not be available otherwise. However, it compounds the risk to your assets. Therefore, it's wise to carefully assess your financial stability and the implications of tying multiple debts to vital assets before proceeding with such arrangements.

Benefits and risks of cross-collateralization.

Cross-collateralization can be a double-edged sword for savvy business owners, meshing intriguing benefits with profound risks. It's like stepping into a strategic game where your assets are on the line, offering a chance to secure more funding while posing a significant risk if the tides turn. In this section, we'll unravel the perks and perils of cross-collateralization, aiming to provide a balanced view that helps you weigh its worthiness against your business strategy.

Benefits

- Increased loan access: Cross-collateralization can significantly enhance your borrowing power. By leveraging the same asset for multiple loans, businesses can access higher loan amounts or more favorable terms than might be available with unsecured financing.

- Flexibility in financing: This strategy offers flexibility, allowing businesses to tap into the equity of their assets, such as real estate or vehicles, for various financial needs, from expanding operations to covering unexpected expenses.

- Potential for better rates: Often, loans that are secured by collateral have lower interest rates compared to unsecured loans. Cross-collateralization might help negotiate lower rates due to the added security it provides lenders.

Risks

- Increased loss risk: The primary risk of cross-collateralization is the potential loss of valuable assets. If a business cannot meet its loan obligations, the asset securing multiple loans could be seized, having a more significant impact than defaulting on a single secured loan.

- Complexity in managing loans: Juggling multiple loans tied to the same collateral can lead to intricate financial management challenges. Keeping track of various terms, interest rates, and repayment schedules requires diligent oversight.

- Difficulty in switching lenders: Once an asset is cross-collateralized, it may be more challenging to refinance or obtain new loans with different lenders. The existing cross-collateral agreements might limit flexibility and negotiation power with potential lenders.

What is a cross-collateral loan?

A cross-collateral loan essentially links the collateral of multiple loans together. This means if you've borrowed money to purchase a car and later decide to take out a personal loan, the same car can act as the collateral for both loans if both are through the same lender. This strategy can be particularly appealing for borrowers looking to maximize their borrowing capacity without having to find new assets to secure each loan.

However, it's essential to understand that cross-collateralizing your loans binds them together in a way that can complicate future financial moves. For instance, if you wanted to sell the car that's serving as collateral for your loans, you'd need to pay off or substantially pay down the debts to remove the lender's claim on your asset. This intertwining of debts and assets makes managing your finances a bit more complex but can be a powerful tool in the right circumstances.

Is cross-collateralization legal?

Cross-collateralization is legal and fairly common, but a lender is required to inform you that cross-collateralization is occurring.

If you take out multiple secured loans from the same lender, like a bank, it might use the same collateral, making your assets cross-collateralized. You must legally consent to this, but do your due diligence in reading over any loan agreement. Be especially aware of “dragnet clauses” where a lender can pursue your asset if you used it for collateral for any loan with the lender.“

Lenders cannot use your business’s property as collateral without your consent,” writes Shawn Grimsley in the Houston Chronicle. “Lenders obtain your consent to cross-collateralization through a dragnet clause, which may allow the lender to use the collateral for any loans or other obligations your business may owe the lender.”

Is cross-collateralization bad?

If you can make your loan repayments on time, you’ll probably have no issues with cross-collateralization. Trouble arises if you default, however. If an asset is cross-collateralized and you default on one of your loans, you will default on all of your loans, because the asset can no longer secure any of them.

Can banks cross-collateralize?

Banks cross-collateralize often, but cross-collateralization is even more common with credit unions. Cross-collateralization is especially conventional when you seek multiple loans from a single lender. With every loan you take out, read over the agreement and make sure you consent to how a loan is secured.

How do I get out of cross-collateralization?

The best way to untangle yourself from a bad cross-collateralization situation is to contact the lender and attempt to renegotiate your loan. You might, for example, be able to secure the remaining debt with other collateral, although the repayment terms might be worse.

Bad cross-collateralization situations usually end with the loss of the asset, even if you declare bankruptcy. Unfortunately, besides repayment, the only way to get out of cross-collateralization is by letting your lenders repossess the collateral.

Alternatives to a cross-collateral loan.

Exploring alternatives to a cross-collateral loan is important for any business owner seeking flexibility and minimal risk in financing options. One such alternative is seeking out unsecured loans. Although typically bearing higher interest rates due to the increased risk for the lender, unsecured loans do not tie down your assets, providing peace of mind and simpler asset management.

Another option could be asset-based lending, which focuses on the value of specific assets rather than intertwining them across loans. This method allows for targeted borrowing against inventory, receivables, or other business assets without cross-collateralization complications.

Crowdfunding or peer-to-peer lending platforms also present innovative financing avenues. These methods can offer more favorable terms and the opportunity to avoid traditional banking systems and their associated risks and constraints. Each alternative has its unique set of benefits and considerations, gearing towards providing a tailored solution that aligns with your business's financial strategy and growth objectives.

Navigating the complexities of cross-collateralization requires a delicate balance between leveraging your assets for financial gain and protecting them from undue risk. Whether you're a seasoned business owner or new to the entrepreneurial scene, understanding the intricacies of secured loans, including cross-collateral loans, is crucial.

By weighing the benefits against the potential drawbacks and considering viable alternatives, you can make informed decisions that align with your financial goals and risk tolerance. Remember, the key to successful financial management lies not only in securing the necessary funds but also in maintaining control over your assets and their future.

You may have decided to buy an existing business after it popped up on your radar. But more likely, you’ll have to look for a business that is for sale.

You can find businesses for sale via:

- Business brokers

- Networks and small business associations

- Your current employer

- Directory listings

- Advertisements

1. Hire a business broker.

A business broker is similar to a real estate agent. They know the ins and outs of which businesses are for sale (including which are a steal versus a money pit) and understand the nuances of specific industries. The broker will also help you throughout the negotiation process.

You may have to use a business broker with certain sellers who use intermediaries to protect their identity. Business owners sometimes keep their “for sale” activity secret to avoid provoking anxiety in suppliers, customers, and employees.

What to look for in a business broker.

Choosing the right business broker is crucial for a smooth transaction. Consider these key attributes:

- Experience and Industry Expertise: A broker with a solid track record in your business sector will better understand market conditions and potential pitfalls.

- Certifications and Professional Affiliations: Look for membership in the International Business Brokers Association (IBBA) or similar organizations to ensure professionalism.

- Reputation and Client Testimonials: Research reviews and ask for references to gauge client satisfaction and success stories.

- Network and Reach: A well-connected broker with extensive industry contacts can offer more opportunities and access to potential buyers or sellers.

- Fees and Contract Terms: Discuss upfront to ensure there are no hidden charges and both parties are clear on expectations and deliverables.

You’ll pay a fee to use a business broker, but it can be worth it to avoid surprises during the purchase process.

How to find a small business broker.

Places to find a small business broker include:

- Business broker associations

- Your professional network

- Ask other for-sale businesses

Business Broker Associations

Business brokers are like the rest of us. They often belong to professional organizations to stay current with industry trends, boost their visibility, and increase networking opportunities. Most business broker associations list their members on their websites.

Two well-known business brokers’ associations to review are:

Your network

Your professional network, including your attorney, accountant, or business peers, may be able to recommend a business broker. Don’t forget to check with your local SCORE chapter or small business development centers.

Ask for recommendations from for-sale businesses.

Do you know a business for sale that you aren’t targeting for purchase? Ask them if they are using a business broker that they’d recommend.

2. Ask your network.

This is the perfect time to tap into your professional network and small business associations. Often, they know what companies are on the market or are open to a conversation about selling.

Using your network to find businesses for sale offers several significant advantages. Firstly, there’s an inherent level of trust and credibility because you're often dealing with established relationships. This trust can streamline negotiations and provide access to information that might not be publicly available.

Secondly, your network can offer deeper insights and firsthand experiences about potential businesses, helping you make a more informed decision.

Additionally, leveraging your network can lead to more discreet inquiries, which is crucial in preserving confidentiality during your search. Finally, using your network can save both time and resources by tapping into a pool of pre-vetted opportunities, compared to cold-search methods.

3. Check with your employer.

Depending on your employment situation, perhaps you could buy your current employer’s business. You don’t want to appear to be staging a takeover, so start the conversation by asking what their succession plan is. That could lead to deeper discussion, including your interest in purchasing the business.

4. Explore directory listings.

Internet searches and directory listings such as BizBuySell.com, Bizquest.com, and LoopNet.com are also great sources for finding businesses for sale.

These sites allow you to filter your search by location, industry, and business size. They also provide detailed information on the business’s financials, such as revenue and cash flow. However, keep in mind that many of these directories charge a fee for listing businesses for sale, so not all companies may be represented.

5. Look for advertisements.

Finally, don’t overlook traditional methods like newspaper or online ads. Local publications often feature businesses for sale in their classifieds section.

A business owner planning a DIY sale may accept a lower purchase price since business broker fees will be eliminated. Finding the best small business to buy takes time but will pay off in dividends down the road. When you are ready to take the leap, remember that Lendio can walk you through the steps to secure a business acquisition loan.

The availability of dependable cash flow can have a big impact on the success of a small business. Yet a 2021 report from the Federal Reserve shows that, when businesses applied for financing, nearly 60% of applicants were either outright denied or able to borrow only a portion of the money they needed.

It’s tempting to look at the bank as the bad guy in this scenario. Yet it’s important to understand that smaller commercial loans aren’t always a good fit for large traditional lenders. From a processing and profit standpoint, issuing smaller commercial loans might not be practical for some lending institutions.

So, what options do small business owners have in this situation? For many small business owners who are stunned to learn how hard it is to get a business loan, the answer is to consider alternative business loans.

What are alternative business loans?

Alternative business loans are business loans, lines of credit or other forms of business financing offered by lenders other than through traditional banks. They are also often called online loans because they are accessible through online applications and platforms.

Alternative business loans vs. traditional business loans.

Traditional business loans are generally associated with banks and credit unions, where the application process can be lengthy and requires extensive documentation, such as financial records and business plans. Interest rates might be lower, but qualifying for these loans is often a challenge for small businesses without a strong credit history or significant collateral.

On the flip side, alternative business loans, accessible through online lenders, provide a more streamlined application process, often with less stringent requirements for credit scores and documentation. They can be a boon for businesses needing quick cash flow solutions, as approval times are significantly shorter, sometimes even within the same day. However, this convenience can come at a cost, with potentially higher interest rates and fees than traditional loans.

What are my alternative financing options?

Here are some examples of alternative financing options available to small businesses.

Business term loans.

Business term loans are what many people think of when they think of business financing. Term loans often feature fixed interest rates, fixed monthly payments, and a fixed number of monthly payments (aka repayment period). Depending on the lender, you may be able to use the funds you borrow for a variety of purposes, from equipment needs to cash flow support to expansion.

Short term loans.

Short term loans earn their title because they typically feature a shorter repayment period. With this type of alternative business loan, you might have to repay your loan within a year or less, though terms can vary. These loans sometimes come with weekly or even daily payments as well.

This loan option could be helpful if your business needs to access funds in a hurry (provided you’re working with a reputable alternative lender). However, you should make sure the loan offer makes sense for your business and that you can manage an expedited repayment schedule. A business owner might consider this type of loan to address a financial slump, manage a seasonal downturn, finance short-term projects, and more.

Equipment financing

Equipment financing is a type of loan that can help you finance essential tools and equipment for your business to operate. The equipment itself typically serves as collateral for the loan. As a result, you may be able to lock in a better rate for this type of financing, compared to other borrowing options. Depending on the lender, however, you may also need to provide a down payment.

SBA loan

Although you can apply for SBA loans with traditional banks, some online lenders offer them as well. Loans backed by the U.S. Small Business Administration can be a great fit for small businesses, since they often feature affordable rates, high loan amounts, and lengthy repayment terms.

On the other hand, the approval criteria for SBA loans tends to be on the stricter side. For example, with SBA 7(a) loans, you’ll need a minimum FICO® SBSS Score of 155 to qualify. SBA loans also tend to feature slower funding periods with loan processes that often take weeks or even months to complete.

Business credit card.

Business credit cards are a flexible financing option that may be available to established businesses and startups alike. However, you may need good personal credit to qualify. The interest rates on business credit cards (and credit cards in general) are often high. So, it’s best to use this form of financing for short-term cash flow support—never borrowing more than you can afford to pay off in a given billing cycle. When you revolve a balance from one month to the next, interest charges generally apply.

Many business credit cards come with the potential to help you build good business credit for your company as well. And if you open a business rewards credit card, you might earn valuable points, miles, or cash back on purchases that your business already needed to make.

Business line of credit.

A business line of credit is another flexible way to borrow money for your business. When you open a line of credit you receive a credit limit—the maximum amount your business can borrow on the account. As you use the line of credit, your available credit shrinks. But when you repay some (or all) of the money you borrowed, you should be free to borrow again against the same credit line.

Business lines of credit often feature revolving interest rates (like credit cards). These revolving interest rates can range from affordable to high, depending on the lender you choose, your creditworthiness, and other factors. Yet you pay interest only on the money you borrow, not the overall credit line. So, you have a bit more control over the process than you would with a traditional business loan.

Business cash advance.

A business cash advance (also called a merchant cash advance) lets your company borrow against money it will make in the future. In general, the cash advance provider will base the amount your business is eligible to borrow on its credit card sales volume.

As you collect future credit card payments, the cash advance company may take a portion of your daily sales to repay the borrowed funds, plus a “factor rate.” Factor rates can be high, making merchant cash advances a potentially expensive financing option. So, it’s important to review your company’s finances and make sure it can handle the expense and repayment schedule before you move forward.

Accounts receivable financing.

Accounts receivable financing—also called invoice financing—offers small business owners another way to borrow against future earnings. If your business invoices its customers and has to wait to receive payment, you might be eligible for this funding solution.

In general, you don’t need good personal or business credit to qualify for accounts receivable financing. Rather, financing companies will consider the creditworthiness and payment capability of your customers (aka debtors) instead.

Peer-to-peer lending.

Peer-to-peer lending (P2P lending) has emerged as a popular alternative financing option for small business owners. Unlike traditional loans issued by banks or financial institutions, P2P lending allows businesses to obtain capital directly from individual investors. This occurs on online platforms specifically designed to facilitate these types of transactions.

For borrowers, the appeal of P2P lending lies in its potentially lower interest rates, flexible terms, and the ease of application and quick funding times. For investors, it offers an opportunity to earn higher returns on their investment compared to traditional savings or investment products. However, it's important for business owners to understand that while P2P lending can be less stringent in terms of creditworthiness requirements, the rates and terms vary widely based on the platform and the borrower's credit profile.

Who are alternative lenders?

Since 2012, more than 100 participants have entered the alternative lending industry. These companies offer a variety of alternative financing options, from term loans to cash advances. The flexibility that alternative business loans offer can make these funding solutions an excellent resource for small business owners.

| Lender/funder* | Best loan/financing type | Loan/financing amount | Min. time in business | Min. credit score |

| Idea Financial | Line of credit | $10k to $250k | 2 years | 650 |

| Headway Capital | Line of credit | $5k to $100k | 1 year | 625 |

| Funding Circle | Term loan | Up to $500,000 | 2 years | 660 |

| OnDeck | Term loan | $5,000 to $250,000 | 1 year | 625 |

| BHG Money | Term loan | $20k to $500k | 2 years | 700 |

| Ready Capital | SBA 7(a) | Up to $5 million | 2 years | 640 |

| Balboa | Equipment financing | Up to $500,000 | 1 year | 620 |

| Clicklease | Equipment financing | $500 to $20,000 | Any | 520 |

| Kapitus | Revenue-based financing | Up to $5 million | 2 years | 650 |

| Raistone Capital | Invoice Factoring | $40k to $500 million+ | 1 year | N/A |

| Gillman-Bagley | Invoice Factoring | $50K to $10 million | 3 months | N/A |

| Eagle Business Funding | Invoice Factoring | Up to $5 million | None | None, based on your accounts receivable |

See our full collection of best business loans.

Pros and cons of alternative lending.

Pros

Below are some of the benefits that alternative business loans have to offer.

Online applications

Most alternative lenders have embraced technology and provide applicants with simple loan applications that take just a few minutes to fill out. By comparison, some business loan applications can take hours or more to complete, given their sometimes heavy documentation requirements. With a simplified loan application process, alternative lenders free small business owners up to focus on what really matters—running their businesses.

Less stringent requirements.

Traditional lenders will consider a variety of factors when you apply for a business loan. A business lender may review your personal credit score, business credit score, time in business, annual revenue, collateral, and more to determine whether or not to approve your application for financing and what terms to offer you if you qualify.

Alternative lenders tend to be more lenient where business loan requirements are concerned. You might be able to get an alternative business loan with less-than-perfect credit, lower annual revenue numbers, etc. There are even first-time small business loans from alternative lenders for eligible startups.

Faster funding speed.

Another potential perk of using alternative business loans has to do with funding speed. When you work with a traditional lender, you might have to wait days or even weeks after qualification to receive your business loan proceeds. The SBA loan process, for example, is reported to sometimes take several months to complete.

With alternative financing, on the other hand, some lenders offer same-day or next-day funding. This can give small business owners faster access to the capital they need in a hurry to manage cash flow, cover expenses, order inventory, invest in growth opportunities, and more.

Credit building potential.

The potential to establish credit for your business is a valuable benefit. Many alternative business lenders also offer their customers the opportunity to build business credit, just like traditional lenders. If you want to establish business credit, you should look for an alternative lender that reports to one or more of the business credit reporting agencies.

Of course, how you manage your alternative business loan matters most where your business credit is concerned. If you have an alternative business loan that appears on one or more of your business credit reports, it’s essential to pay on time every month. (Tip: Some business credit scoring models may reward you more if you pay early.) If you make late payments on your business credit obligations, however, those negative notations have the potential to damage your business credit scores.

Flexible usage of funding.

Some alternative business loans offer business owners more flexibility when it comes to how they use the money they borrow. If you need to secure financing that your business may need to cover a variety of different expenses or investments, having less restrictive rules around how you use the funds you borrow can be useful.

More financing options.

When you apply for business financing from a traditional lender, you might not have a lot of different funding choices available. Alternative lenders, by comparison, offer a variety of financing options, such as those outlined below.

Cons

While alternative lending offers a plethora of advantages, it's important to approach them with a balanced perspective by considering the possible downsides.

Higher costs

One significant drawback of alternative lending is the potentially higher cost of borrowing. Interest rates and fees may be considerably higher than those offered by traditional lenders, especially for businesses with less-than-stellar credit histories. This can significantly increase the overall cost of financing, affecting your business's financial health in the long term.

Shorter repayment terms.

Many alternative loans come with shorter repayment terms compared to traditional bank loans. This can result in higher monthly payments, which might strain your business's cash flow. It's crucial to assess whether your business can comfortably manage these payments before proceeding.

Risk of unreliable lenders.

The alternative lending space, though innovative, can also attract lenders who are less than scrupulous. Due diligence is essential to ensure you're dealing with a reputable lender. Look for reviews, testimonials, and any possible red flags before you commit to a loan.

Potential for debt cycle.

Because of their accessibility and speed, there's a risk of becoming reliant on alternative lending for regular cash flow needs. This can lead to a cycle of debt that is difficult to escape, especially if the business uses new loans to pay off existing debts.

May not report to credit bureaus.

Some alternative lenders do not report to credit bureaus, which means these loans won't help build your business's credit profile. If building credit is one of your goals, verify with the lender whether they report to the major credit bureaus before you apply.

Less personalized service.

While not always the case, alternative lenders might offer less personalized service compared to a traditional bank where you might have a dedicated relationship manager. This can make it more challenging to negotiate terms or receive guidance based on your specific business needs.

The bottom line.

Navigating the world of business financing can be complex, but understanding your options with alternative lending is a crucial step towards finding a solution that aligns with your company's needs and goals. Whether you're seeking to manage cash flow, expand operations, or simply get through a rough patch, alternative loans offer a range of solutions that might be suitable. Remember, the key is to consider both the immediate benefits and the long-term implications of any financial decision.

Before making a decision, assess your business's financial health, project future cash flows, and consider how the loan fits into your broader business strategy. It's also prudent to consult with a financial advisor to understand the full impact of taking on new debt. Ultimately, by doing your due diligence and thoroughly weighing the pros and cons, you can choose a financing option that helps your business grow while maintaining its financial health.

Alternative lending can be a vital resource for businesses that might not qualify for traditional bank loans. However, it's essential to approach this option with caution, understanding the terms, the lender's credibility, and how the loan fits into your overall financial strategy. With careful planning and strategic decision-making, alternative lending can provide the financial support your business needs to thrive.