Running a business is difficult, and the COVID-19 pandemic didn’t make it any easier for businesses worldwide. To mitigate damage to businesses as a result of the pandemic, the U.S. Congress, fortunately, passed the Coronavirus Aid, Relief, and Economic Security (CARES) Act. One key component of the CARES Act is the Employee Retention Credit (ERC). While many small business owners have acted to take advantage of the ERC to reduce their taxes owed or receive a much-needed tax refund, however, many are unaware that a portion of the ERC can be non-refundable.

To help you better understand and accurately anticipate how the ERC could benefit your business’ bottom line, let’s discuss how the ERC works and which portions are non-refundable.

The Employee Retention Credit

To incentivize companies to keep employees on the payroll during the coronavirus, the ERC allowed companies to take a 70% tax credit for up to $10,000 of an employee’s qualifying wages in each quarter of the first three quarters of 2021. Companies which started after February 15, 2020 and made less than $1,000,000 in gross receipts could also qualify for $7,000 in the fourth quarter of 2021. Companies could also take up to $5,000 in credit for the 2020 year.

The credit reduces a business’s total owed taxes. It does not lower its taxable income like a deductible.

The ERC was focused on more small businesses with fewer than 500 employees in 2021 or less than 100 employees in 2020. However, any business can qualify if the business meets the required criteria for the ERC. Find out more about the ERC and if you qualify. Companies can only qualify for the credit if they were subject to a lockdown or a significant loss of revenue.

In 2021, the ERC was also amended to help startup businesses, too. “Recovery Startup Businesses” are companies that were started after February 15, 2020, and had less than $1 million in revenue. Recovery startup businesses can apply for the ERC for Q3 and Q4 of 2021 and receive up to $50,000 in ERC per quarter.

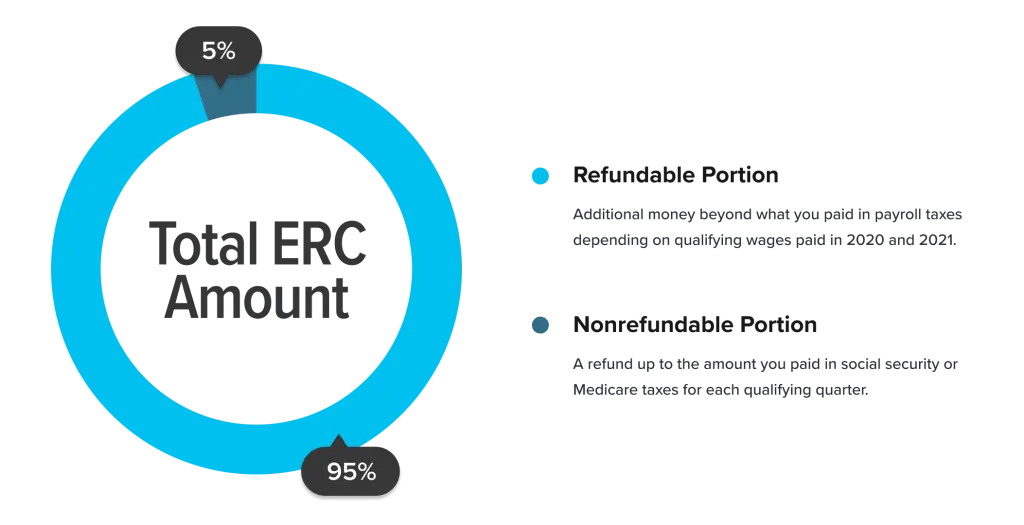

What is the Non-Refundable Portion of the ERC?

It really comes down to some confusing definitions.

Most people think of a refund as money they’re getting back that they already paid. But in the case of the refundable portion of the ERC, if you qualify for the tax credit, you will most likely be getting more money back than you initially paid in payroll taxes.

That’s because the refundable portion of the ERC is meant to offset your total payroll expenses and is calculated on qualifying wages minus any remaining social security or medicare tax liability, depending on the quarter.

In IRS speak, the term “non-refundable” means that the amount cannot be used to increase a business’s refund or create a refund that wasn’t there prior. Most tax credits are nonrefundable.

With the nonrefundable portion of the ERC, you are credited up to, but not more than, the amount you paid in social security or medicare taxes for each qualifying quarter.

When your ERC is being calculated, your total tax credit will be a combination of these two portions.

How to Claim the ERC on Form 941-X

If you qualify for the ERC, but did not use the credit in previous filings and overpaid your taxes, you will need to amend your quarterly filings with Form 941-X.

Form 941-X requires a bit of information, including when you discovered the error (or in this case, when you discovered you qualified for the ERC), the monetary amount, and why you believe the mistake happened. Since the form can have some complicated pieces, it is best to work with someone with expertise in ERC.

If you’re filing a Form 941-X, you have 3 years from the initial filing to amend your taxes.

Can I Still Qualify for the ERC?

Good news! Businesses can still qualify and apply for the ERC. The Employee Retention Credit officially ended on September 30, 2021, but businesses have 3 years from that date to look back at taxes and apply for the ERC.

Even if your business received other assistance from a Paycheck Protection Program (PPP) loan, you might still qualify for the ERC.

Get Started on Your ERC

The ERC is a great benefit for businesses affected by the pandemic. If your business kept your team employed during the pandemic and you were affected by a lockdown or a drop in revenue, you may be eligible for the ERC. The non-refundable part of the ERC is based on the Social Security Tax of the employees. However, if you amend a previous Form 940, the Social Security Taxes may have already been paid, and the non-refundable portion is already settled.

Filing for or amending an Employer’s Quarterly Federal Tax Return to get the ERC can be a bit daunting for business owners. Working with a team who understands the ERC and how to file correctly will help streamline the process.

Kenny Rogers had it right: it is important to understand how to approach different situations and learn to deal with the cards you are dealt—literally and figuratively—particularly when you're addressing market competitors.

The same sentiment from “The Gambler” applies to small business owners considering their best move forward with competition on Main Street. As a business owner, you need to know when your competition makes moves, how their moves affect your business, and what you need to do in response.

Much like gambling at the poker table, you can increase the odds of beating your business opposition when you understand the strategy behind their moves and your available options.

What Are Common Moves by Small Business Competitors?

Small businesses in any industry or market have several strategic moves available to them, including your own.

Whether it’s a market competitor opening another location close to yours, a business deciding to slash their prices for the summer, or the launch of a new product in your space, the moves your competitors might make can be broad and with varying significance.

For example, if you run a Mexican restaurant, you may have a cross-town competitor launch a special on Tuesday night’s “Taco Tuesday” that offers a significant discount to patrons. You may also have a Mexican food truck that partners with the brewery across the street from you, where a lot of your walk-ins come from. You know that responding to both these moves is important … but after assessing the competition and situation, you prioritize the food truck across the street because your analysis indicates that it is likely to have a more immediate and bigger impact on your business.

Some of the common competitive moves you may face include:

Market Competition Lowers or Raises Prices: Changing prices is one of the most common competitive moves made by small (and large) businesses. With an estimated 92% of customerscomparing prices before purchasing, it’s also one of the most effective ways to gain a competitive advantage. Whether competitors are decreasing or increasing their prices, you have to determine how your business will respond.

Market Competitor Invests in a Marketing Strategy: Businesses of all sizes will often turn to marketing and advertising when looking for opportunities to gain market share from the competition. If you hear your competitor on the radio or see their ad on a billboard, how would you respond?

Market Competitors Expand Their Business: Your competitors may decide to expand their business through additional locations or by purchasing new equipment or assets to further their production capacity and scale. If you run a junk removal business and one of your competitors purchases an additional truck and trailer to increase their output, how will that impact your business and what should you do about it?

Market Competition Changes Product or Service: Competitors will often add or remove products or services from time to time, creating opportunities or challenges for your own business. How you respond to changes in your competitors’ offerings can have a significant effect on your short- and long-term growth.

How Do Direct Competitors’ Moves Affect Your Business?

Recognizing when your direct competitors make a move is important, but even more so is the ability to know how it will affect your business. If you run a local web design company and your competitor starts contacting your clients, do you know how that will affect your business? Are your clients going to defect to your competition?

While every industry, market, and business is unique, below are a few potential outcomes of different competitive scenarios in businesses.

Direct Competition Lowers Their Prices

Competing businesses can go months or even years without changing their prices, and this period may sometimes feel like a ceasefire during the inevitable pricing war. Then, out of the blue, your competition decides to break this unspoken truce and lower its prices.

Immediately, you may feel pressured to lower your own prices to match—but is that the right move? Before you take any action, you need to understand how your business is impacted by their lower prices.

When competition lowers their prices, it can:

Change customer expectations: There’s a value exchange anytime a customer purchases a product or service, and the price of that purchase is the quantifiable measurement of said value. When a competitor lowers their prices for a similar good or service to yours, it can change the customer's perceived value either positively or negatively depending on the quality of your goods or services. If your quality is similar to or worse than the competitor's, customers may choose your competition because they are receiving more value.

Signal an industry change: Your competition may have lowered their price because they found a way to lower their own costs and want to pass those savings onto the customer. Whether it’s new equipment, improved technology, cheaper materials, better vendors, or operational changes, the move to lower pricing could signal a larger change within the industry or market.

Influence market share: Market leaders don’t usually spearhead price wars, it’s usually businesses with a smaller share of the pie or new companies entering a competitive market. In either case, when a competitor has lower prices, it can influence market share in their favor—if they can sustain those lower prices.

To truly understand the impact of a competitor’s lower prices on your business, consider talking with your customers and gaining some additional insight into their loyalty and perception of the competition’s new prices.

Market Competitor Steals Your Best Employees

You may not realize it, but your employees are some of your most valuable assets, especially your best ones. And, if a competitor swoops in with a better offer, would they jump ship?

Odds are, yes.

We’re currently in the midst of the “Great Resignation,” with US employees quitting jobs at rates unmatched over the last 20 years. Your small business isn’t just competing with other companies for customers, it’s also competing for talent.

If your employees are switching to your competitor, it can have a significant effect on your business. It causes productivity to decrease—the highest-performing employees are believed to be 4x more productive than your average employee. It also costs a lot of time and money to replace them with the average US company spending approximately $4,000 and 52 days finding a new employee. Moreover, employees for small businesses often develop strong relationships with customers, so if they move to a competitor, those customers may follow.

Direct Competitor Introduces a New Product or Service

Many businesses will introduce new products or services to their customers in an effort to diversify their portfolios and add value. If your competitor launches a new product or implements a new or improved service, customers are likely to notice.

For example, even before the pandemic and global lockdown, retailers—including small businesses—were implementing more flexible check-out experiences with services like home delivery or buy-online-pickup-in-store (BOPIS).

One study from the National Retail Federation found that 70% of shoppers said the convenience of BOPIS improved their shopping experience. If you run a retail store and a competitor launches BOPIS for its shoppers, you may see customers opt for the convenience of your competition.

When your competition introduces new products or services, customers may reevaluate their needs. If it’s disruptive or isn’t easily replicated, it can differentiate them from you and other similar businesses in your market—making it challenging to overcome. This could lead to lost customers or worse if it renders your business obsolete (video rental stores, one-hour photo labs, record stores).

How to Respond to a Competitor’s Move

So far, we’ve discussed common competitive moves and how some of those moves affect businesses differently, but the real question is, what do you do? How should you respond when a competitor takes aim at your business?

1. Acknowledge and Assess Their Competitive Strategy

Before you can respond to a competitor’s move, you need to recognize and contextualize it. This requires monitoring your competition on an ongoing basis and staying updated on your market and industry.

Conducting periodic competitive and market analyses is a great way to keep a pulse on what’s going on with your competition and the industry as a whole. You may also want to check your direct competitors more frequently for common changes related to pricing, products, and marketing.

2. Measure and Forecast Its Impact

After you’ve discovered a strategic move by your competition, the next step is measuring its effect on your business. Depending on the move, you may already have noticed a change in your business—more times than not, however, you’ll need to forecast and estimate its impact.

For example, if a competitor has lowered their pricing on a product you also offer from $10 to $9, you should try to predict the impact that change will have on your business before making any response.

If that product costs you $6, a change from $10 to $9 decreases your profit by $1 per sale. If you want to go a step further (and you should), try to predict the total effect it could have on your revenue by estimating how many customers you expect to lose (and keep) if you don’t lower your price.

Let’s say over the course of a year, you average 2,000 sales of that product. If you lower your price, you’ll retain them all—if you don’t, you anticipate losing 500 sales. At first, losing 25% of your sales may seem like a red flag, but let’s look at the numbers.

Lower Price to $9

Keep Price at $10

2,000 sales

1,500 sales

$3 profit per sale

$4 profit per sale

$6,000 profit

$6,000 profit

In this scenario, you end up with the same profit at the end of the year regardless of whether you lower the price or not. With this knowledge in hand, you can make the best decision for your business using actual analysis and not instincts alone.

By anticipating the impact of the competitor’s move on your own business in the short and long term, you can make better strategic decisions.

3. Determine Your Options and Your Own Best Competitive Strategy

When your market competitor makes a change to their business, you have an endless amount of responses available. To avoid a knee-jerk reaction, take time to list out all your potential moves and the impact of each.

It’s important to remember that when assessing what response to take, consider the relevant external factors—you’re not operating within a vacuum.

For example, if a competitor is stealing your best employees, an immediate response might be to raise your employees’ pay. However, this doesn’t consider other factors like rising inflation, which may already be eating away at your profit.

Increasing pay could be a short-term solution to losing valuable employees, but it could lead to long-term revenue issues, which may eventually cause you to cut back your employees’ hours—driving employees away again.

If you don’t take the time to analyze your options, you’re not going to consistently make the right decision. In the example above, the actual answer to keeping employees loyal could be unrelated to pay altogether. Maybe your employees want more flexible work schedules, better training, more ownership, autonomy, or any number of other non-monetary benefits.

Before making a decision, take a beat to assess all your options. You may even find that your best response is no response at all.

4. Make Your Move, Measure the Results, and Adjust If Needed

After you’ve made the decision on how to respond to your competitor’s move, the next step is to simply execute it and measure its results over time. While you may have estimated its impact prior to taking action, you should still track performance afterward—in case a change is needed.

For example, in the pricing example from step 2, we estimated a loss of 500 sales annually if the price was not lowered to $9. If you break this out monthly using seasonal sales trends from previous years, you should have a rough idea of how many sales you expect to lose monthly.

After three months without lowering the price, you can collect sales data for that product and compare it to what you forecasted. If sales are in line with what you expected, great! If they’re much worse than you anticipated, you may decide to pivot and lower your price.

Businesses must aim for agility when it comes to their competitive response. While not every scenario will allow the same flexibility of raising or lowering prices, a willingness to assess business decisions objectively and make swift changes as needed is what’s most important.

Competing in business comes with a lot of chance and unpredictability. What may have been the right decision from every analytical perspective could end up failing, and that’s okay. Don’t be afraid to be wrong—but when you are, be willing to correct it.

What is market share?

Market share refers to the entire consumer pie for a specific industry or market. It’s the percentage of total purchases for a product or service that a company makes up.

For example, if your business makes $100,000 a year and all your other competitors combined make $900,000, the entire market is $1M—of which you own 10%. Your market share of 10% means there is 90% of the market available to you.

The excess market share is your growth opportunity. With 90% of the market available, you can make strategic moves to begin capturing more of that share.

What are competitive strategies in business?

In business, a competitive move refers to a deliberate strategic change by one company with the purpose of increasing market share. Most competitive moves involve strategies related to pricing, product/service, customer relations, costs, or marketing and advertising.

When a competitor makes a strategic move, other businesses within that market must decide how to respond. This can create market pressures that lead to price wars, innovation, and other consumer-friendly benefits. In short, competitive moves are the driving force behind a free market.

How quickly should businesses respond to a direct competitor’s move?

When responding to competition, it’s best to act as quickly as possible after you’ve made your decision. However, it’s important to give yourself enough time to assess the situation from several vantage points.

First, you need to understand how the competitor’s move will affect your business, customer perception, other competitors, and the market as a whole. You then need to outline all your available responses and the impact each will have on your business.

With all this information in hand, you are now prepared to make an educated strategic decision—not simply the first or easiest choice.

Play the Cards You’re Dealt

Running a business is a lot like playing poker. You're competing against several others and all striving for the same goal (to win). You’re also constantly evaluating risks and making strategic decisions based on the information available—both present and historical. Finally, you’re not going to win every time, and you can’t dwell on the losses.

So, the next time you hear Kenny Rogers’ “The Gambler,” think about how that applies to running your business—especially as it relates to competing on Main Street. You may come away with more clarity and understanding of how to simply play the cards you’re dealt.

Opening your dental practice is exciting, but it comes with a significant increase in accounting responsibilities. Most dentists prefer to focus on client work rather than business management, but you can’t afford to neglect the function.

Here’s what you should know about dentist accounting to stay on top of your financial obligations, including what it involves, the most common mistakes to avoid, and some best practices that can help your system run smoothly.

What Is Dental Practice Accounting?

Dental schools are great at teaching prospective dentists how to care for their patients' oral health. However, they don’t share the knowledge dentists need to be effective small business owners.

When you open your dental practice, you become responsible for your dental practice accounting. That refers to everything necessary to keep your finances organized, make intelligent business decisions, and comply with tax laws.

More specifically, dental practice accounting involves:

Maintaining records of your day-to-day transactions

Paying your calculated tax obligations and filing tax returns to stay in compliance

Analyzing your financial statements to inform business decisions and tax strategies

The unique aspects of running a dental practice can complicate these processes. For example, accounting for your revenues properly despite the complexities of insurance billing can be one of the most significant challenges.

Even if you switch to a fee-for-service model, multiple moving parts in the dental payment process can quickly lead to messy financial records.

Problems can also arise when a dental practice owner plans to sell their business at the end of their career. While that’s a long-term financial goal, it creates many accounting challenges regarding practice valuation and retirement planning.

Best Practices For Dentist Accounting

Not only do busy dentists enjoy reducing their time doing accounting, but focusing on your craft is in your business's best interest. Maximizing the hours you spend on your core competency is highly beneficial to your profitability.

Here are some best practices you should follow to minimize the interference of your dental accounting responsibilities in your day-to-day working life.

Invest In Cloud-Based Software

Bookkeeping can be one of the most time-consuming aspects of small business accounting when you do things by hand. Fortunately, modern cloud-based software has made that entirely unnecessary.

Nowadays, all dental professionals should connect their business bank accounts and credit cards to solutions that can track their transactions and generate financial statements.

Fortunately, you can automate those functions with accounting software.

Of course, software can make many other aspects of your finances more efficient. For example, dental practice management and payroll service software are essential tools for many dentists.

Ideally, you want to create a tech stack that integrates seamlessly. While this can be costly, consider treating it as an investment, just like your practice’s equipment.

Optimize Your Legal Entity Structure

Business owners have multiple legal entity options, including sole proprietorships, partnerships, limited liability companies (LLCs), and corporations. In some industries, all of them are viable, but that’s usually not the case for dentists.

That’s because litigation is one of the most significant risks in the healthcare industry, and you can’t afford to leave yourself exposed. As a result, dentists generally must choose from corporate and LLC structures.

However, even those options have vastly different impacts on your taxes and accounting, and there’s no one-size-fits-all answer regarding the best choice. As a result, it’s a good idea to consult a tax or legal expert to help you make this decision.

Consider Your Billing Structure Carefully

Dental practices have multiple options when it comes to determining their billing structures, and they have a significant effect on your overall business strategy and accounting processes.

First, dental practices can go with the traditional route of being a participating provider. That means you’re in-network with a dental benefit plan and usually involves collecting payments from insurance companies and patients.

Generally, this favors a quantity-over-quality approach. Dentists accept the lower prices insurance companies set for their services in exchange for the consistency of capitation payments and increased patient volume due to insurance referrals.

Alternatively, dentists can switch to a fee-for-service approach, which involves setting your prices for services and collecting payment in full from patients upfront. You or the patient can still submit a claim to their insurer for reimbursement if there is one.

Typically, choosing the fee-for-service approach implies a shift to a quality-over-quantity strategy. You’ll likely have fewer patients, but your profit margins for each one should increase.

Your billing strategy is another hugely impactful decision you’ll need to make before you start doing business, and it’s best to ask an expert for help with all of the implications for your financial management and tax reduction planning.

Delegate As Much As Possible

Providing care to your dental patients is a full-time job, and every additional hour you can dedicate to your core competency increases the efficiency and profitability of your business.

As a result, dentists benefit more than most from delegating their financial responsibilities. It’s often worth paying for help with your bookkeeping processes and the more complex dental accounting services.

In many cases, it makes sense to bring the bookkeeping process in-house. It’s usually straightforward enough to have one staff member handle it with other administrative tasks like scheduling.

However, few practices need to hire a full-time dental accountant for their financial planning. Instead, you’re often better off paying for outsourced accounting and tax services from a Certified Public Accountant (CPA) firm.

They can provide all the dental practice accounting services you need at a much lower cost, including strategic tax planning, new business advisory, and tax preparation.

Just be sure you choose one who's had clients like you before, so they understand the nuances of accounting service for the dental industry.

Common Mistakes

Because dental education doesn’t prioritize financial management, it’s easy for new practice owners to make unforced errors. Fortunately, many of them are easily avoidable when you know about them in advance.

To help you set yourself up for success, here are some common pitfalls dentists fall into that you should know to avoid.

Failing To Separate Business Activities

Failing to open a separate business bank account for your practice’s transactions is one of the most common ways dentists cause accounting problems for themselves. It makes it surprisingly difficult to distinguish which activities belong in which category later.

Many businesses recognize this issue after their first few months or year of operations, but the damage is done by then. To avoid unnecessary accounting work, open separate business accounts before transitioning to practice ownership.

Neglecting Financial Analysis

Dentists are rarely excited by the prospect of financial concerns interfering with their craft, but you can’t afford to ignore that aspect of your responsibilities. Dental practices are businesses, so you must understand the monetary aspects to run them well.

That means you should take the time to explore your financial statements and look for ways to improve your profitability, cash flows, or operational efficiency.

For example, debt is one of the primary budgetary challenges for dental practice owners. Not only do dentists carry sizable student loans, but they also usually have to take out business loans to afford the equipment they need.

As a result, you’ll likely have high fixed costs, and you must be careful to avoid cash flow issues.

Choosing A Generalist Accounting Advisor

Every business is subject to the same fundamental accounting principles, but their applications vary significantly due to the nuances of each industry. As a result, choosing a generalist accounting advisor is often a mistake for dentists.

When shopping for a dental CPA firm, review their accountant websites carefully and take advantage of free consultation options. Make sure you choose one with extensive dental business consulting.

They'll need it to help you navigate the unique aspects of dentist accounting, like dental insurance and selling your practice.

*The information provided in this post does not, and is not intended to, constitute business, legal, tax, or accounting advice and is provided for general informational purposes only. Readers should contact their attorney, business advisor, or tax advisor to obtain advice on any particular matter.

Owning your own medical practice is an exciting prospect, but it comes with additional accounting responsibilities. While you’d probably prefer to focus on providing healthcare services to your patients, you can’t afford to ignore the business side of your operation.

Here’s what you should know about medical practice accounting to keep your financial systems running smoothly, including the unique challenges involved, some best practices to implement, and the most common mistakes to avoid.

How Is Accounting For Medical Practices Different?

The many years you spent in medical school were highly effective at preparing you to assist your patients. Unfortunately, they probably didn’t do as good a job of teaching you how to be a business owner.

As a result, healthcare professionals are often unprepared to manage their company’s accounting and tax responsibilities. To make matters worse, the unique nature of the healthcare industry creates financial issues beyond what most business owners face.

Generally, the most significant medical practice accounting challenges stem from the healthcare billing process. Most businesses provide a product or service to a customer, then receive a predictable payment from them in exchange.

Unfortunately, medical practices provide services to their patients but have to coordinate payment between them and their insurance companies. There are many more moving parts than usual, and it’s much easier for things to go wrong.

For example, medical coders make mistakes, patients fail to pay their bills, and insurance companies reject claims. As a result, medical practices must establish even more efficient systems for tracking and organizing data.

Best Accounting Practices For Medical Practices

As a healthcare provider, you probably want to focus on serving your patients and spend as little time as possible worrying about the financial health of your business. An efficient accounting system is essential for doing so without harming your practice.

Here are some best practices you can implement to optimize your accounting function and minimize the time you have to spend managing it.

Leverage Cloud-Based Software

The sheer complexity of medical practice accounting makes software essential for healthcare providers. It’s prohibitively difficult and time-consuming to keep track of everything by hand.

Fortunately, modern cloud-based software solutions can automate many of the most time-consuming aspects. That noticeably reduces the strain on your administrative staff with bookkeeping and accounting responsibilities.

Businesses often need to invest in multiple tools, but healthcare providers can meet most of their needs with practice management solutions (PMS). For example, they can usually facilitate processes like the following:

Scheduling appointments

Capturing patient details

Storing treatment plans

Billing patients and insurers

Insurance claim scrubbing

You may still need to acquire a few tools for whatever your PMS can’t help you with, such as accounting and payroll services. Before committing to any products, make sure you’ve chosen ones that can interface with each other seamlessly.

Use The Accrual Accounting Basis

Businesses generally have to choose between the cash and accrual accounting methods. Neither is inherently superior, but the accrual basis is generally better suited to medical practices.

The cash basis of accounting involves recognizing revenues when you receive them and expenses when you pay them. Meanwhile, the accrual basis recognizes revenues when you earn them and expenses when you incur them.

The cash basis is easier to implement, but it generates financial statements that poorly represent a medical practice’s profitability. Doctors often provide services and go without the corresponding revenues for months, if they ever receive them at all.

As a result, the accrual basis is much better at matching revenues with expenses and accurately representing your business's financial situation. However, it makes cash flow monitoring harder, so remember to track that separately.

Invest In Financial Education

One of the reasons healthcare providers often struggle to run their practices' accounting effectively is that business management is well outside their expertise. Fortunately, you can remedy that by investing in your own financial education.

Finance, accounting, and tax strategies aren’t the most exciting topics for most medical practitioners, but you don’t have to become a master. You usually only need to know enough to hire and manage people who run those functions.

Once you have an administrative staff in place, it’s a good idea to invest in their financial education as well. The more knowledgeable and reliable they are, the less that business will interfere with your day-to-day routine.

Delegate As Much As Possible

Providing medical services to your patients is more than enough work to occupy all of your working hours. It’s also the aspect of your business where your time generates the highest return, not to mention the one you probably enjoy the most.

As a result, delegating will benefit you even more than most business owners. Embrace the fact that you’re going to need help managing your medical practice accounting responsibilities, and don’t be afraid to pay for assistance.

Of course, labor is expensive, and you shouldn’t waste money unnecessarily. Fortunately, you don’t need to hire full-time workers for all your accounting functions.

For example, an in-house bookkeeper might make sense, but you’re probably better off using an outsourced accounting service for your more sophisticated financial needs.

A Certified Public Accountant (CPA) firm can provide all of the medical practice accounting services you need for a fraction of the cost, including proactive tax planning strategy, new business advisory, and business tax preparation services.

Common Mistakes

Healthcare providers rarely study business management during higher education. As a result, it’s easy for new practice owners to make mistakes as they transition into business ownership.

Here are some of the most common errors physicians make that you should know to avoid.

Lack Of Organization

Accounting for medical practices involves many more moving parts than accounting for most other businesses. As a result, it’s more important than usual that you set up systems to keep everything organized and running smoothly as soon as possible.

Here are some of the most effective steps you can take:

Separate personal and business accounts: Using the same bank accounts for your business and personal activities forces you to go back and split the two later. Separate them from the beginning to save yourself the trouble.

Customize your chart of accounts: Medical practices have nuanced revenues, expenses, assets, and liabilities. Creating particular accounts in your accounting software helps keep your bookkeeping accurate and actionable.

Keep track of your asset purchases: Medical practices need expensive equipment to run. Unfortunately, you need to capitalize and depreciate these costs instead of deducting them immediately, so keep separate records for them.

Whatever you can do to optimize your accounting from the start will pay dividends indefinitely, so be as diligent as much as possible from day one. Preventing accounting problems from occurring is much more effective than fixing them later.

Neglecting Financial Analysis

Healthcare providers can benefit significantly from automating and delegating significant portions of their accounting. However, that doesn’t mean you can ignore your medical practice’s finances.

Patient care can be your main priority, but your medical practice is also a business. As a result, you need to take the time to review your financial statements and reports to draw conclusions that can inform your business decisions.

For example, variable analysis is one great way to identify extraneous expenses and improve your overall profitability. It involves creating budgets for your expected costs, comparing them to your actual numbers, and investigating the differences.

While you can pay an accounting firm for help with a lot of this, you can't give up the financial controls altogether. You need to know enough to understand and assess any management solutions they suggest.

Choosing A Generic Accounting Advisor

While the same fundamental accounting principles apply to every business in the United States, the nature of the healthcare industry presents some unique issues. As a result, it’s usually a mistake to settle for a generic CPA’s medical practice accounting services.

The average CPA firm can handle basic small business accounting and tax services. However, if they’ve never worked with a busy medical practice before, they may not be able to develop effective medical practice accounting solutions.

When you’re looking through accountant websites, make sure you select providers who demonstrate a clear understanding of healthcare accounting challenges. Use the free consultation and ask each one how they deal with insurance and medical billing issues.

Here For Your Funding Needs

As you're growing and expanding your medical practice, you'll likely need access to additional capital. Lendio can help match you with the right lender for your medical practice loan.

All businesses in the United States follow the same fundamental accounting principles, but their application varies between industries. Because the hospitality industry has some unique financial quirks, hotel accounting can be particularly intensive.

If you're a hotel owner, here’s what you should know about accounting for your business, including what separates it from accounting in other industries, the most significant obstacles you’ll face, and some best practices that can minimize your issues.

How Is Hotel Accounting Different?

The fundamental challenge of accounting for hotel operations is relatively straightforward. In simple terms, there’s much more financial data to document, organize, and analyze in the lodging industry than in most others.

The rules aren’t any more sophisticated than usual, but running a profitable hotel business often requires managing many different income streams and a diverse set of expenses.

While room rentals are a hotel’s primary offering, their supplemental revenue streams can still be significant. They often have their own unique costs, and running them may require accounting for them separately.

In addition, hotel activities are virtually endless and generate transactions every day of the year. Unlike other businesses that close at the end of the day and shut down entirely for a couple of days a week, hotels do business at all hours and every day of the year.

As a result, everything from maintaining organized, accurate financial records to analyzing operational data for decision-making purposes becomes significantly more difficult.

Accounting Challenges Faced By Hotels

Ultimately, the primary challenge of hotel accounting is establishing systems that can effectively organize and analyze the overwhelming amount of data involved. To help you tackle the problem, here’s a more in-depth explanation of the factors contributing to it.

Ceaseless Operations

One of the most significant contributors to the challenge of hotel accounting is that hotels rarely close. In most cases, hotels are open for business 24 hours a day, 365 days a year.

After all, their primary offering is a place for people to stay, and there’s always demand for it. Demand is often even higher on holidays when many other businesses are closed since people tend to travel away from home around those days.

As a result, hotels have new transactions to deal with daily, which creates a constant strain on the staff members responsible for maintaining financial records. For example, this typically necessitates a “night audit.”

Now a standard in the hotel industry, the night audit is an after-hours process that involves confirming room statuses, documenting no-shows, reconciling guest transactions, and everything else necessary to close the books for the day.

Multiple, Unrelated Activities

Hotels generate the vast majority of their revenues by renting out their rooms. However, many of them have multiple additional income streams that range from tangentially related to completely separate from their primary offering.

For example, hotel revenues can come from room rentals, room service, meeting space rentals, on-site restaurant and bar sales, valet and parking charges, vending machines, spa and massage services, gift shops, in-room minibars, movie rentals, and more.

It might not make sense to account for all of these activities separately. However, if a few are significant enough to impact profitability, it’s often worth breaking out the related transactions to help managers handle them effectively.

For example, a hotel with a popular on-site bar would need to keep track of its revenues and expenses separately to maintain the supplies necessary to maximize profitability and operational efficiency.

Varying Room Rates

Setting room rates is one of the most unique and complex aspects of hotel accounting. Though software exists that can organize the necessary data and help with the challenge, it’s not perfect, and human input is still often needed.

Once again, the sheer scope of the data to consider is what makes this so challenging. For example, all of the following have some impact on the ideal price of your hotel rooms:

Seasonality

Days of the week

Competitor prices

Customer expectations

Current occupancy rate

Minimum price to cover costs

Accounting for all these variables while setting prices is a delicate process, even for experienced hoteliers using hotel management software. Setting prices too high can scare off customers, but setting them too low means leaving money on the table.

Complex Payroll Costs

Few businesses have a staff as diverse as the army of workers that hotels need to employ to function effectively. For example, even a small hotel with simple amenities and offerings would need to hire all of the following:

Front desk staff

Housekeepers

Security

Management

Valets

Culinary staff

In addition to the many different functions they need to fulfill, these workers often have vastly different compensation formats. Hotels usually have both full-time and part-time workers, with some receiving tips and others not.

Unfortunately, hotels need to account for these labor costs accurately and timely so their managers can staff effectively. Otherwise, they risk wasting money by overstaffing for slow periods or overwhelming employees by understaffing in busy times.

Increased Managerial Accounting Requirements

Another reason accounting can be more challenging for hotels than other businesses is that there’s a greater need for managerial accounting processes in the hospitality industry.

Managerial accounting involves organizing your financial reporting in a way that helps managers make intelligent business decisions, and it’s essential for hotels. They need financial information to set room rates, hire staff, and determine budgets.

For them to do so effectively, you can’t lump your hotel’s activities together. It obscures the numbers relevant to individual income streams, and hotel managers need more specific accounting data than revenue and expense totals.

As a result, a significant portion of hotel accounting involves matching transactions to the correct activities so managers can generate the financial reports they need to make intelligent choices.

Best Practices For Hotel Accounting

Hotel accounting can be challenging, but you can mitigate many of the most troublesome issues with preparation, organization, and automation. Here are some best practices you should follow to ensure your accounting system is as efficient as possible.

Choose An Accounting Basis Carefully

Hotels can choose between using the cash or accrual methods of accounting. Both have pros and cons, but the best option depends primarily on the size of your operation. If you choose incorrectly, you could cause yourself significant accounting issues later.

The cash method involves recognizing revenues when you receive payments and deducting expenses when you pay them. It’s generally easier to implement, but it’s also the less accurate of the two.

It generally does a better job of measuring your company’s cash flows than its actual profitability. As a result, it’s usually only suitable for small hotel businesses like bed and breakfasts.

Meanwhile, the accrual method involves recognizing revenues when you earn them and deducting expenses when you incur them. It also requires that you keep track of your accounts payable and receivable.

These additional complexities make it harder to execute, but accrual financial statements paint a more accurate picture of your business’s profitability and financial position. Managers, investors, and lenders all prefer them for that reason.

As a result, accrual accounting is often better for larger, more sophisticated hotel businesses. Keep that in mind if you plan to scale your hotel operation up over time.

You might want to use the cash method at first, then change to accrual as you grow, but switching can be difficult. If you plan to use accrual eventually, it may be better to do so from the start.

Take Advantage Of Software

Bookkeeping can be one of the most intensive aspects of hotel accounting. Theoretically, it involves the least amount of critical thinking, but the volume, diversity, and unending flow of transactions make it difficult to handle the function manually.

As a result, accounting software is essential for tracking your hotel’s activities efficiently. However, while generic tools are effective for many small businesses, they may not meet the complex requirements of many hotels.

The more your business grows, the more likely you'll need advanced industry solutions. For example, if you’re running a group of hotels, you’ll need a property management system that can handle all of your locations from a single dashboard.

Fortunately, many hotel accounting software options exist with a broad range of capabilities. The right accounting solution will depend on your tech stack, level of sophistication, and growth expectations, so explore your choices thoroughly.

If you choose a less comprehensive option to keep the cost down, you may need to supplement it with additional tools, such as payroll, booking, or point-of-sale software. Keep those extra potential expenses in mind as you shop.

Optimize Your Night Audit

Hotels usually need to perform nightly audits to ensure the accuracy of their complex financial records. These involve taking steps like confirming room statuses, posting room charges, and preparing financial management reports.

Because these audits are a daily occurrence and critical to the success of your accounting function, it’s worth taking the time to optimize them. Otherwise, they can become one of the most tedious and time-consuming aspects of your business.

To make the process as efficient as possible, consider doing the following:

Systematizing your night audit training

Documenting step-by-step instructions for the process

Training multiple employees to complete night audits

Investing in software to automate the audits as much as possible

Because these reconciliations need to happen nightly, you don’t want to rely on one accounting team member to complete them. They won't be available every day of the year, but your hotel has to be.

In addition, you want it to be relatively easy to train someone new to complete the process. Otherwise, losing one or two key team members could cripple your accounting department.

Get Expert Help

Almost every business can benefit from expert accounting services, and hotels are no exception. Running a hotel is more than a full-time job, so you’ll probably need to pay others to handle your business’s more sophisticated accounting needs.

In addition to the accounting manager responsible for recording daily transactions and other bookkeeping activities, it’s best to get assistance from a Certified Public Accountant (CPA) knowledgeable in hotel accounting services.

In addition to verifying the accuracy of your balance sheet and income statement, they can provide personalized tax planning, cash flow and financial analysis, budgeting, and forecasting services.

One of the best ways to get these kinds of accounting services without paying for another full-time hotel accountant is to hire an outsourced CPA firm. Just make sure you choose one with experience in the unique challenges of hospitality accounting.

*The information provided in this post does not, and is not intended to, constitute business, legal, tax, or accounting advice and is provided for general informational purposes only. Readers should contact their attorney, business advisor, or tax advisor to obtain advice on any particular matter.

Opening your own law firm is an exciting point in your legal career, but you can’t get so caught up that you neglect the financial aspects of owning a business. To keep your company running smoothly, you must stay on top of your accounting responsibilities.

Here’s what you need to know to establish and maintain an effective accounting system for your law firm. We’ll cover the unique accounting challenges lawyers face, some general best practices to follow, and the most common pitfalls you need to avoid.

How is accounting for law firms different?

Fortunately, most accounting concepts for law firms are relatively straightforward. The finances of service providers tend to have far fewer moving parts than those of businesses with an inventory on the books.

However, there are a couple of unique aspects to law firm accounting, and managing them can be challenging. Most notably, lawyers often hold onto funds that don’t belong to them, and specific rules govern how you need to handle that cash.

For example, lawyers may collect settlement funds on behalf of their clients. Not only do you have to keep these funds separate from yours and your firm’s, but even mingling them with other clients’ funds can be problematic.

In addition, you may need to use clients’ funds on their behalf, in which case you must provide detailed reports about your activities to remain in compliance.

That’s known as trust accounting, and you should understand the guidelines thoroughly before opening your own law office. If you make a mistake and violate the rules, it could cost you your law practice or your license.

In addition, law firms sometimes pay for expenses on behalf of their clients using the company’s funds. These aren’t tax-deductible expenses and can muddy your financial records if you’re not careful.

Bookkeeping vs. accounting for law firms

Before proceeding further, let’s clarify the difference between bookkeeping and accounting. The two functions are closely related, and there’s often some significant overlap between them. Accountants may provide bookkeeping services, and bookkeepers frequently need to know accounting fundamentals.

However, they’re still distinct, at least theoretically. Bookkeeping for a law office involves recording your day-to-day transactions and maintaining clean financial records. It’s an almost administrative task that involves relatively low levels of critical reasoning.

As a result, lawyers can automate a significant portion of their bookkeeping using accounting software. Subsequently, they can often handle the aspects that require a human touch personally without much training.

Conversely, accounting for law firms is more complex. It involves verifying bookkeeping data and using it to generate financial statements and facilitate processes like tax planning and cash flow analysis.

Much like practicing law, accounting requires extensive training and in-depth knowledge of intricate rules. Making mistakes can lead to penalties and interest or audits from the Internal Revenue Service (IRS).

As a result, it’s unwise for lawyers to attempt to handle their law firm’s accounting without assistance from an expert. It’s usually best to pay for a Certified Public Accountant’s (CPA) tax services.

Best practices for lawyer accounting

Staying on top of your law firm’s accounting responsibilities while providing legal services to clients can be a significant challenge. Here are some practices you should follow to minimize the burden and set yourself up for success.

Open Separate Accounts Before Going Into Business

Every small business owner should have a separate bank account for their personal and business activities. Splitting your funds makes it much easier to determine which of your transactions belong in each camp.

Many new small business owners make the mistake of diving head first into growing their operations without taking this step. Unfortunately, that often makes filing their first tax return a headache since they must go back and sort out what belongs where.

That’s challenging in any industry, but it can be especially difficult for a small law firm. Not only do you have to keep track of which transactions are personal and which are business, but you also need to know which costs you incur on behalf of your clients.

If you need to go back at the end of the year and sort your financial data into all three categories, it’ll be a nightmare. As a result, you should open a separate checking account and credit card for your legal practice before you start taking on clients.

Implement Job Costing

Preventing messes before they occur instead of cleaning them up afterward is a common theme in many lawyer accounting best practices. One of the most important ways of doing this is to develop an organized bookkeeping system as soon as possible.

For example, job costing is a strategy lawyers can use to ensure their financial records are easy to interpret and analyze. It’s a form of cost accounting that involves assigning every expense you incur to a specific project.

For businesses like law firms whose operations revolve around clearly distinct jobs, it’s one of the best ways to organize expenses. It’s especially beneficial when you employ other lawyers, as it can help you set a profitable hourly rate when billing your clients.

Take Advantage Of Software

Continuing with the theme of setting yourself up for success from day one, make sure that you take advantage of software’s ability to streamline your accounting processes as soon as possible.

At the very least, you should leverage accounting software to track your transactions. There’s no reason to manually enter transactions anymore with so many affordable options available.

However, most lawyers shouldn’t settle for generic software. Attorney-specific accounting software exists, and it can facilitate many more aspects of running your business, including:

Time tracking software that integrates with your invoices

Client intake, scheduling, and relationship management

Automatic trust account updates and reconciliations

Many different solutions are available, and each can offer you a unique combination of benefits. Make sure you review them carefully and determine which tool makes the most sense for your business in its current stage of development.

Consider The Cash Accounting Basis

One of the most significant decisions small business owners have to make in the early days of their company is which accounting basis to follow for tax purposes. Generally, the two allowable options are the cash basis and the accrual basis.

The cash basis of accounting involves recognizing revenues when you receive cash and deducting expenses when you pay them. Because it’s the easiest to implement, lawyers often prefer this method. The American Bar Association also recommends it.

Meanwhile, the accrual basis of accounting involves recognizing revenues when you earn them and expenses when you incur them. That requires significantly more expertise and forces you to keep track of accounts receivable and payable.

You’ll often hear that the accrual basis is worth the extra work because it’s more accurate, but that’s primarily true for businesses that carry inventories. The IRS requires companies with inventories and revenues above $26 million to use it.

Meanwhile, a legal business can use the cash basis no matter their revenues, and it often represents their activities more accurately. As a result, many lawyers can avoid a lot of trouble by electing the cash basis.

Stay On Top Of Your Tax Obligations

One of the most significant changes you face when transitioning from full-time employment to business ownership is the loss of tax withholding benefits. As a result, you must make estimated tax payments each quarter.

These payments are to cover your federal and state income taxes as well as your self-employment taxes. If you don’t make them on time or pay much less than you should’ve, you may incur penalties and interest.

If you expand your operation and hire employees or structure your business in a way that involves paying yourself a salary, you’ll also have to worry about payroll taxes. These are also due throughout the year, usually bi-weekly or monthly.

Ultimately, it’s unwise to try and navigate your tax obligations alone. The last thing a new law firm needs is to get on the wrong side of the IRS. Consider consulting with an accounting firm to clarify your responsibilities and ensure you’re meeting them.

Get Expert Help

Finally, one of the best ways to lessen the burden of accounting for your business is to pay someone to help you with it. Not only is accounting complex, but it’s also time-consuming, and you have other responsibilities.

Fortunately, you usually don’t have to hire a full-time accountant for your law firm. That’s often expensive and unnecessary. Instead, consider paying for outsourced accounting services from a CPA firm.

It’s a lot like businesses that engage a law firm for their needs instead of hiring an in-house lawyer. You’ll pay far less and get only what you need. Just be sure to choose a CPA experienced in providing law firm accounting services.

Common mistakes

As a lawyer, you can appreciate the time and effort that goes into becoming an expert in a complex field. Unfortunately, accounting and tax rules can be every bit as convoluted as any area of study in the legal industry.

Since law school doesn’t cover these subjects, it’s easy for new law firm owners to make financial mistakes. Here are some of the most common pitfalls you should know to avoid.

Underestimating Accounting Duties

When lawyers decide to open their firm, accounting is rarely at the top of their minds. After all, you have many more exciting things to pull your attention, such as winning clients and providing services.

As a result, it’s easy to make accounting a secondary priority thinking you can always deal with it later. Unfortunately, that attitude leads to some of the most frustrating accounting situations.

For example, you could discover once it’s time to file your return that you owe penalties and interest for missing your estimated tax payments or that your accounting records are in such disarray that you have no idea how to untangle them.

Remember, it’s always better to prevent problems than to try and solve them after the fact. If you’re planning to open your own law firm, make sure you give your accounting the attention it’s due sooner rather than later.

Misattributing Transactions

Whether it’s mixing up your business and personal transactions or deducting an expense from the wrong client trust account, it’s easy for law firm owners to record transactions incorrectly.

As a result, you must develop a habit of performing regular reconciliations to ensure that your financial records are in order. It’s typically best to perform bank reconciliations for your business checking accounts each month.

In addition, all state bar associations require law firms to perform three-way reconciliations monthly or quarterly. That involves confirming that your trust ledger, client ledgers, and trust account statement balances agree with each other.

A trust ledger records all the transactions impacting your trust account. Client ledgers record those same activities but assign each one to a specific client.

Mismanaging Trust Accounts

Managing trust accounts is one of the unique aspects of legal accounting, and the consequences of mishandling them can be significant. Not only will you incur fines, but you could also lose your license or face legal repercussions.

You might think that keeping your clients’ funds separate from your own sounds simple enough, but it’s surprisingly easy to violate trust accounting requirements.

For example, many banks are unfamiliar with lawyer trust accounts. As a result, you could accidentally use a regular business checking account to store your clients’ funds, which violates trust accounting rules.

As a result, you need to understand your trust account responsibilities thoroughly. Take the time to master what constitutes professional conduct. For example, you should understand all of the following:

Taking funds out of trust accounts: While you must pay taxes on advance fees in the year you collect them under the cash method, you can’t take them out of your trust account until you earn them. Unfortunately, it can be hard to determine when lawyers can say they’ve earned their advance funds and retainers.

Pooling client funds in one trust account: Generally, lawyers that hold relatively small amounts of money for a short time from multiple clients place them all in a single trust account. However, a significant sum from a single client should have its own.

Interest on Lawyer Trust Accounts (IOLTAs): Traditional trust accounts may or may not earn interest, but IOLTAs do. However, lawyers can’t keep the interest their clients’ funds generate. Instead, IOLTAs automatically go toward charitable purposes.

Once again, it’s best to master the trust accounting rules well before you go into business for yourself. It’s one area you can’t afford to make mistakes because there’s rarely a chance to fix them later.

Running a manufacturing company while managing its books is a challenging prospect. Manufacturing involves a significant amount of cost accounting, which is a notoriously complex subject.

Here’s what you need to know to navigate manufacturing accounting successfully, including the best practices for the industry, the most complicated processes involved, and some fundamental terms.

Manufacturing accounting tips.

Manufacturing accounting follows the same fundamental principles as accounting in other industries, but there are many more moving parts than usual. Let’s look at some general best practices you should follow to optimize your accounting system.

Leverage manufacturing software.

Bookkeeping is one of the most time-consuming aspects of manufacturing accounting. Maintaining accurate and organized records of all the transactions and costs involved in production can be incredibly laborious if you do it manually.

However, manufacturing accounting software can automate a significant portion of this responsibility. You or an accountant should still perform reconciliations to confirm the accuracy of your financial records, but it’s much easier than doing everything by hand.

Invest in your financial education.

While you probably won’t handle all your business’s accounting personally, you still need to understand it. A lot of manufacturing accounting revolves around creating records that managers can use to inform business decisions.

As a result, it’s worth investing in developing a deeper understanding of the related accounting and tax rules. If nothing else, it’ll help you analyze your financial statements and reports to improve the efficiency of your business.

Choose your accounting basis carefully.

Because manufacturing businesses carry an inventory, the Internal Revenue Service (IRS) requires them to use the accrual basis of accounting. However, there’s an exception for small businesses with less than $26 million in average annual revenues.

As a result, your manufacturing company may get to choose between using cash or accrual accounting. While the cash method is often easier to implement, it’s not always the best way to organize your financial records.

Because you must get special permission from the IRS to change your accounting basis later, it’s best to get it right the first time. Consider consulting an expert before choosing one or the other.

Get expert assistance.

Getting expert tax and accounting advice is worthwhile for virtually every business. A Certified Public Accountant (CPA) with experience in your industry can provide valuable financial insight and ensure you meet your tax obligations.

Fortunately, you don’t necessarily have to hire an accountant full-time for your manufacturing business at first. Outsourced accounting from a CPA firm is less expensive and may be enough to meet your needs.

What type of accounting is used in manufacturing?

The primary type of accounting used in manufacturing is known as cost accounting. It’s a form of accounting that tracks production costs in a way that managers can use to inform business decisions.

As a result, cost accounting is less about creating financial statements for third parties and more about facilitating various forms of internal analysis. For example, manufacturing businesses use cost accounting to complete processes like the following:

Budgeting: Manufacturers must create budgets for each stage of the production process to ensure they stay on track and set appropriate sales prices. Cost accounting tracks historical production costs, which helps create more accurate estimates for future activities.

Constraint analysis: This involves isolating potential bottlenecks in your manufacturing and improving them to increase overall efficiency. Organizing your production costs helps managers determine which resources limit their output most and plan accordingly.

Margin analysis: This involves calculating all the costs associated with an aspect of production, then subtracting them from the revenue it generates. That gives you each aspect’s marginal profitability, which managers can use to find the most lucrative products, customers, or channels and inform business decisions.

In addition, manufacturing involves inventory management accounting. Because manufacturers carry significant inventories, they need to know how to track their costs to create accurate financial statements and comply with accounting standards.

Cost-flow assumption methods.

Your cost of goods sold and ending inventory values play a significant role in your manufacturing business’s profitability. Because that directly affects your tax liability, the IRS requires that you use specific methods to calculate both numbers.

These are the inventory tracking methods they accept for manufacturing businesses.

Specific identification

The specific identification method is the most straightforward option. It involves keeping track of each item in your inventory. If that’s feasible for your business, the Internal Revenue Service (IRS) requires you to use this method.

However, specific identification is usually only possible for manufacturing businesses that produce a low volume of differentiated products. For example, car manufacturers may use this approach, but a stapler manufacturer probably wouldn’t.

FIFO

If you can’t keep track of every item in your inventory because the units are interchangeable, you must assume which ones you sell first. While you can’t know for sure which you sell first, this keeps your books organized.

The first-in-first-out (FIFO) inventory valuation method assumes that the first unit you manufacture is the first one you sell. FIFO is generally the most popular approach, especially for manufacturers of products with limited shelf lives.

LIFO

The last-in-first-out (LIFO) inventory valuation method is the opposite of the FIFO approach. It assumes that the last unit you produce is the first one you sell.

Because prices tend to rise over time, the LIFO method generally maximizes your cost of goods sold and minimizes your closing inventory values. As a result, it also leads to the lowest possible net income, which is beneficial for tax purposes.

However, LIFO is controversial among regulators. The International Financial Reporting Standards (IFRS) prohibits it, and businesses in the United States may not be able to use it forever.

Weighted average

The weighted average cost flow assumption is between FIFO and LIFO. It involves calculating the weighted average cost of all units available for sale during a given period. You then assign that cost to your goods sold and ending inventory.

The weighted average is generally the least common cost flow assumption for manufacturers. In fact, the IRS previously dismissed this method as inaccurate, only allowing businesses to use it for tax purposes in 2008.

Production costing methods.

Production costing methods organize your cost accounting records to help management make decisions. Depending on your business model, you may prefer to structure your accounting around individual units, product lines, or processes.

Here are the most popular production costing methods for manufacturers. Keep in mind that the terminology for these approaches can vary between sources.

Standard costing

Standard costing is one of the most common production costing methods among manufacturers. It involves calculating a standard rate for groups of costs that go into each unit, including direct materials, direct labor, and manufacturing overhead.

This approach to production costing helps with creating and refining budgets. When you can estimate how much it’ll cost to produce each unit, you can gauge your progress during each accounting period.

Variance analysis, which involves comparing your standard costs to your actual expenses, is a great way to reveal areas of overspending, improve production efficiency, and increase cash flow.

Job costing

Job costing organizes your accounting around each unit. It involves tracking the costs for every item you produce, including direct materials, direct labor, and manufacturing overhead. It’s also popular in construction accounting.

This approach is primarily beneficial for manufacturers who produce a relatively low number of unique products. For example, a manufacturer of made-to-order furniture would likely employ job costing.

Manufacturers of highly differentiated products need to track costs for each unit so they can set prices appropriately and monitor the profitability of their products.

Process costing

If job costing is ideal for manufacturing businesses that produce lower numbers of unique products, process costing is for those that create a high volume of homogenous units. For example, a cement manufacturer might use this method.

Process costing involves tracking the cost of each stage of production. It helps facilitate analysis and efficiency refinement for businesses that revolve less around each unit and more around repetitive procedures.

Activity-based costing

Activity-based costing (ABC) is a way to assign indirect manufacturing costs like overhead to products or processes. Though it takes more work than applying a standard overhead rate, it generates more accurate cost estimates.

ABC systems involve sorting your business’s indirect costs into groups, calculating a per-unit rate based on their primary cost drivers, then using that rate to allocate costs to products or activities. It helps businesses factor indirect costs into pricing.

Basic manufacturing cost terms.

Deciphering jargon can be a frustrating challenge when you’re learning to navigate the complexities of manufacturing accounting. Here are brief explanations of some fundamental terms you’ll need to know to succeed.

Direct materials

Direct materials refer to the raw materials that manufacturers transform into finished products. That includes everything you can readily identify as going into a unit. For example, wood and screws are direct materials for table manufacturers.

Direct labor

Direct labor includes the cost of workers who transform raw materials into finished goods. For example, say you’re a table manufacturer. The wages of the worker who assembles the tables are direct labor, but not the salary of the janitor who keeps your factory clean.

Direct costs

A direct cost is an expense that you can easily trace to product manufacturing processes. Direct expenses primarily include direct labor and direct materials.

Manufacturing overhead

Also known as factory overhead, manufacturing overhead refers to the cost of maintaining and operating your production facilities. Overhead costs include expenses like factory rent, utilities, and administrative costs.

Indirect costs

Indirect costs are those that you can’t tie directly to the production process. Instead, you must allocate each indirect cost to your products using various methods to determine the value of each unit. It primarily refers to manufacturing overhead.

Fixed costs

In manufacturing, fixed costs remain consistent no matter how many units you produce. For example, that might include rent for your factory or interest payments on a business loan.

Variable costs

Variable costs change depending on the number of units your manufacturing firm produces. For example, direct materials and direct labor are both variable costs.

Cost of goods sold

The cost of goods sold includes all direct and indirect costs associated with the products you sell during a given period. It typically refers to direct materials, direct labor, and manufacturing overhead. Its value depends on your cost-flow assumption.

Cost of goods manufactured

Your cost of goods manufactured includes all direct and indirect costs that go into the products you finish producing during an accounting period. Like the cost of goods sold, it generally refers to direct materials, direct labor, and manufacturing overhead.

WIP inventory

Work-in-process (WIP) or work-in-progress inventory refers to products that have made it through part of the manufacturing process but remain unfinished. Though they’re not ready for sale, these goods are still an asset on your balance sheet.

Finished goods inventory

Finished goods inventory refers to the units that have made it through the production process and are ready for sale. You must use cost-flow assumptions and inventory valuation methods to calculate the balance.

Staying on top of your business’s accounting while running the operation is often challenging, but it can be particularly complex in the retail industry. Retail stores face at least one significant challenge that many others don’t.

Here’s what you need to know about retail accounting to navigate it successfully, including what makes it different, how to approach its most complicated aspects, and some best practices to keep in mind.

The primary reason retail accounting is different from accounting in other industries is that retail stores must keep track of their inventories. In contrast, a service business’s financial system usually has fewer moving parts.

Meanwhile, retail businesses can have extensive, diverse inventories that change constantly. Stores may hold large quantities of many different products and sell a high volume of units each business day.

Unfortunately, inventory accounting is essential for creating accurate financial statements and reports. In most cases, it’s simultaneously your business’s most significant asset and expense.

Not only is having inventory numbers necessary when creating financial statements to inform your tax strategies, but it’s also vital for performing cash flow analysis and making financial projections.

For every period, retail stores need to know their beginning inventory, units sold, and the amount left on hand. Otherwise, they may struggle to meet expected demand without buying too many units and impacting their cash flow management.