Facing an SBA loan default can be a daunting experience, but you aren't alone. In February 2025, a Senate Committee hearing was held to discuss the ballooning rate of early defaults in the SBA 7(a) loan program. In 2024, over 1% of small business owners defaulted on their SBA loans in the first 18 months.

If your small business is at risk of defaulting, or has already defaulted on your SBA loan, understanding the implications and exploring available options can provide a path forward. This guide will cover what happens if you default on an SBA loan, managing SBA loan defaults, and your options for next steps.

What is an SBA loan default?

An SBA loan default happens when a borrower has continually failed to make the agreed-upon payments, and hasn't come to any resolution with their lender. Defaulting on an SBA loan, or any loan, can have negative impacts on your business, and potentially lead to steep legal or financial consequences.

If you're worried you may not be able to make your agreed-upon payments, reach out to your lender to explore your options before the situation progresses to a default.

The difference between SBA loan default and SBA loan delinquency

As mentioned above, a default happens when you missed your payments and haven't worked things out with your lender. However, an SBA loan doesn't go into default immediately.

Before this stage, usually when you first miss payments, your loan will be classified as delinquent. Your lender will begin to reach out over missed payments. After a period of time, on average three to four months, your loan will default if you have not paid your past due amount or contacted your lender.

What happens if an SBA loan goes into default?

Once an SBA loan goes into default, things get serious. Although time frames will vary depending on lender and loan terms, usually a lender will issue a formal demand letter for the amount due. You will then have 30-45 days to pay the entire amount.

Failure to do so means the lender can use several other measures to collect the amount due.

Asset Seizure

Any collateral that you used to secure your loan, such as business bank accounts, real estate, inventory, or equipment, can be seized by the lender and sold to recoup their losses.

A lender can also seize and sell your personal assets if you’ve filled out an SBA loan personal guarantee. The personal guarantee form is required for most SBA 7(a) loans from anyone who owns 20% or more of the business. This also applies to any other owners or individuals who signed personal guarantees.

Depending on asset seizure specifics, or if the assets seized are not enough to cover paying off the loan in full, you may face lawsuits at this stage.

Lender files with the SBA

The lender will also file a claim with the SBA for the guaranteed portion of the loan, and turn the remainder over to the SBA, who will take over attempts to collect on the loan. Generally, a borrower must be in default for more than 60 calendar days before a lender can put in a loan purchase request with the SBA.

SBA takes over account and attempts to collect

The SBA will repay the lender the guaranteed portion of the loan to recover their losses, but will continue to attempt to collect payment from you. In most cases, the SBA will issue a 60-day demand letter, which details that you must respond within 60 days, or your account will be turned over to the U.S. Treasury Department. At this point, you can repay the loan, or submit an offer in compromise.

Submitting an offer in compromise (OIC) is an option when you have genuine financial hardship. It's a settlement that the SBA will consider for eligible businesses, but it's not guaranteed, and the amount of forgiveness that the SBA will consider is subject to a number of factors.

The U.S. Treasury will step in

If payment and settlement is not reached, the SBA can contact the Treasury Department with either a notice to the Treasury Offset Program (TOP) or an Administrative Wage Garnishment (AWG) notice to an employer. With the former, the TOP allows the government to take a portion of federal wages or social security benefits that you're owed, as well as seize vendor payments and/or income tax refunds.

An AWG allows wages to be garnished for up to 15% of disposable income (net pay after deductions). There is no statute of limitations for either TOP or AWG methods, and they will remain in place until the debt is paid, including interest and collection fees.

Communicate with your lender if you can't pay back a small business loan

Taking immediate action is crucial when you face a situation where you can't pay back a small business loan, as the consequences can escalate rapidly. Communicating clearly and transparently with your lender helps you both explore alternative solutions, such as restructuring payment terms, or arranging a temporary deferment until you can resume payments.

Maintaining communications also demonstrates your goodwill, which can help prevent the situation from progressing to more drastic collection methods.

Usually, a lender can offer two main types of assistance in this situation. Loan modification, or loan deferment, to help you through the situation until your business is in a better state to manage payments.

Loan modification

A loan modification refers to changes to the terms of the loan. For example, your lender could give you a term extension to push back the loan maturity date. This approach can provide immediate relief by reducing the size of your periodic payments, which can ease the cash flow burden on your business.

Lenders may temporarily or permanently alter interest rates, which can lower repayment costs. Some lenders may also consider offering a temporary reduction in interest payments, with any deferred amounts added to the loan balance. However, it's important to thoroughly discuss these options with your lender to understand the long-term implications. Modifications can extend the loan duration and affect your future business financial planning.

Loan deferment

A loan deferment can work as a short-term solution for businesses in a difficult period of cash flow. Typically, a lender can defer your loans for repayment for three, six or sometimes even twelve months.

Your lender often provides you with short-term solutions to bridge financial hardship when it comes to paying your SBA loan back. If this is simply not an option, then these solutions will only delay the inevitable. In this case, if you cannot repay your loan, then proactively pursuing an Offer in Compromise with the SBA is a route to settle your debt for less than the owed amount.

The bottom line

Defaulting on an SBA loan can have serious repercussions both personally and professionally. However, by understanding the default process and proactively seeking solutions, before the situation progresses too far, you can navigate these challenges more effectively.

Explore all options, maintain communication with lenders, and seek professional assistance when necessary. These steps can lead to a resolution that aligns with your financial and business goals, helping you regain control and stability.

To learn more about managing SBA loan defaults and discovering potential pathways for debt relief or forgiveness, consider reaching out to financial advisors who specialize in small business loan challenges. Your journey to financial stability and business success is not one you have to navigate alone.

Need quick, flexible financing for your small business? An SBA line of credit might be your best bet.

SBA lines of credit offer low interest rates, government-backed security, and the ability to draw funds as needed. They're perfect for covering cash flow gaps, seasonal expenses, and unexpected costs.

How do you qualify? And which SBA line of credit is right for you? We'll break it down below.

What is an SBA line of credit?

The Small Business Administration (SBA) offers an SBA line of credit through its SBA CAPLines program—a subset of the SBA 7(a) program, which is designed to provide ongoing working capital to small businesses. The SBA offers both revolving and fixed lines of credit options to choose from.

Revolving line of credit

A revolving line of credit works much like a credit card. It offers a source of funds that the borrower can draw from as needed. The main advantage of a revolving line of credit is its flexibility. You can access the funds, repay the amount used, and then draw again, as long as you don’t exceed your credit limit. This type of line of credit is especially useful for businesses with fluctuating cash flow needs.

Fixed line of credit

On the other hand, a fixed line of credit—also known as a traditional or standard line of credit—works differently. Once the funds have been drawn and utilized, they can’t be accessed again, even after repayment. This type of credit is most suitable for businesses with predictable and steady financial needs. It provides a one-time lump sum of money that is repaid over a set term.

SBA loan vs. SBA line of credit

While both SBA loans and SBA lines of credit provide small businesses with the financing they need, they differ significantly in structure and usage. An SBA loan is a lump-sum amount borrowed at one time and repaid in fixed monthly installments, often used for significant, one-time expenses, such as purchasing equipment or real estate.

On the other hand, a line of credit offers more flexibility. It establishes a maximum loan balance and allows businesses to draw funds as needed, making it ideal for managing cash flows or unexpected business expenses. Because of this flexibility, an SBA line of credit often has a slightly higher interest rate than an SBA loan.

Types of SBA CAPLines

SBA offers four types of CAPLines up to $5 million to meet different business needs:

- Seasonal line of credit – This type of line is suitable for businesses that experience seasonal changes in their cash flow, such as retail or tourism businesses.

- Contract line of credit – This type is ideal for businesses that need funds to finance specific contracts or projects.

- Builders’ line of credit – This type is designed for businesses in the construction industry to cover the costs of labor, materials, and other expenses.

- Working capital line of credit – This general-purpose line of credit is built to support ongoing business operations.

SBA Express Line of Credit

In addition to the four types of SBA CAPLines, the Small Business Administration also offers an SBA Express Line of Credit.

This type of funding offers expedited processing times, making it an ideal solution for businesses in need of quick access to capital.

The SBA Express Line of Credit provides a guarantee of 50% on loans up to $500,000, with a maximum term of 10 years.

The key advantage of the SBA Express Line of Credit is its accessibility—with a simplified application process and faster approval times, businesses can have access to the funds they need when they need them.

| Type | Term | Fixed or Revolving |

| Seasonal CAPLine | 10 years | Either |

| Contract CAPLine | 10 years | Either |

| Builders CAPLine | 5 years | Either |

| Working CAPLine | 10 years | Revolving |

| SBA Express Line of Credit | 10 years | Revolving |

SBA 7(a) Working Capital Pilot program

The SBA’s 7(a) Working Capital Pilot program was designed for modern small businesses—offering monitored lines of credit within the 7(a) program.

There are a number of more evolved features that the WCP program adds on top of the existing 7(a) line, including:

- A different fee structure: The fee structure for WCP is modeled after the SBA’s 7(a) Export Working Capital Program (EWCP).

- Support for transaction-based lending and asset-based lending.

- One-on-one counseling with SBA experts.

- The ability to provide working capital for domestic and international orders under a single loan.

To be eligible for the SBA WCP, you’re required to have been in business for at least one year. The maximum loan size is $5,000,000, with maturity up to 60 months. Interest rates for WCP loans are currently the same as the existing 7(a) rates (see below).

As of August 2024, all existing lenders approved to process 7(a) loans were able to begin providing Working Capital Pilot loans as well.

Interest Rates

The interest rates for an SBA line of credit vary but are typically lower than traditional bank loans. The rates are determined by the lender and depend on factors such as the borrower’s credit score, financial history, and the type of line of credit chosen.The interest rate for an SBA line of credit is usually expressed as Prime +.

The “Prime” refers to the current prime rate, which is a benchmark interest rate used by lenders. The “+” indicates a percentage that is added on top of the prime rate. This additional percentage varies depending on the amount of credit line and the lender’s assessment of the borrower’s creditworthiness.

| Line Size | Maximum Variable Rate |

| Up to $50,000 | Prime + 6.5% |

| $50,000 to $250,000 | Prime + 6.0% |

| $250,000 to $350,000 | Prime + 4.5% |

| Greater than $350,000 | Prime + 3.0% |

| Line Size | Maximum Fixed Rate |

| $25,000 or less | Prime +8% |

| $25,000 - $50,000 | Prime +7% |

| $50,000 - $250,000 | Prime +6% |

| Greater than $250,000 | Prime +5% |

Terms

The terms for SBA CAPLines also vary, with a maximum repayment period of up to 10 years.

However, there’s an exception for the builder’s line of credit. This specific CAPLine has a maximum repayment period of up to five years, or the time it takes to complete the construction or renovation project, whichever is less. This exception is designed to match the repayment period with the completion of the project, ensuring that businesses are not overburdened with repayments post-project completion.

SBA line of credit requirements

To qualify for an SBA line of credit, businesses must meet certain eligibility criteria, such as:

- Being a small business located in the United States

- Having good personal and business credit scores

- Being able to demonstrate the ability to repay the loan

While the general eligibility criteria apply to all SBA CAPLines, there are some specific qualifications depending on the type of CAPLine:

- Seasonal CAPLine – To qualify, businesses should demonstrate a definite pattern of seasonal activity, with an operating cycle of not more than 12 months. The business should also have been in operation for at least one year.

- Contract CAPLine – To be eligible, businesses must have specific contracts or orders that the funds will be used for. The repayment comes from the contract’s proceeds.

- Builders CAPLine – This CAPLine requires businesses to be involved in building or renovating commercial or residential buildings. The repayment comes from the conversion of construction loans into long-term financing or the sale of the residential or commercial property.

- Working CAPLine – Businesses must have inventory or accounts receivable.

For all CAPLines, you’ll need to provide collateral that can be liquidated by the lender if the loan is not repaid. The collateral requirements may differ based on the specific CAPLine, the amount borrowed, and the lender’s policies. Remember that every lender may have slightly different criteria for qualifying businesses, so you should always speak to your lender to understand the specific requirements.

How to apply for an SBA line of credit.

Applying for an SBA line of credit is similar to applying for any other loan. The first step is to find a lender that offers SBA CAPLines and meet their eligibility criteria.

Once you have found a suitable lender, you will need to gather the necessary documents, such as financial statements, tax returns, and business plans. You may also need to provide collateral for the line of credit.

After submitting your application and supporting documents, the lender will review your application and make a decision. If approved, you can start using your line of credit to support your business’ ongoing needs.

Conclusion

In conclusion, an SBA line of credit can be a valuable tool for small businesses looking for flexible and affordable financing options. With various types of CAPLines available and competitive interest rates, it is worth exploring as a potential funding source for your business. Learn more about SBA loans.

SBA loans are managed by banks as well as various online and nonprofit lenders. The Small Business Administration (SBA), which oversees this program, provides annual reports detailing the number of loans approved by each lender. Below, we highlight the SBA lenders that issued the highest number of SBA loans in 2023, categorized by program.

Best SBA 7(a) lenders for 2025.

The SBA 7(a) loan program remains the most sought-after option, offering flexible terms and various uses like working capital, equipment purchases, and real estate. Here are the top SBA 7(a) lenders (excluding Express and Community Advantage) by loan approval count, along with key details:

| *Lender | Funding Amount | Term Length | Minimum Credit Score | Time to Funding |

| BayFirst National Bank | Up to $5M | Up to 25 years | 675 | 2 weeks |

| Newtek Small Business Finance | Up to $5M | Up to 25 years | Not disclosed | Not disclosed |

| Live Oak Banking Company | Up to $5M | Up to 25 years | Not disclosed | Not disclosed |

| Cadence Bank | Up to $350K | Up to 10 years | 650 | As soon as 2 weeks |

Best for speed to funds.

BayFirst National Bank

BayFirst offers standard SBA 7(a) loans. They are an SBA-approved lender.

Funding amount: Up to $5 million- General

Term length: Up to 25 years- General

Minimum credit score: 675 - General

Time to funding: 2 weeks - General

Best for a comprehensive business solution.

Newtek Small Business Finance

Newtek provides comprehensive solutions for businesses from SBA loans to business insurance and payroll processing. They are an SBA-approved lender.

Funding amount: Up to $5 million.

Term length: Up to 25 years.

Minimum credit score: Not disclosed

Time to funding: Not disclosed

Best for large loan amounts.

Live Oak Bank

Live Oak Bank is an online financial institution that specializes in providing a substantial volume of larger SBA loans, with an average loan size of $1.7 million in 2023. As an approved SBA lender, they are well-positioned to support businesses seeking funding.

Funding amount: Up to $5 million.

Term length: Up to 25 years.

Minimum credit score: Not disclosed

Time to funding: Not disclosed

Best non-bank lender.

Cadence Bank

Cadence Bank provides a variety of SBA loan products backed by excellent customer service, and they are an SBA-approved lender.

Funding amount: Up to $350K

Term length: Up to 10 years.

Minimum credit score: 650.

Time to funding: As soon as two weeks

Best Community Advantage lenders.

A Community Advantage loan is a type of SBA 7(a) loan specifically designed to assist underserved markets by financing small businesses that may not qualify for traditional bank loans.

Below, we detail three noteworthy lenders who funded the most Community Advantage loans in 2023:

| *Organization | Funding Amount | Term Length | Requirements | Works with Startups? |

| CDC Small Business Finance Corporation | $10K - $350K | 6 - 10 years | No minimum credit score, sufficient cash flow, business projections for startups | Yes, with 10% downpayment and relevant experience |

| LiftFund | Up to $350K | 7 - 10 years | Sufficient cash flow to meet payments | Yes, with 20% owner injection |

| Wisconsin Women's Business Initiative Corp. | Up to $350K | Up to six years | Business plan with three years of financial projections | Yes, with extensive industry experience |

Best for businesses in major cities

CDC Small Business Finance Corporation

Small Business Finance Corporation provides loans to startups and small businesses across several major metropolitan areas. They serve a variety of industries, with dedicated specialists focusing on home healthcare and childcare sectors. Additionally, they offer complimentary business counseling to support their clients.

Funding amount: $10K-$350K

Term length: 6-10 years

Locations: Arizona; Atlanta, Georgia; California; Dallas-Fort Worth, Texas; Detroit, Michigan; Miami, Florida; Nevada, Washington, D.C. Metro Area

Requirements: No minimum credit score, sufficient cash flow to meet payments, business projections for early-stage/startups

Works with startups? Yes, with a 10% downpayment and management or industry experience

Best for businesses in Southern states

LiftFund

LiftFund provides access to capital for small businesses and startups throughout the Southern states. LiftFund also partners with other organizations to offer specialized loan programs to veterans and businesses in certain cities.

Funding amount: Up to $350K

Term length: Terms usually range from 7-10 years.

Locations: Alabama, Arkansas, Florida, Georgia, Kentucky, Louisiana, Missouri, Mississippi, New York, New Mexico, Oklahoma, South Carolina, Tennessee, and Texas.

Requirements: Cash flow sufficient to meet payments

Works with startups? Yes with 20% owner injection.

Best for businesses in Wisconsin

Wisconsin Women's Business Initiative Corporation

This nonprofit organization specializes in providing financial and educational resources to entrepreneurs in Wisconsin. In addition to loans, the nonprofit offers one-on-one business coaching and operates as a Veterans Business Outreach Center.

Funding amount: Up to $350K

Term length: Up to six years

Locations: Wisconsin

Requirements: Business plan with three years of financial projections

Works with startups: Yes- if the owner has extensive industry experience.

Top SBA Express Loan lenders.

A subset of the SBA 7(a) program, SBA Express loans are designed to provide rapid access to financing for small businesses, with approval times significantly shorter than traditional SBA loans. Below are the top three SBA Express loan lenders of 2024 based on number of SBA Express loans approved in 2023:

The Huntington National Bank

Huntington National Bank is one of the most experienced SBA lenders having approved the most SBA Express loans in 2023. Current customers can apply online for a loan of up to $350,000. The bank also runs the Lift Local Business Program which supports minority, woman, and veteran-owned small businesses through business planning support, free financial courses, and loans with reduced fees and lower credit requirements. They are an SBA-approved lender.

TD Bank

TD Bank provides SBA Express Loans of up to $350,000 and features an online application for loans up to $250,000. Beyond their loan program, the bank also manages an equity fund specifically designed for SSBICs and CDFIs, aimed at offering small business loans to minority-owned and women-owned enterprises. As an SBA-approved lender, TD Bank is committed to supporting diverse business initiatives.

U.S. Bank

U.S. Bank also offers Express loans up to $350,000 with an online application available for amounts up to $250,000. The bank also offers a Business Diversity Lending program for minority, women, and veteran-owned businesses for loan products outside the SBA program. They are an SBA-approved lender.

Top SBA 504 Loan lenders.

SBA 504 loans are designed to provide financing for major fixed assets, such as real estate and equipment. SBA 504 loans follow a 50-40-10 model where 50% of the total loan amount comes from a bank loan, a Certified Development Company (CDC) provides 40% in the form of a debenture or bond, and the remaining 10% is the down payment from the small business owner.

A Certified Development Company (CDC) is a nonprofit organization that facilitates the SBA 504 loan program. Each CDC operates within a designated area and is tasked with working closely with small businesses and lenders to approve and process 504 loans. We list the CDCs with the greatest amount of CDC loans approved in 2023 below. You can search for a CDC that operates in your state on the SBA website.

| *SBA 504 Lenders | Approval Count | Locations |

| Mortgage Capital Development Corporation (TMC Financing) | 461 | Arizona, California, Nevada, and Oregon |

| Florida Business Development Corporation | 416 | Florida, Alabama, Georgia |

| Florida First Capital Finance Corporation, Inc. | 283 | Florida, Alabama, Georgia |

| California Statewide Certified Development Corporation | 227 | California, Arizona, Nevada |

| Empire State Certified Development Corporation (Pursuit Lending) | 226 | New York, Pennsylvania, New Jersey, Connecticut |

| Business Finance Capital | 217 | California |

How to find an SBA microlender.

An SBA microloan is a loan of up to $50,000 administered by a nonprofit lender. Similar to a CDC, these lenders operate locally. To locate an SBA microlender, start by visiting the SBA’s official website where a list of approved lenders and resource partners is available. You can also utilize the SBA’s local district offices as they often have details on microlenders in your area.

How to choose an SBA lender.

Selecting the right SBA lender involves considering several factors. Here's how to make an informed decision:

Evaluate Your Needs

Determine the type of SBA loan that best suits your business needs. Whether it's a 7(a) loan, a 504 loan, or a microloan, understanding your requirements will help narrow down your choices.

Compare Lenders

Research and compare lenders based on their loan offerings, interest rates, terms, and customer reviews. Look for lenders with a strong track record of supporting businesses similar to yours.

Seek Personalized Service

Choose a lender that offers personalized support and guidance throughout the loan process. A dedicated loan officer can help you navigate the complexities of SBA lending and increase your chances of approval.

How to Get an SBA Loan through Lendio.

Lendio is an online marketplace that streamlines obtaining SBA loans for small businesses. By connecting users with a network of lenders, it allows business owners to compare financing options through a single application. Lendio's loan experts help gather necessary documents, making the process easier. Loans are typically funded in under 30 days, depending on the lender and documentation completeness.

Methodology

Top lenders were selected based on the number of SBA loans approved in 2023 as reported by the Small Business Administration. Lenders were also evaluated based on their lending criteria, application process and whether they are an SBA-Preferred lender.

*The information contained in this page is Lendio’s opinion based on Lendio’s research, methodology, evaluation, and other factors. The information provided is accurate at the time of the initial publishing of the page (August X, 2024). While Lendio strives to maintain this information to ensure that it is up to date, this information may be different than what you see in other contexts, including when visiting the financial information, a different service provider, or a specific product’s site. All information provided in this page is presented to you without warranty. When evaluating offers, please review the financial institution’s terms and conditions, relevant policies, contractual agreements and other applicable information. Please note that the ranges provided here are not pre-qualified offers and may be greater or less than the ranges provided based on information contained in your business financing application. Lendio may receive compensation from the financial institutions evaluated on this page in the event that you receive business financing through that financial institution.

Launching a startup business is exciting, but it can also be stressful if you need external money to keep the momentum going. While the U.S. Small Business Administration offers several small business loans for established companies, there are also some loan options available to new ventures. This guide will cover SBA funding for startups, as well as how to apply. We’ll also cover the SBA loan requirements for startups, and alternatives for capital if these loan types won’t work for your business.

SBA loans for new startups.

While there’s no specific SBA startup loan, there are two financing options available to newer businesses: the SBA microloan and the SBA Community Advantage Program. Each one has its own loan terms and eligibility requirements, and can help serve brand new businesses that are just starting out.

SBA Microloan

An SBA microloan for startups allows businesses to borrow up to $50,000. The average loan size, however, is much smaller at $13,000. The maximum loan term is seven years. These smaller loans are geared towards early-stage businesses, so have less strict eligibility requirements than other SBA loans and traditional loan options.

Ideal for: Managing a new business and providing working capital.

Can be used for: Working capital, inventory, supplies, equipment, furniture or fixtures.

Cannot be used for: Paying existing debt, settling lawsuits, trade disputes, fines, penalties, or purchasing real estate.

Eligible businesses: For-profit small business or nonprofit child care center.

Application Process: Even when choosing to use an SBA loan to start a business, you’ll still need to apply directly through a lender. Lenders typically require collateral and a personal guarantee in order to get approved for a microloan. Read our guide to learn more about applying for an SBA microloan.

SBA Community Advantage Program

Historically underserved communities may be eligible for the Community Advantage Program for a SBA loan for their startup. It’s specifically designed to help new entrepreneurs in underserved markets obtain working capital. You can borrow up to $350,000 over the course of 10 years through Community Advantage Small Business Lending Companies (CA SBLCs) Originally begun as the Community Advantage Pilot program that sunsetted September 30, 2024, the Community Advantage Program is now a permanent part of the SBA 7(a) loan program, through new licenses issued to previous lenders in the program who can now issue 7(a) loans to traditionally underserved businesses.

Ideal for: New businesses located in low-to-moderate income communities that are less than two years old.

Can be used for: Purchasing commercial real estate that the owner occupies, leasehold improvements or renovations, purchase of inventory, equipment, furniture, fixtures, working capital, business acquisition, or debt refinance for any of the above.

Cannot be used for: Illegal businesses or businesses that do not meet the eligibility requirements, delinquent taxes, investment real estate, or personal use.

Eligibility requirements: Eligible businesses must be part of an underserved market. There are several ways to qualify for this designation, such as:

- Businesses located in Low-to-Moderate Income Communities, Empowerment Zones and Enterprise Communities, Historically Underutilized Business Zones, Promise Zones, Opportunity Zones or Rural Areas

- New businesses that have been operating for less than two years

- Veteran-owned businesses that are 51 percent or more owned and controlled by one or more veterans

- Businesses where more that 50% of the full-time workforce is low-income or resides in LMI census tracts.

Interested in exploring loan options, including SBA loan products like microloans and 7(a) loans, for your new business? Compare loan offers from multiple lenders with Lendio. Applying is free, and won’t impact your credit. Apply now!

SBA loans for established startups.

Once your startup has reached two years old, the options for SBA loans expand. The following options have their own eligibility requirements.

SBA 7(a) loan

SBA 7(a) loan funds can be used for a number of purposes. The maximum loan amount is $5 million, and any loan amount over $25,000 requires collateral. Loan repayment terms can vary depending on what the loan is used for, but the repayment period is usually 10 years.

Ideal for: Businesses who have reached the growth stage.

Can be used for: Working capital, equipment, supplies, real estate, debt refinancing and ownership changes.

Cannot be used for: illegal or unqualified business as defined by the SBA, delinquent taxes, investment real estate or personal use.

Eligibility Requirements: Each SBA lender's criteria may vary for an SBA loan. For example, some may require a higher credit score than other lenders. However, at minimum you must have owner equity and engage in for-profit operation in the U.S. or its territories. Read our guide for more information about SBA 7(a) loan requirements.

SBA 504 loan

The SBA 504 loan is designed to help small businesses make major investments. Funds can be used for long-term assets such as real estate (including updates), land, equipment, machinery, or improvements to land, parking lots, and utilities. You can’t use the funds for working capital or inventory. If approved, you could borrow up to $5 million over a period of 10 or 20 years.

Best For: Purchasing or upgrading major fixed assets for your business.

Can be used for: Real estate, land, equipment, machinery, or improvements to utilities, parking lots, and the above.

Cannot be used for: Working capital or Inventory purchase.

Eligibility Requirements: Like 7(a) lenders, 504 lenders may set more stringent criteria to access an SBA 504 loan. In most cases, you will need strong credit history, finances, and multiple years in business to qualify. Read our guide for more details on SBA 504 loan eligibility requirements!

Explore Lendio to find the right SBA loan option for your startup, so you can start making the business moves you need to succeed.

How to get an SBA loan for startups.

In order to pursue an SBA loan for your startup and increase your chances of receiving a loan, you’ll want to do some preparation first. Here are the steps to take to prepare and submit an application for an SBA loan.

1. Calculate your startup costs.

Knowing how much you need to borrow is your first step. Pull together the costs of starting your business, including one-time costs for permits, licenses, equipment, furniture and fixtures. You’ll also need to calculate recurring expenses, such as payroll, rent, and inventory for at least your first year in business.

Calculating your business startup costs will give you an idea of how much money you will need to get your business off the ground.

2. Write your business plan.

Many lenders will want to see your business plan, including research on target market, pricing structure, marketing costs, challenges, and your industry competition. Your startup costs calculation also belongs in your business plan, as well as projected income.

Without multiple years of profits to lean on in your application, you’ll need to use these tools to show that your business will be a success, so spend some time writing a business plan to help you secure funding.

3. Review SBA loan qualifications.

All your hard work will be for nothing if you start the loan application process only to realize you won’t qualify. First, review the standard SBA loan requirements. You’ll need to:

- Be a for-profit business operating in the U.S.

- Meet the Small Business Administration’s definition of a small business.

- Be able to show your ability to repay the loan.

- Have tried to find alternative forms of funding before trying to get an SBA loan.

Because SBA loans are issued through lenders, you’ll also need to review common requirements for underwriting loans to improve your chances. Your personal credit score and business credit score should be improved as much as possible before pursuing a loan, and you’ll need to gather cash flow, sales projections and any available collateral you may have for the loan.

4. Choose a loan and lender for your startup.

After reading some of the available options above, you probably have an idea of which SBA startup loan option will meet your needs. From there, you’ll need to find the best SBA lender for your startup..

The SBA provides a Lender Match tool to help you find a bank, credit union, or community-based lender that participates in your chosen loan program. You can always double check with a financial institution you’ve previously had a relationship with to see if they participate in the loan program you’re searching for.

You can also apply through Lendio to be matched with funding options that best suit your business needs. It takes 15 minutes to complete the application, and you’ll be put in front of 75+ lenders, including those who offer SBA loan options.

5. Prepare your loan application.

After you’ve chosen a lender, you’ll be ready to start your SBA loan application. You’ll need a lot of documentation to support your application, but there may be some variations on specific documents you need based on your loan program and lender.

Prepare all your business and personal documentation, including tax returns, financial statements, certificates and licenses, business history, business plan, contracts and more.

You’ll also need to complete some SBA forms, such as SBA Form 1919 Borrower Information Form, SBA Form 912, Statement of Personal History, and SBA Form 413, Personal Financial Statement.

Thankfully, your lender will be able to help you through the application process and make sure you have all the required documentation.

Online business loans

Many online lenders have flexible qualifications and multiple loan products for startups. If you’re looking for funding fast, exploring these options can be a great way to get funding, sometimes in as little as 24 hours. Curious what kind of loan options might be best for your business? Visit the Lendio Industry funding resource center to select your industry and see loan type recommendations for your business.

Small business grants

Grants for small businesses are a way to avoid accumulating debt by offering capital that you don’t have to repay. The application process may be time-consuming, but if you can secure funds this way it may be worth it for your business.

Business credit cards

If you need help with everyday expenses while launching your business, business credit cards for startups are a great way to build your business credit score with responsible management and earn rewards that benefit your business.

Get funding for your startup.

Now that you know the SBA loan options for your startup, as well as how to apply and some alternatives to consider, it's time to figure out which loan option you’re going to pursue. Let Lendio take some of the guesswork out of funding your startup with the Lending Marketplace.

Simply fill out an application, and receive offers from our network of 75+ lenders to compare your funding options. There’s no impact to your credit score, and once you accept an offer, you could receive the funds you need for your startup in as little as 24 hours.

If you're a small business owner looking for financing options, you may have come across the term “SBA loan.” But what exactly is an SBA loan?

In this blog post, we’ll dive into the details of what SBA loans are, the pros and cons, and how to apply, while helping you understand if getting an SBA loan is the right option for your business.

SBA Loans

What is an SBA loan?

Small Business Administration (SBA) loans are government-backed loans designed to help small businesses access the funding they need to start, grow, or expand their business.

SBA loans are partially guaranteed by the SBA, making them less risky for lenders, and therefore, more accessible to small businesses. These loans are not directly provided by the SBA, but rather through participating lenders such as banks and credit unions.

What does SBA stand for?

SBA stands for the Small Business Administration, a U.S. Government agency that supports small businesses by giving them access to capital, counseling, and other community resources.

How do SBA loans work?

Unlike traditional loans where the lender assumes all the risk, an SBA loan is backed by the government.

This means that if a borrower defaults on their loan, the SBA will partially reimburse the lender for their losses.

This guarantee reduces the risk for lenders and encourages them to provide loans to small businesses, even if they have lower credit scores or less established financial histories.

What can you use an SBA loan for?

Types of SBA loans

There are several types of SBA loans available, each designed for different purposes and needs of small businesses. Here are the most common types:

SBA 7(a) loans

SBA 7(a) loans are the most common and flexible type of SBA loan. They can be used for a wide range of purposes, including working capital, equipment purchases, real estate, and refinancing existing debt.

Visit the SBA website to read more about SBA 7(a) loans.

| SBA 7(a) loan details | |

| Common use cases |

|

| Maximum loan amount | $5 million |

| Terms | Up to 10 years for working capital or equipment Up to 25 years for real estate |

| Maximum guarantee | 85% |

SBA 504 loans

SBA 504 loans are specifically designed to help small businesses purchase major fixed assets such as machinery or real estate. These loans are provided through Certified Development Companies (CDCs), private, nonprofit corporations set up to contribute to the economic development of their communities.

The benefit of an SBA 504 loan is that it offers long-term, fixed-rate financing, making it a more affordable option for businesses looking to make major investments.

Read more about SBA 504 loans here.

| SBA 504 loan details | |

| Common use cases |

|

| Maximum loan amount | $5.5 million |

| Terms | 10, 20, or 25 years |

| Notable details |

|

SBA microloans

The SBA microloan program provides smaller loan amounts for businesses that need just a small injection of funds. These loans are designed to help startups, microbusinesses, or non-profit child care centers with their various needs, whether it's working capital, inventory, supplies, or equipment. The maximum loan amount under the microloan program is $50,000, but the typical loan size is much smaller, often averaging around $13,000.

The exact terms of the loan depend on how much you borrow, what you'll use the loan for, and your own financial circumstances. This type of SBA loan is unique in that it is provided through non-profit community lenders who also offer business training and technical assistance, making it a comprehensive package for first-time entrepreneurs and small business owners.

Learn more about microloans and see a list of microlenders here.

| SBA 504 loan details | |

| Common use cases |

|

| Maximum loan amount | $50,000 |

| Terms | Up to 6 years |

SBA disaster loans

SBA disaster loans are designed to provide financial support to businesses, homeowners, and renters affected by declared disasters. Unlike other types of SBA loans, disaster loans are directly funded by the SBA, not through lenders. They offer low-interest, long-term loans for physical and economic damage caused by a declared disaster.

Businesses of all sizes, homeowners, and renters can apply for a physical disaster loan to repair or replace damaged property, while businesses and non-profit organizations can apply for an economic injury disaster loan to help meet working capital needs caused by the disaster. The SBA will determine the loan amount and term based on each borrower's financial condition.

Read more about SBA disaster loans here.

| SBA disaster loan details | |

| Maximum loan amount | $2 million |

| Terms | Up to 30 years |

SBA loans vs. conventional loans

Since SBA loans are government-backed, there are a few specific differences to call out relative to conventional loans.

- You can qualify with a much younger, riskier business profile. Conventional loans typically require at least 6 months of time in business, whereas SBA loans work with eligible startups. Since lenders shoulder less risk from the actual loan, they’re willing to take on more risk from the lender.

- SBA loan amounts are capped at $5.5 million. Conventional loans don’t have defined limits, and can vary more greatly.

- SBA loans have a longer approval time. Since you have to meet requirements for both the lender and the government, approval can take more than 30 days. For conventional loans, approval can happen in just a few days.

- SBA loans have capped interest rates. While SBA loans may not offer the lowest possible interest rates, they keep the ceiling of interest lower than conventional loans. See current SBA loan rates here.

Eligibility requirements for an SBA loan

Is it hard to get approved for an SBA loan?

Given the combination of personal and business requirements, it’s moderately difficult to get approved for an SBA loan—not easy, but not overly difficult. A large part of the approval process revolves around your personal history and available financial resources.

To qualify for an SBA loan, you must meet the following requirements:

- Your business must operate in the US and be legally registered

- Your business must fall under the SBA's definition of a small business

- You must have invested your own time and money into your business before seeking outside funding

- You need to have a good credit score (typically above 680) and a solid financial history

- Collateral may be required, depending on the type of loan you apply for

Pros and cons of SBA loans

| The pros | The cons |

| Capped interest, assuring fair rates for new businesses | Longer application and approval processes due to the involvement of the government in guaranteeing the loan |

| Longer repayment terms, making it easier to manage cash flow | Collateral may be required without a strong credit score |

| Ranging loan amounts, offering flexibility for different business sizes | Additional costs, such as packaging fees or maintenance fees, may be involved |

| Broad business eligibility |

Application process for an SBA loan

Applying for an SBA loan requires you to know a lot about your business, and requires a combination of personal and business-specific paperwork to submit successfully.

1. Understanding the numbers behind your business:

To qualify for an SBA loan, it’s important to note that your business should have been operational for a reasonable period of time. Many lenders prefer businesses to have been in operation for at least two years.

This is to ensure that your business has a proven track record and demonstrates stability and the ability to generate consistent revenue.

In terms of credit score, a personal score of at least 680 is generally preferred by most lenders. This high credit score showcases your reliability and ability to repay the loan.

Otherwise, you need to know your business down to the dates and dollars its comprised of. Are you able to prove profit and loss and cash flow for your business? Can you show both historical numbers and future projections to prove you’re generating revenue?

You should be prepared to show all money in and out, taxes, and any existing debt.

2. Making sure you have the proof:

Do you have all the documentation needed to prove the dates and dollars mentioned above?

This includes fundamental business and financial documents, such as your business plan, personal and business income tax returns, personal and business bank statements, and a balance sheet. You’ll also need to provide financial projections, ownership and affiliations, business license, loan application history, and business lease.

3. Finding an SBA-approved lender in your area:

Your next step is to find an SBA-approved lender in your area. This could be a traditional bank, a Community Development Company (CDC), or a microlender, depending on your needs.

The SBA has a free online Lender Match tool that can connect you with participating SBA-approved lenders within 48 hours. They also provide lists of CDCs and microlenders.

When choosing a lender, consider factors such as their SBA loan expertise, the types of businesses they typically work with, and their understanding of your industry. Building a relationship with your lender can be beneficial, as they could provide valuable guidance throughout the loan application process.

4. Submitting your application.

After you’ve gathered all necessary documentation and found an SBA-approved lender, you’ll need to package your paperwork together alongside SBA forms 1919 and 413.

Your lender will guide you through the application process and help you submit all required documents.

How long does it take to get approved for an SBA loan?

The timeline for approval can vary depending on the type of loan you apply for and the lender's processing times.

Typically, the application process can take anywhere from one to three months (30 to 90 days), while the funds can take an additional one to two weeks to be disbursed.

What happens to an SBA loan if your business closes?

Sometimes it happens—your business closes. In that case, what happens to your SBA loan?

Like any other loan, you need to continue making payments, or else you’ll go into default, where lenders can begin to seize collateral.

The SBA does compromise in some cases. Via their Offer in Compromise (Form 1150), businesses that default on their loan are able to apply for a settlement of a lower amount if paid in full more immediately. In this case, the loan is considered paid off.

Generally, the most important thing to keep in mind—you’re responsible for the money owed to the lender no matter what.

SBA loans can be an excellent financing option for small businesses looking to grow or sustain their operations. With an understanding of your requirements, you can begin to search for an SBA lender today.

As a small business owner, financing backed by the U.S. Small Business Administration (SBA) represents some of the most affordable types of business loans available. SBA loans are a popular option for both startups and established businesses alike. These loans tend to feature low interest rates, higher loan amounts, and generous repayment terms compared to other business loan options.

At the same time, understanding how to apply for an SBA loan and qualify for this type of financing can be complicated. The SBA loan application process can be tedious, and if you don’t complete it properly, you could hurt your chances of getting a loan approval.

That’s why Lendio has put together a complete guide to applying for an SBA loan, including types, requirements, the application process, and how to improve your chances of approval.

Step 1: Decide which type of SBA loan you need.

There are several different types of SBA loans available to small businesses. With SBA loans, your business may be able to borrow up to $5 million and repay those loans over a period of 10 to 30 years. (Repayment terms can vary.)

You can find SBA loans to help you finance many different aspects of your business needs. Whether you need startup funding, working capital, equipment financing, inventory financing, or funding for some other type of business need, you may be able to find an SBA loan to support your goals.

First, Ask yourself a few key questions about your business needs to find the right SBA loan program for your needs, like:

- How much funding do I need?

- What will I use the funding for?

- What is the minimum repayment term I need to work with?

Once you figure out the type of SBA loan you want, you can determine if your business is eligible for the loan program.

Step 2: Check eligibility requirements

The specific eligibility requirements that your business needs to meet in order to qualify for an SBA loan will vary based on a few factors. First, each SBA loan program has unique requirements you must meet to qualify. In addition, you may need to satisfy additional loan requirements that your SBA-approved lender requires from small business borrowers.

The minimum requirements for most SBA loans are as follows.

- Be an operating business

- Operate for profit

- Be located in the U.S. or in U.S. territories

- Can meet SBA “small business” size requirements

- Not be a type of ineligible business

- Be creditworthy and demonstrate reasonable ability to repay the loan

- Collateral to secure a large percentage of the loan

- Unable to access business financing through non-government means (not including personal funds)

If you meet these requirements, then the next step is confirming that you qualify with an SBA lender, and this is where it can get complicated. Let’s go over some major eligibility requirements with most SBA-approved intermediary lenders as lender standards vary.

Creditworthiness Requirements

SBA 7(a) loans and SBA 504 loans are issued by traditional lenders, so they will have more stringent credit criteria than other loans, like microloans.

Most lenders for these loans will want to see a FICO® credit score of 650 or above.

On the other hand, SBA microloans have less strict credit criteria, and you may be able to qualify with limited credit history.

Time in Business Requirements

Like credit criteria, SBA 7(a) loans and SBA 504 loans will require more time in business and proof of revenue than microloans.

Most lenders will want to see at least two years in business for 7(a) and 504 loan applicants. In contrast, lenders may not require as much time in business for the microloan program, with some lenders only requiring six months in business.

If you meet these eligibility requirements, the next step is to gather all the documentation you will need for the application process.

Step 3: Prepare documentation for SBA loan application

Before you apply for an SBA loan, it’s important to gather the documentation your lender will request on your application. The time it takes to move through the SBA process from application to funding will vary.

While it might take 30 to 90 days with your local bank, Lendio, on average, can close an SBA 7(a) small loan in less than 30 days. Having your documents prepared ahead of time may help improve your chances of approval and could help you move forward through the SBA loan process at a faster pace.

Below is a list of the documents you should prepare for your SBA loan application:

- Six months of business bank statements (connect account or manually upload images)

- Copy of your driver’s license or state ID

- Voided check from your business account

- Month-to-date transactions

- Two years of business and personal tax returns (for all business principals with 20% or more ownership)

- Debt schedule

- Year-to-date profit and loss statement

- Year-to-date balance sheet

- Cash flow projections

- List of collateral

- Business certificates or licenses

- Loan application history

- Business owner resume(s)

- Business plan

- Business lease, if applicable

Additional SBA loan application requirements.

In addition to the documents listed above, you should be prepared to include more information on your SBA loan application. Details you may need to provide include:

- The amount of money you want to borrow.

- The purpose of the loan and how you plan to use the proceeds if approved.

- Assets you need to purchase and the name of your business suppliers.

- When your business started.

- General information about your business (owners, affiliations, etc.).

- Your birthday and your Social Security number

- Details regarding other business debts and your creditors.

Anyone who owns 20% or more of the business will generally need to fill out an SBA loan application form, as the SBA requires that anyone with 20% or more ownership in the business provide an unlimited personal guarantee.

Owners with less than 20% ownership can provide full or limited guarantee. Owners will also need to complete a personal financial statement, called SBA Form 413. SBA uses the personal financial statement to assess risk and help determine an applicant’s ability to repay as promised.

Here's a list of SBA-specific forms to include in your application package:

- SBA Form 1919 - Borrower Information Form

- SBA Form 912 - Statement of Personal History

- SBA Form 413 - Personal Financial Statement

- SBA Form 148 - Unconditional Guarantee (or lender’s equivalent to this form.)

- SBA Form 148L - Limited Guarantee (or lender’s equivalent) for owners with less than 20% ownership

Step 4: Find an SBA-approved lender

You can use an SBA loan to support your small business in many different ways. Once you feel ready to begin your SBA loan application, you can start by choosing an SBA lender to guide you through the process.

Depending on the type of SBA loan program you are applying for, you might have a few different options for finding an intermediary lender. Since SBA 7(a) loans and SBA 504 loans lenders are more traditional financial institutions, you can try reaching out to a bank you have a previous relationship with.

The SBA also offers a few resources for finding active certified development companies (cdcs) and active microlenders on their website.

If you would like to connect with lenders directly, you can use the SBA’s lender match system. You’ll fill out a questionnaire about your business, and in two days, you’ll receive an email with possible lender matches.

Lendio offers a convenient SBA loan application process. Potential borrowers can complete an application and get a preapproval within 24 hours, and after providing the documentation listed above, can get funded with a 7(a) small loan in less than 30 days.

Step 5: Submit your SBA Loan Application Package

Once you’ve prepared your loan application package, it’s time to submit it to the lender. Don’t be surprised if they may follow up with questions, or request for additional documents. Every lender has different requirements, so work with your contact to provide everything they need to begin the initial underwriting process to review your application.

If your lender decides to move forward, you can expect a “loan proposal” or “letter of intent” to follow. This document will detail your request, loan terms, and deposits, fees and/ or closing details.

If you accept and sign the proposal, you’re not out of the woods yet. Your lender will begin a formal underwriting process, in which both the lender and the SBA review your application, documentation and credit history thoroughly.

If you are approved after this process, you will be notified and provided a letter of commitment. You must accept it in order to receive closing documents and start the closing process. Once everything is signed and the process is complete, your money will be disbursed.

What to do if your SBA Loan application is denied

Although it's not the outcome you want, only about one-third of SBA loan applicants were fully approved in 2023. A decline is not uncommon, so knowing your options if this happens will help you plan for your next steps.

If your application is denied, your lender will provide you with a letter explaining the reason you were denied, and may provide some options for you after that. You may be able to appeal the decision, for example, and your lender can provide insight.

Read our guide on common reasons why your SBA loan application may have been declined, and what to do next.

Alternatives to SBA Loans

If you aren’t able to find a workaround in the event that your SBA loan was declined, or if you aren’t confident you meet the eligibility requirements, here are some other alternatives to consider:

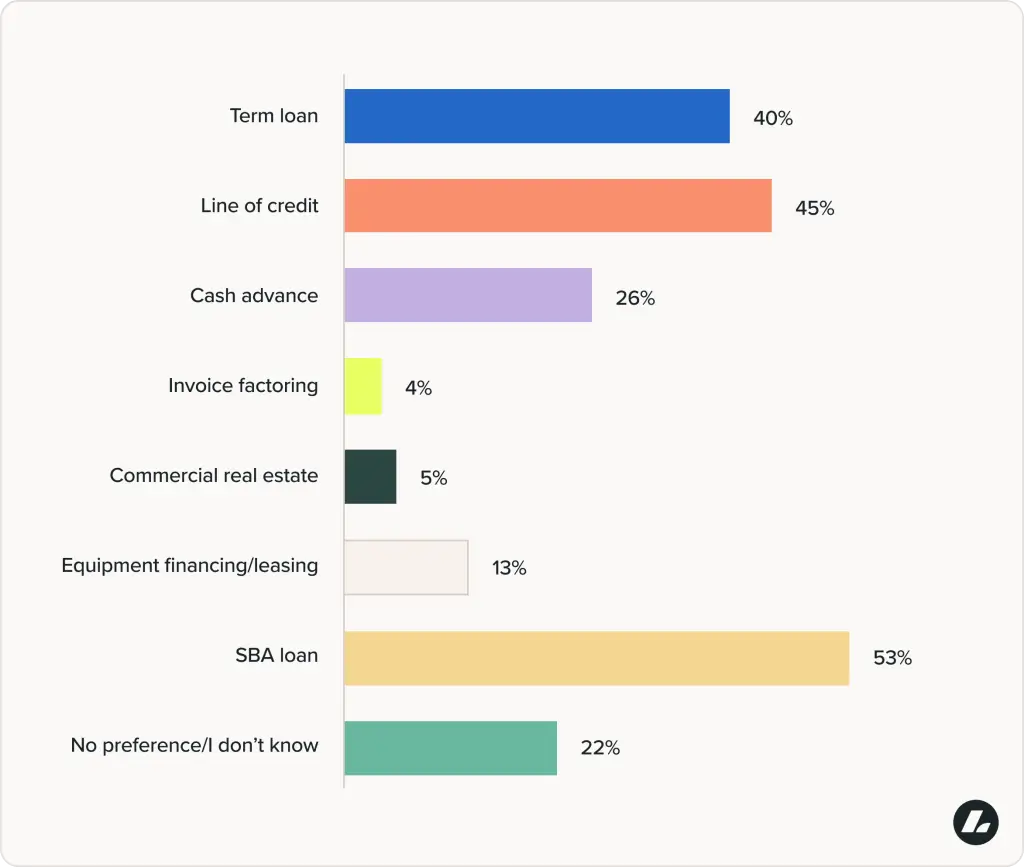

- Equipment financing- if new equipment upgrades, repair or replacement is what you need, consider exploring term loans or leases for equipment.

- Term business loans - If you don’t qualify for an SBA loan, you may still be able to obtain a business loan paid off with equal payments at a fixed rate through other lenders.

- Business lines of credit- Opening a line of credit enables you access to funds that you can borrow anytime up to your credit limit.

Business loans are crucial for helping small businesses thrive by providing the necessary capital to cover startup costs, invest in inventory, or upgrade equipment. For many small business owners, these loans are not just a means to an end; they are a lifeline that enables them to seize growth opportunities and navigate the challenges that come their way. Therefore, it is vital to understand the current lending landscape that small businesses are facing.

Key stats.

- 68% of small business owners say access to financing is the most important factor in the growth of their businesses.

- 67% of small business owners have no preference about which type of lender they get a loan from.

- 85% of small business owners said that speed to loan approval is important when selecting a lender.

- 77% of small business owners surveyed stated that they prefer to apply for a loan online or via a mobile app.

- 50% of small businesses say they don't know if the bank they use for checking has the right loan options for them.

- Only 24% of small business owners apply through the bank they already work with.

- The average small business loan is $38,000.

- 59% of SBA loans are approved.

High-level overview.

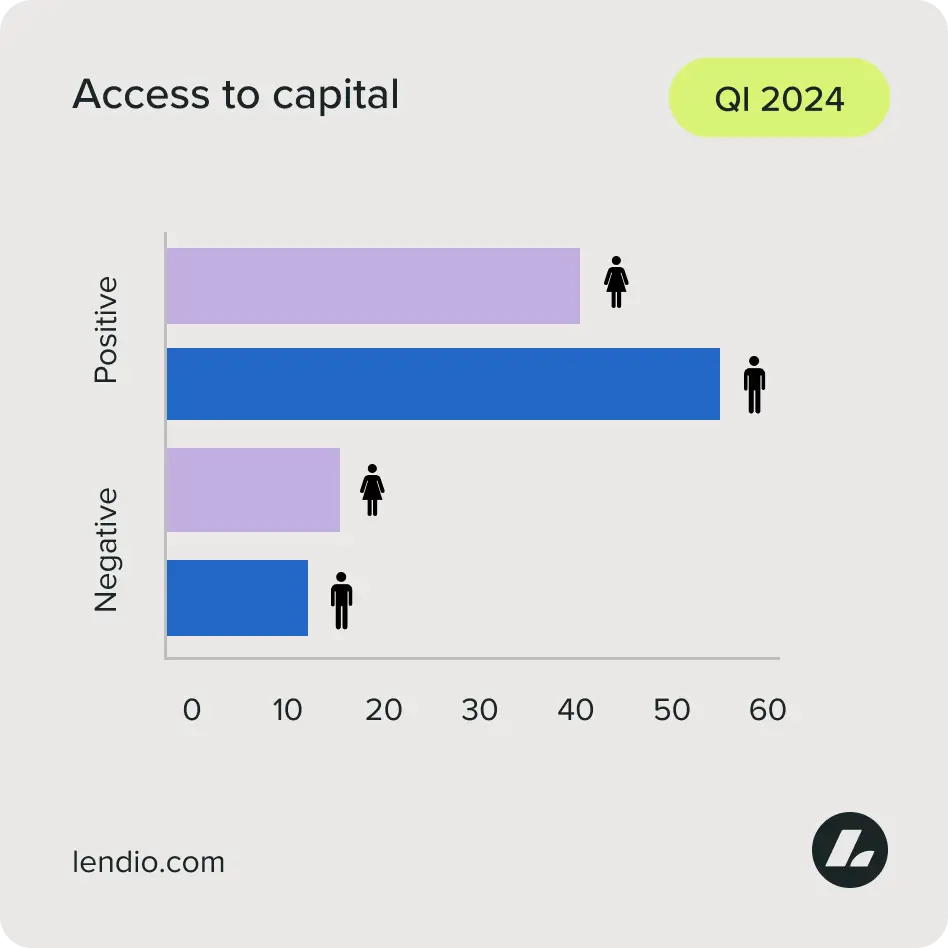

Lendio recently surveyed 1000+ small business owners to better understand how financing affects the success of their business, their experience in today's lending environment, and how they view the future of small business lending. Of those small business owners, 68% said that access to financing is the most important factor in the growth of their businesses. Additionally, 46% of those 1000+ small business owners said they would see anywhere from 30-100% revenue growth if they had access to financing their business needs.

Lendio found that 78% of the small businesses it interviewed have a positive outlook on their ability to access capital in the next year. Perceptions vary based on how well-qualified the small business is for a loan. Only 12% of the most qualified borrowers stated that the majority of small businesses don't have access to the capital they need while 21% of the least qualified borrowers said the same.

Lendio found that while small business owners generally have a positive outlook on their ability to access capital, they have a fairly neutral perception of the loan application process. When asked which type of lender they'd prefer 67% of small business owners said they have no preference.

The takeaway:

85%

of small business owners say speed to loan approval is important when selecting a lender.

While larger enterprises are willing to experience lengthy loan approval and funding processes, small business owners behave more like consumers--they prefer a quick and easy loan process.

- 85% of small business owners said that speed to loan approval is important when selecting a lender.

- 77% of small business owners surveyed stated that they prefer to apply for a loan online or via a mobile app.

Lendio also found a general lack of awareness of the small business loan process.

- 50% of small businesses say they don't know if the bank they use for checking has the right loan options for them.

- Only 24% of small business owners apply through the bank they already work with.

- Lendio found that 22% of small business owners either don’t know or don’t have a preference for their preferred type of business financing.

These findings point toward a need for more education about the lending landscape for small business owners.

Average business loan amount.

Understanding the average loan amounts small businesses receive is critical for entrepreneurs seeking to plan their financial strategies effectively. Businesses should be aware of not only the amounts they might qualify for but also how these figures align with their growth aspirations and operational needs.

- The average amount a small business receives through Lendio’s marketplace is $38,000.

- The average SBA loan amount in 2023 was $479,685.

- On average, small businesses are offered 50% of the loan amount they initially asked for.

SBA loan approval rates.

The Small Business Administration (SBA) plays a vital role in supporting small businesses by providing access to loans with favorable terms. In 2023, approximately 59% of SBA loans were approved (34% received full approval, 25% received partial approval), indicating that over half of small business owners successfully navigate the application process. This is particularly encouraging for entrepreneurs who might face challenges securing traditional financing, as SBA loans often come with lower interest rates and longer repayment terms.

Reasons for a business loan.

Lendio found that the majority of small businesses pursue loans for a variety of essential reasons, primarily to secure working capital (33%) to support daily operations and manage cash flow. Additionally, small businesses often seek financing for crucial investments like equipment purchases (19%), expansion efforts (15%), starting a business (14%), payroll (6%), real estate (4%), or for other purposes (9%). Each of these reasons highlights the integral role that loans play in facilitating growth and sustainability in the competitive business landscape.

Gender insights

Men and women generally had similar responses to Lendio's survey questions, but a few differences stood out.

Only 46% of women are positive or very positive that they can access the capital they need compared to 55.8% of men who said the same. 13% of women also rated their ability to access the capital they need as "very poor" compared to 9% of men.

Another key insight points to a need for education surrounding the business lending landscape, especially for women. 53.3% of women and 41.7% of men are unsure of their primary bank's loan options. More women business owners stated that they would like education on the business loan application process across the board except interest rates (this was equal). This includes lender types, loan agreements, and loan types.

Women-owned businesses received just 32.6% of approvals and 28.4% of the dollars offered in SBA 7(a) and 504 loans in the 2024 fiscal year. Across the lending landscape as a whole, women are less likely to receive the full amount of funds requested. In 2023, 45% of women-owned businesses were approved for the full amount of capital requested vs. 55% of men-owned businesses.

Additionally, 25% of women are denied a business loan compared to 19% of men.

Minority insights

When it comes to accessing business loans and receiving funding, entrepreneurs of color can face significant challenges.

- 84% of businesses started by a person of color relied on personal savings or funding from friends or family to fund their businesses.

- 28% of employer businesses started by a person of color have obtained a business loan compared to 48% of white-owned business startups.

- Nearly half of black business owners who apply for a loan are denied.

Conclusion

Understanding the lending landscape for small businesses is crucial for their growth and success. The statistics presented highlight the significant role that access to financing plays in empowering entrepreneurs across the United States. While optimism prevails among small business owners regarding their ability to secure capital, challenges persist, particularly for women, minority, and veteran entrepreneurs.

Even though the acronym UCC sounds like a college of some sort, it stands for the Uniform Commercial Code (UCC). And rather than hand out diplomas, the UCC was developed to regulate how commercial transactions operate.

OK—But what's a UCC filing?

UCC filings are how lenders establish their right to the assets you, the borrower, use to secure a loan. The filing serves as a lien, so that there's public record of your efforts to take out a loan.

UCC filings are made up of UCC-1 and UCC-3 filings, explained in more detail below.

What is a UCC-1 filing?

A UCC-1 is the official original UCC filing that gets made by a lender, referring to the UCC1 form that's needed in order to do so. It's effectively a public announcement lenders make that either a borrower has taken out a loan with them or is looking to take out a loan with them.

This filing defines the collateral the borrower puts up to secure financing, which prevents a borrower from using the same collateral for multiple loans (a move that would put the lenders at much higher risk).

You could think of it as the financial version of “going public” on social media with a new relationship. Once you change that relationship status, other people who might be interested can see you’re already committed to someone else. They allow lenders to see how you’ve treated other loans in the past.

What is a UCC-3 filing?

A UCC-3 filing is simply an amendment to the original UCC-1 filing.

This might be used to update the information of the borrower or lender, add or change collateral, terminate a filing, or reassign or terminate creditor interest.

What is the difference between a lien and a UCC filing?

Put simply, a UCC filing serves as a lien, whereas a lien may not always be a UCC filing.

Liens can span everything from personal property, to real estate, to tax liens, child support, and much more. UCC liens fall within this list as another subcategory.

Oftentimes, liens arise from legal issues, and can be created involuntarily—for instance, with a property lien. UCC liens are intentionally created by creditors to establish a security interest.

When does UCC filing happen?

This step depends on the lender and the loan product.

Some UCC filings happen after you’ve secured funding. Others are actually filed when you apply for funding so lenders can protect themselves from borrowers trying to get multiple loans at the same time without the lenders knowing about it.

SBA UCC filings

As a security measure, the SBA will file a UCC lien on EIDL loans of more than $25,000. In this case, the SBA establishes the right to any assets you use to secure your EIDL loan, in the case that the loan goes unpaid.

Is a UCC filing bad?

No. UCC filings aren’t bad, nor are they good. They are used as a safety blanket for lenders to secure loans they provide to borrowers. If you take out a loan that goes unpaid, the fact that there is a filing can become a bad thing, but the UCC filing itself does not impact your credit or ability to obtain future loans.

How do you know if you have a UCC filing?

To find if you have a UCC filing, or simply search UCC liens in general, you can use a public record lien search tool, which are usually available on a State-level.

Most states provide public databases of UCC filings. Click below to learn more about accessing UCC filings in your state:

(Note: In some cases, a subscription might be required for access.)

- Alabama UCC Search

- Alaska UCC Search

- Arizona UCC Search

- Arkansas UCC Search

- California UCC Search

- Colorado UCC Search

- Connecticut UCC Search

- Delaware UCC Search

- Florida UCC Search

- Georgia UCC Search

- Hawaii UCC Search

- Idaho UCC Search

- Illinois UCC Search

- Indiana UCC Search

- Iowa UCC Search

- Kansas UCC Search

- Kentucky UCC Search

- Louisiana UCC Search

- Maine UCC Search

- Maryland UCC Search

- Massachusetts UCC Search

- Michigan UCC Search

- Minnesota UCC Search

- Mississippi UCC Search

- Missouri UCC Search

- Montana UCC Search

- Nebraska UCC Search

- Nevada UCC Search

- New Hampshire UCC Search

- New Jersey UCC Search

- New Mexico UCC Search

- New York UCC Search

- North Carolina UCC Search

- North Dakota UCC Search

- Ohio UCC Search

- Oklahoma (individual counties keep UCC records)

- Oregon UCC Search

- Pennsylvania UCC Search

- Rhode Island UCC Search

- South Carolina UCC Search

- South Dakota UCC Search

- Tennessee UCC Search

- Texas UCC Search

- Utah UCC Search

- Vermont UCC Search

- Virginia UCC Search

- Washington UCC Search

- Washington, DC UCC Search

- West Virginia UCC Search

- Wisconsin UCC Search

- Wyoming UCC Search

How can you remove a UCC filing?

A UCC termination filing requires an amendment be made to the original UCC-1 filing, completed using the UCC-3 form.

Thing is, a UCC-3 form can only be submitted by the lender. To get a UCC lien removed, you must ask your lender to file a UCC-3 form, which then comes at their discretion.

In most cases, liens are not removed until you’ve fully repaid a loan.

In the end, UCC filings typically serve purely as an informational guideline—a “just in case” stipulation. It helps to be aware of any UCC filings you might have, but in general, if you’re paying your debts, UCC liens should not bring you any harm.