You’ve toyed with the idea of starting a healthcare business, but you might not be sure what business you could start. Even if you have a healthcare business idea, you’re not sure if it would be profitable or have the potential to grow over the next few years.

According to the Centers for Medicare and Medicaid Services, U.S. national healthcare spending grew to $4.3 trillion in 2021. This equaled an average of $12,914 per person, and it accounted for 18.3% of the Gross Domestic Product (GDP). While a lot of this money was spent with large healthcare organizations, a considerable amount was paid to private healthcare business owners as well.

Healthcare businesses are not only the focus of so much spending, but also much more likely to survive and thrive. According to the U.S. Bureau of Labor Statistics, only 15.6% of healthcare businesses fail in the first year, significantly below the 21% average first-year failure rate across all industries.

In short, starting a healthcare business is an extremely promising prospect right now. To help you narrow down the direction you could take, we will cover 24 healthcare business ideas—any of which you could start executing over the next few weeks.

Let’s dive in.

Year

Healthcare failure rate

Overall failure rate

1

15.63%

20.90%

2

24.99%

31.42%

3

30.14%

39.32%

4

37.10%

44.54%

5

41.15%

48.37%

Based on U.S. Bureau of Labor Statistics Data of survival rates of businesses started in 2017.

Growth and cost comparison.

Healthcare business growth and cost comparison.

There are multiple factors to consider when choosing which type of healthcare business you want to start, including your own expertise and personal interests. The following chart gives you an overview of the estimated market size, compound annual growth rate (CAGR), and startup costs for common business types within the healthcare industry. Keep in mind that costs can vary considerably, depending on how you set up your business and where you are located.

Business type

Market size

CAGR (Next 8-10 years)

Average startup cost

Medical Billing Outsourcing

11.1 billion

12% (2022-2030)

$12,272

Primary Care Physician

260 billion

3.2%

$70,000-$100,000

Home Health

336 billion

7.93%

Private Pay: $40,000 to $80,000. Licensed Home Health non-Medicare agency: $60,000 to $100,000. Medicare Certified agency: $150,000 to $350,000

Massage Therapy

54.6 billion

8.6% (2022-2032)

$18,308

Medical Transcription

19.8 billion

6.1%

$2000-$10,000

Medical Equipment

59.7 billion

5.7%

$13,936

Nurse Concierge Service

547.8 billion

9.2%

$18,308

Infusion Services

4.6 billion

7.3%

$6000-$20,000

Assisted Living

467 billion

5.9%

Varies based on size and state requirements

Independent Retail Pharmacy

1009 billion

4.8%

$500,000

Medical Waste Handling

21 billion

5.4

$19,267

Sources Below

Healthcare business ideas.

24 healthcare business ideas.

Read on to learn more about individual healthcare business ideas.

At the height of the COVID-19 pandemic, telehealth services rose to the forefront. Now, although many healthcare practices have returned to seeing patients in person, at least 37% of U.S. adults continue to use telehealth services. This is where your telehealth software solution could come in.

An app or software that enhances the telehealth experience is always welcome in the market. This may include tools that allow healthcare providers, such as doctors and nurse practitioners, to monitor their patients whom they are serving remotely or even virtual reality telehealth solutions.

2. Medical equipment rental and maintenance service.

Medical equipment is expensive. Renting can be a cost-effective way for some families to get a piece of medical equipment their loved one needs. With a medical equipment rental service, you could start to fill this gap, connecting patients in need with the right devices. In addition to renting equipment, your business may also provide certified technicians and engineers to maintain the equipment and carry out repairs.

3. Nurse concierge service.

If you’re an experienced nurse who is looking for a change of scenery beyond bedside nursing, you could consider concierge nursing. Concierge nursing is private nursing and it can span a variety of patient types. For example, if you have pediatric nursing experience, your concierge nurse business could focus on caring for children. Other nurse concierge services specialize in providing care services for high-income clientele.

With a host of niches to be filled with a concierge nursing business, your possibilities are endless.

4. Medical staffing agency.

In the U.S., it can take up to 90 days to fill a vacant registered nurse role. Meanwhile, many hospitals are understaffed and need talent quickly to fill the need. Medical staffing agencies act as matchmakers between professional medical professionals and the health organizations that need them.

They can be critical in shortening this long timeline and create a win-win scenario for both sides. The medical professional avoids the burden of applying with 10 or 15 employers to find the perfect role. Once they apply with a medical staffing agency, the agency does the work of finding roles to suit the professional’s needs. In turn, the hospital organization benefits by gaining access to vetted professionals and filling staff shortages faster.

5. Sole practice business.

If you’re a licensed healthcare professional who can practice independently, starting a sole practice such as your own medical, dental, optometry, chiropractic, or physical therapy practice may be the most logical business for you to start.

6. Medical billing service.

Effective billing is the lifeblood of any health practice. While bigger institutions may have their own internal billing departments, smaller healthcare businesses and medical practices often depend heavily on medical billing services to keep the lights on. If you’re thinking about starting a medical billing services company, you will always find high demand in the marketplace.

7. Home healthcare agency/homecare agency.

Medical home health agencies offer nursing care to seniors, people recovering from surgery or a severe illness, or for people who are on hospice/end-of-life care. Home healthcare professionals may also come into private homes to help disabled adults with their long-term medical needs. Non-medical home care agencies help a wide range of clients (including the elderly and disabled adults) with activities of daily living, such as bathing, dressing up, and companion care.

8. Massage therapy

As a massage therapist, you can break out on your own and start a business. Depending on where you live, this might mean investing in proper licensing. In most jurisdictions, you cannot start a massage therapy business unless you are a licensed massage therapist. Regardless, many massage therapists are able to find high demand for their services and make a strong income serving their clients.

9. Outpatient substance abuse management.

For people trying to overcome an addiction to drugs or alcohol, getting the right medications, counseling, and tools during their recovery period is crucial. For those who may want or need to do this outside of a residential recovery center, outpatient addiction and management recovery services are crucial. If you have training and specializations in mental health and substance abuse care, you could start such a business. This can be done from an office or even remotely.

10. Medical supply courier services.

Medical supply courier services (sometimes called health logistics services) deliver medical equipment to homes, hospitals, and medical practices. Running a medical supply courier service requires that you know how to handle and safely transport medical equipment and supplies. In some states, starting a medical supply courier service will require that you have a pharmacy degree.

11. Drug testing business.

The U.S. Department of Transportation requires certain safety-sensitive employees to undergo drug testing. Moreover, many public and private companies require drug testing as part of their pre-employment and onboarding processes. In addition, drug testing may also be needed in certain legal cases. All of this points to a massive market for drug testing services and a potentially lucrative business idea for nurses (RNs and LPNs) and doctors.

12. Infusion services

For patients who have been discharged from the hospital but still need medications to be infused into their bodies via an intravenous (IV) line while they recover at home, infusion service businesses are critical.

Infusion service companies are sometimes based in an office, where patients come in weekly or monthly to receive their medication. Others are run via a mobile infusion service that attends to people in their homes.

13. Medical apparel sales.

Whether it’s a pair of scrubs or a white coat or comfy shoes for medical professionals who stand and walk all day, medical professionals need their uniforms. You could manufacture your own scrubs or it is possible for you to wholesale and put your private label on medical apparel.

14. Medical waste handling.

When it comes to the handling of medical waste, like used syringes, needles, tubing, and soiled wound dressings, federal and state regulations abound. To stay on the right side of these regulations, hospitals and practices of every size need reliable medical waste management services, opening yet another potentially profitable business opportunity.

15. Medical laundry services.

Besides handling medical waste, hospitals often need professional laundering services to take care of bedding, hospital gowns, and hospital-provided attire like surgical scrubs. Your medical laundry services business could meet this need and provide a solid income at the same time.

16. Assisted-living services.

Assisted-living services provide residential services to seniors. Seniors who live in an assisted living facility may do a lot for themselves, but still need help with daily living activities like bathing, grooming, and mobility. Assisted living services may also provide health-related services like nursing care and medication assistance.

17. Senior day care center.

Instead of opting for an assisted living community or senior community, more and more elders are choosing to age in place, living at home for the rest of their remaining years. Other seniors may also live with adult children or caregivers who have to go to work during the day.

To stay safe and to have people to socialize with during the day, these elders may opt to go to a senior daycare center, where they can receive professional care and assistance with their medications, as well as participate in social activities.

18. Medical transcription service.

Medical transcriptionists transcribe recordings made by doctors, nurses, and other medical workers into legible medical records, including notes from patient examinations and discharge reports. They might also review documents for errors, so that facilities can keep accurate records.

While some hospitals and medical practices may have their own in-house medical transcriptionists, there are other organizations that rely on external medical transcription services.

19. Legal nurse consulting.

Legal nurse consultants are registered nurses who have further training that allows them to be assets to attorneys and the legal system. For instance, when there is a malpractice, worker’s compensation, or personal injury lawsuit, attorneys may depend on a legal nurse consultant’s background in the healthcare system and medical science to help build their case. As a legal nurse consultant, you would operate independently. If you have extensive experience in a particular nursing field (e.g., oncology), starting your own legal nurse consultancy that serves that vertical can be a great business.

20. Hydration therapy business.

This business can be similar to the infusion services idea mentioned above. But while infusion services often focus on delivering medication for health conditions, hydration therapy is a simple treatment that delivers fluids and electrolytes (and sometimes, medication), directly into a person’s bloodstream through an IV line.

In most states in the U.S., licensed healthcare professionals, including medical doctors, nurse practitioners, and nurses, can start a hydration therapy business.

21. In-home physical and occupational therapy services.

Your in-home physical therapy and occupational therapy business could help seniors, people with disabilities, or individuals recovering from an illness or accident. Like some of the private care businesses mentioned already, this kind of business allows patients to receive one-to-one care in the comfort of their homes.

22. Autism support services.

Autism support service businesses can provide personal or group support services to individuals on the autism spectrum. Autism support businesses may provide a host of services, including applied behavioral therapy, speech, and occupational therapy services.

23. Retail pharmacy store.

Don’t let big chain pharmacy stores intimidate you. If you have the proper education and licensing to be a pharmacist, you can still make money as an independent pharmacy store owner.

24. Non-emergency medical transportation.

Non-emergency medical transportation (NEMT) services help patients get to their healthcare appointments on time. While the guidelines differ from state to state for starting your NEMT business, it is likely you will need basic training in CPR and first aid. If your NEMT business transports people who use wheelchairs, you might also need special training on how to securely transport these individuals.

Execute your healthcare business idea today.

While several of these businesses require you to have a specific healthcare degree in order to start, there are others on this list that don’t require degrees. And in almost each case, instead of reinventing the wheel, you will be starting a tried-and-tested business.

Forty-one percent of healthcare businesses fail by their fifth year. There are various reasons why this may happen. But often, a lack of funding to support the business is one of those reasons. Learn how you could get the money you need to fund your healthcare practice or get the medical equipment you need to start today.

Crowdfunding is a term used to describe individuals coming together to support—and directly fund—projects by other individuals and organizations. For small businesses and startups, crowdfunding can be an engine for job creation and development.

Compared to other methods of raising money, crowdfunding is very new, but has nonetheless already provided many businesses with the capital they needed to jumpstart and expedite their growth and potential.

What is crowdfunding?

Crowdfunding is a term used to describe individuals coming together to support—and directly fund—projects by other individuals and organizations.

Types of crowdfunding.

Types of crowdfunding.

Prospective and established small business owners can use crowdfunding platforms to jumpstart their next project, and there are four models of crowdfunding they employ to do so:

Donations, philanthropy and sponsorship - Like it sounds, this form of crowdfunding involves people donating money for nothing in return.

Lending - Also known as peer-to-peer lending, this model involves individuals lending a certain amount of money to be repaid with interest.

Equity-based crowdfunding - The company sells shares of the company.

Rewards-based crowdfunding - Anyone who donates money receives a reward, such as a discounted product or swag.

Anyone with questions about crowdfunding should first decide what they’re willing to give (if anything) and how they intend to excite potential donors to invest in their company.

How crowdfunding works.

How does crowdfunding work for businesses?

For a business that wants to use crowdfunding to raise capital, the first step is to decide what type of crowdfunding it wants to pursue. All types are available to small businesses, but there are benefits and drawbacks to each.

Businesses that want to avoid paying additional taxes may want to steer clear of a rewards-based crowdfunding campaign. While the reward is given in exchange for a "donation," to the IRS, it is a sales transaction and is considered taxable income.

To start a crowdfunding campaign, you’ll need to choose a crowdfunding platform. Crowdfunding platforms revolve around a specific type of crowdfunding. They're all a little different and are often aimed at specific demographics.

Once you've decided on the type of crowdfunding campaign you want to run, you will need to create a campaign page that explains what you need the money for and how you intend to spend it. Successful campaigns often provide videos to help motivate and excite donors.

Do crowdfunding sites charge money?

Yes, they do. The amount varies with each site, but it’s not uncommon for platforms to charge 5% or more of the total funds raised, plus a transaction fee for each donation. If you have an exact amount you need for your small business, you’ll need to calculate the fees when determining how much you need to raise.

Can crowdfunding money be used for anything?

Any money raised through crowdfunding must be used for the exact purpose stated to the public. Therefore, if you state that you need the money to cover manufacturing costs, you cannot turn around and use any funds raised to purchase stock or real estate.

Crowdfunding pros & cons.

The pros and cons of crowdfunding.

Consider the following pros and cons when considering using crowdfunding to fund your business.

Pros:

Serves as a marketing tool - Crowdfunding can be a company’s first exposure to the world and can therefore be used as a means to advertise to the general public

Provides a forum for feedback on the project - It’s common for investors to provide needed feedback on a service or product they have invested in; this feedback may be essential for your company’s long term success in the market

Fees are minimal - Crowdfunding platforms take only a small percentage of the funds you raise from investors

Inexpensive way to raise funds - No traveling is needed to speak with investors, nor does it cost that much to establish. You can spend money to launch and run a campaign, but the amount you spend is up to you.

Can make it easy to communicate to your investors -With all of your investors in one spot, communicating to them is a lot easier.

May not have to give up equity depending on which type of crowdfunding campaign you choose -Equity crowdfunding is just one type of crowdfunding. Other methods don’t require selling portions of your company, which means you will be able to keep more of the profits for yourself.

Is a valid alternative to bootstrapping and debt -Not too long ago companies had very few options when it came to raising money, but crowdfunding has changed that.

Can create excitement over your project or product -Smart companies realize that raising money through a crowdfunding campaign is only one benefit—the other is generating buzz and excitement pre-launch.

Provides partial proof of concept - While a successful crowdfunding campaign is not complete proof of concept, it is still a very good sign. Full proof of concept is only established once the product or service is launched and is financially successful

Cons:

Often limited on amount of funding you can raise -Companies can not raise more than $5 million in a 12-month period

Exposes project to the public, risking copycats - it’s not uncommon for companies to avoid crowdfunding altogether if they are currently unable to afford a patent because some companies use crowdfunding sites to get ideas for new products

Funds may be subject to securities regulation - Companies selling securities via crowdfunding must comply with all federal security laws, regardless of the platform they choose

Takes a lot of work to find investors -It’s unlikely investors will find your page on their own and give you money. Successful campaigns often involve full-blown social media activity to attract attention.

Takes a lot of work to create a campaign - Making a donation page, shooting a video, and filling out all of the appropriate paperwork takes more time than you may be willing or able to give.

Dwindled influence of the crowdfunding model - Thanks to too many scammers, some investors have grown weary of crowdfunding altogether.

Does not necessarily show proof of concept - There are many examples of "successful" campaigns that did not translate to the real world of business.

Can be expensive to get going - If you contract your campaign’s creation, you may end up having to spend more than you want.

Too much competition on crowdfunding sites - Just creating a campaign is unlikely to be enough, and it can take a lot of work to have your project stand.

Crowdfunding sites

Crowdfunding sites

Popular crowdfunding sites include:

Indiegogo

Classy

Seedinvest

FundRazr

Fundly

Startengine

GoFundMe

Mighty Cause

Kickstarter

Fundable

WeFunder

EquityNet

Patreon

To choose the best crowdfunding site, decide which type of campaign you want to create and compare the fees charged on each. It’s rare for investors to scroll through campaigns. Instead, many learn about investment opportunities on forums and social media. Therefore, don’t worry too much about where you launch your campaign because everything comes down to how it’s promoted.

Crowdfunding tips

Tips for a successful crowdfunding campaign.

Like any other type of business financing, crowdfunding requires strategic thought, upfront work and a commitment to reach out to potential investors. Consider the following tips when planning your crowdfunding project.

Choose the right site for you - Some sites occupy a specific niche, such as arts or nonprofits. Find the one that fits your business and your ideal donor demographic. You can run multiple campaigns at the same time through different sites, but you will want to consider how.

Set a realistic target and time limit - Asking for too much or too little can affect your project’s chances of success.

Create a campaign video - A personal touch—which video excels at— can pay off. In fact, projects with videos outperform those without by 125%.

Post regular campaign updates - Keep supporters engaged to maintain momentum. The more buzz and excitement you can generate and maintain for your project, the more likely your donors will recommend your project to their peers. If done correctly, they may even promote your campaign for you.

Connect with friends and family first - Begin with word of mouth among your inner circle, then promote your campaign on social media. Some donors are more likely to contribute if they feel the campaign is already in motion and gaining traction.

Offer rewards - Supporters may be more eager to back you if you offer a small incentive. Just remember that doing a rewards-based crowdfunding campaign means you will pay tax on any money received.

Crowdfunding is an exciting new way to raise money for your small business, and there are a lot of opportunities to be had. However, you may still require additional capital after your campaign ends even if it is successful.

With the rise of the so-called “unicorn startup,” it can be easy to get caught up in the myth that, to start a successful new business, one must be young, have millions of dollars of funding, and plan to grow the business to be the size of Facebook or Amazon. The number of startups funded by venture capital has risen over the years. However, most small businesses start without external investment, and the majority of startup founders are middle-aged.

Failure rates

Startup failure rate statistics.

Startup companies are often considered the backbone of economic growth and innovation, with the potential to disrupt traditional industries and create new markets. However, the reality is that starting a business is risky with no guarantee of success. In fact, statistics show that the majority of startups fail within the first few years of operation.

Starting a new business is a risky venture. This underscores the importance of careful planning, market research, and a solid business strategy to ensure a greater chance of success.

While surviving the first year is crucial, it is not enough for long-term success. This highlights the need for sustained growth, innovation, and adaptability to keep a business thriving over the long term.

Oregon, South Dakota, Mississippi, California, and Massachusetts have the highest five-year survival rates of 55% or more. Missouri has the highest five-year failure rate at 60.5%.

Location can be a significant factor in a startup's success or failure. This may be due to a variety of factors, such as a less-supportive business environment, lower access to capital or talent, or other systemic barriers.

Startup challenges

Startup challenges statistics.

Starting a new business is an exciting and rewarding experience, but it is also a daunting task that comes with a host of challenges. So, what is standing in the way of startups’ success? From securing funding to developing a viable product or service, entrepreneurs face numerous obstacles that can make or break their business.

41% of small business owners state their No. 1 challenge is related to the economy and inflation, with another 14% dealing with other financial concerns.

This highlights the need for small businesses to carefully monitor economic conditions, manage cash flow effectively, and seek out resources and support to overcome financial challenges.

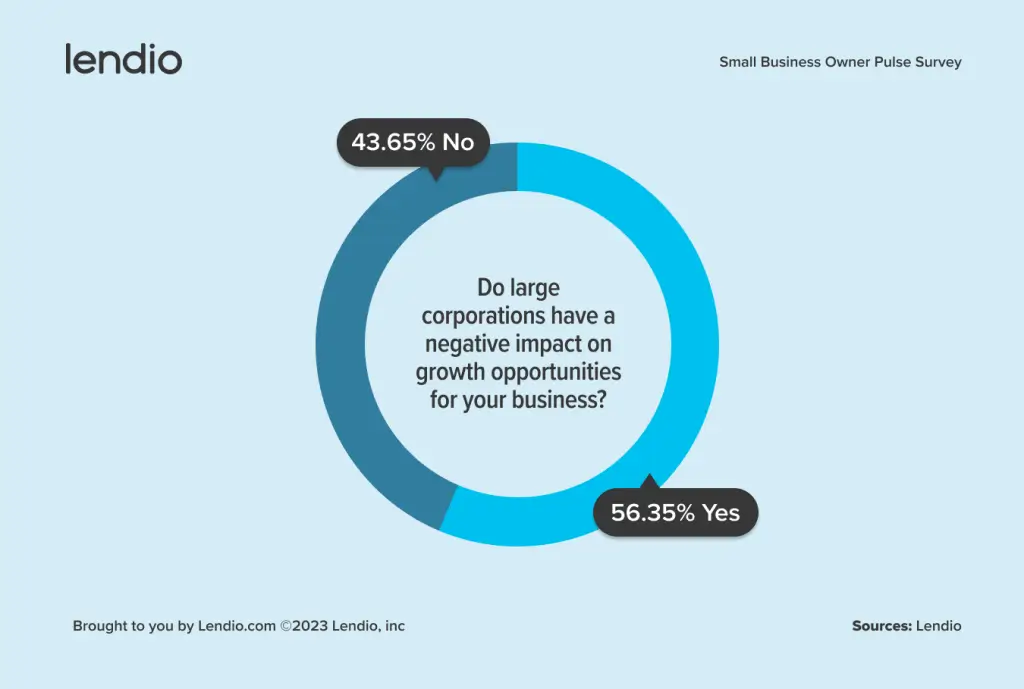

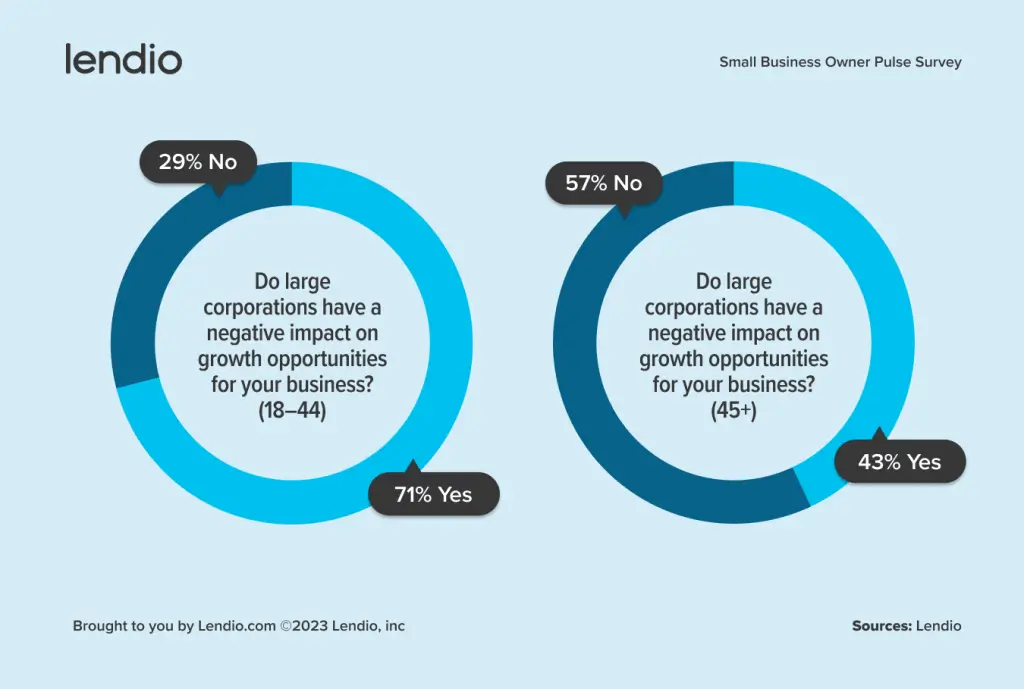

56% of small businesses state that large corporations have a negative impact on growth opportunities for their business.

This may be due to factors such as competition for customers or talent. It may also be the ability of large corporations to invest in technology and marketing that small businesses may not be able to match. As such, small businesses may need to focus on developing unique value propositions, building strong customer relationships, and seeking out niche markets where they can excel.

52% of businesses state access to capital would have had a significant impact in their ability to start a successful business.

This highlights the importance of a robust and accessible financing ecosystem, including traditional loans, venture capital, and alternative sources like crowdfunding.

Startup funding

Startup funding statistics.

Starting and growing a business requires capital, and finding sources of funding is often a top priority for entrepreneurs. From traditional bank loans to venture capital investments, there are numerous options available to businesses seeking funding, but obtaining funding can be a challenge for most early-stage startups. In fact, the majority of businesses are started with personal funds.

54% of SMB owners started their business with personal funds. (Source: Lendio)

43% of small business owners needed less than $10,000 to fund their startup. (Source: Lendio)

Only 3% of startups are funded through venture capital firms. (Source: Lendio)

Colorado, Utah, and Minnesota have the highest access to small business loans. (Source: Lendio)

Massachusetts, California, and New York have the highest amount of venture capital disbursed per $1 million of GDP. (Source: Lendio)

In 2021, early-stage funding totaled $201 billion. (Source: Crunchbase)

Global venture funding was more than 10x higher in 2021 than in 2012. (Source: Crunchbase)

Overall, Kickstarter has successfully funded more than 200,000 projects totaling $6.5 billion in successful funding. (Source: Kickstarter)

40% of Kickstarter projects are successfully funded. (Source: Kickstarter)

66% of Kickstarter startups raise $10,000 or less. (Source: Kickstarter)

77% of tech Kickstarters fail. (Source: Kickstarter)

Unicorn startups

Unicorn startup statistics.

The term "unicorn" is used to describe privately-held startups with a valuation of $1 billion or more. These companies are often seen as the darlings of the tech industry, with the potential to disrupt traditional markets and generate massive returns for investors. While unicorn startups represent only a small fraction of all startups, their impact on the economy and the technology landscape is significant.

There are 1,206 unicorn startups worldwide valued at ~$3791 billion dollars. (Source: CB insights)

Bytedance, an artificial intelligence company in China and parent company of TikTok, has the highest valuation at $140B. (Source: CB insights)

SpaceX has the second-highest valuation at $127B. (Source: CB insights)

Startup demographics

Startup demographic statistics.

Entrepreneurship is often seen as a means of achieving the American dream, with the potential to create wealth and opportunity for individuals and communities. However, not all entrepreneurs have the same opportunities to start and grow their businesses. In fact, access to resources and support can vary significantly based on a variety of demographic factors, including age, race, gender, and education.

Age

Contrary to popular belief, the majority of startup founders are middle-aged, and studies have found that older founders may have a higher chance of success than younger founders.

On average, entrepreneurs are 42 years old when they found their company. (Source: HBR)

In software startups, the average age is slightly younger at 40. (Source: HBR)

In oil and gas and biotechnology companies, the average age is around 47. (Source: HBR)

Entrepreneurs' success rates increase with age, peaking in the mid-50s. (Source: HBR)

Gender

Recent statistics highlight both the progress made and the challenges that remain for women entrepreneurs. On the positive side, startups with female founders are shown to perform better. However, there are still significant disparities in funding and representation. Female business owners tend to ask for less funding than men, and they often face more difficulty securing loans or lines of credit.

Startups with a female founder perform 63% better than startups that have all-male founding teams. (Source: First Round)

The proportion of female co-founded companies has doubled from 10% in 2009 to 20% in 2019. (Source: Crunchbase)

On average, female business owners ask for less funding, about $35,000 less than their male counterparts.

Women business owners make multiple attempts to secure bank loans or lines of credit, and 40% of women business owners applying for a loan never succeed in obtaining funding.

Women represented just 6.4% of the CEOs on the most recent Fortune 500 list—and that was the highest female-male ratio in the list’s 63-year history.

In 2018, Black-owned businesses represented 9.9% of all businesses, while Hispanic-owned businesses represented 12.2%. However, these businesses tended to be smaller and less profitable than non-minority-owned businesses. (Source: Census Bureau)

Only 1% of venture-funded startup founders were Black and just 1.8% were Hispanic. (Source: Stanford)

The National Bureau of Economic Research found that Black-owned businesses were more likely to be denied loans than white-owned businesses, even when controlling for creditworthiness and other factors. (Source: National Bureau of Economic Research)

These startup statistics demonstrate the challenges and opportunities that come with starting and growing a business. While the failure rate of startups can be discouraging, it is important to remember that entrepreneurship plays a vital role in driving innovation and economic growth.

Additionally, it is crucial to acknowledge the systemic barriers that exist in the entrepreneurial ecosystem and work towards creating a more inclusive and equitable environment for all aspiring entrepreneurs. As we continue to track and analyze startup statistics, let us strive to create a world where anyone with an idea and the drive to succeed has the opportunity to do so.

Lendio is committed to helping small business owners survive and thrive by making funding more accessible to small business owners. Learn more about small business loan options.

If you’re in the process of starting a law firm, one of your main concerns is likely how much it will cost. There are many variables that factor into the actual cost to begin your own practice, not to mention how you will fund the whole endeavor. Some attorneys are able to create a firm on a shoestring budget. However, if you are planning on starting big, your initial costs may be more significant.

Here are some things to consider when it comes to law firm start-up costs.

How much does it cost to start a law firm?

It’s impossible to pinpoint exactly how much it will cost you to hang a shingle. However, there are some ballpark considerations that can help you understand your initial budget. Some people are able to start a law firm with a couple thousand dollars. Others need $30,000 or more to begin practice. The exact amount you need depends on your overhead costs and the budget you decide on for items you will need. To determine this amount, consider the following.

Location

Will you have a physical law office or a virtual workplace? If you, like many new attorneys, decide to work from home, you can easily rent a workspace or conference room when you need to meet with clients. On the other hand, having an office space may be important to you. Rent for a physical business location can range dramatically depending on where you are located. If you rent a traditional office space, you may pay $1,000 or more monthly, while renting conference space only when it is needed might cost $200 or less.

Supplies and office equipment

Even if you opt to work from home, you will need certain supplies and office equipment. It’s important to have high-quality printers, scanners, phones, and copiers. For high-quality equipment leases expect to pay $1000/month. You will also need plenty of paper, stamps, pens, note pads, envelopes, and more. These items can add up. However, they shouldn’t amount to more than a couple of hundred dollars per month.

Computer hardware and software

Computer hardware and software will be one of your highest costs when starting a law firm. You will need a quality laptop computer, as well as case management software and document and PDF processing software. These are generally one-time or annual costs, with hardware costing thousands of dollars and software hundreds.

Most legal research databases and data storage in cloud services are subscription-based. You can lower your costs by joining the American Bar Association or your state bar association with free legal research databases. Data storage in cloud services like Dropbox are necessary to ensure your information is secure and you don’t lose valuable files if your hardware malfunctions. These overhead costs may amount to $100 per month or less.

Professional expenses and training

You will need to set aside a budget for professional expenses and training, including licenses, continuing education, conferences, and events. Most states charge companies to obtain a business license, and you will have to pay to maintain your active status as an attorney with the state bar association.

Continuing education is a requirement of all attorneys. While conferences and events are sometimes negotiable expenses, they should be heavily considered to maintain networking and positive appearance. These costs can amount to hundreds or thousands of dollars, depending on the details of the training and events.

Insurance

All businesses need insurance, especially law firms. The types of insurance you need depend on the state you’re in, your practice areas, whether or not you have employees, and other factors. The cost of all these insurance types can vary also, but usually amount to $1,000 or less monthly total.

At a minimum, you should have:

General liability insurance

Property insurance

Malpractice insurance

Workers’ compensation insurance

Cybersecurity Insurance

It’s best to consult with a professional business advisor in your state to ensure you get the right insurance for your new law firm.

New law firm marketing

You will need to invest in marketing for your law firm. However, the amount you decide to put into building a website, social media, Google ads, and other advertising methods depends heavily on your goals. For example, if your target audience does not use social media often, then you can avoid spending money on developing a heavy Facebook presence.

However, one thing you should not skimp on is the quality of your website. And you can achieve a professional site at a low cost or at significant expense. The choice is yours. Many low-cost template options allow you to build your own website. But if you really want to take advantage of SEO tools and rank at the top of Google, you may need to invest in a marketing agency. Many legal marketing agencies offer packages to new law firms for $2,000 to $5,000 monthly to create a website, juggle advertising, and track performance.

Taxes

Every business must pay state and federal taxes. However, the amount you pay will depend on the type of business you form and your annual earnings. It will cost up to $1,000 to have a tax professional keep track of your revenue and expenses and help you complete and file your taxes when the time comes.

Get the funds to start your own law firm

If you are ready to start your own law firm, you should consider all of the costs. Once you create a budget and know how much you need, complete a quick application on Lendio to receive and compare multiple law firm funding offers. Learn more about law firm financing options.

Many newly minted lawyers dream of one day hanging their own shingles. You may be ready to start your own law firm, but unsure of where to begin. Many lawyers, when they first start out, will work out of their home, use their personal cell phone and obtain liability insurance and a simple case management system. This post will explore the steps beyond that if your dream is to build and expand a practice.

Create a business plan

How to create a law firm business plan

One of the first steps in starting a law firm is to create a business plan. This is a document that summarizes your goals and details about operations. It serves as a basis for creating the firm, as well as a roadmap for the future.

Here are some key elements to include in a law firm business plan:

Executive summary stating what your company is

Firm description

Goals and a discussion of how your firm will be successful

Market analysis

Organization of members and management overview

Services offered and practice areas

Marketing strategy and sales goals

Financial plan, including funding needs and fee structure

Financial projections and start-up budget

Budget and financing

Creating a budget and financing a new law firm

Another essential part of starting any new business is figuring out the financial details. When you begin thinking about your new law firm, you need to have a solid understanding of how much it will cost to begin operations and how to get the money you need.

Your initial budget should include everything from startup costs to necessary purchases of hardware and software, including personal computers and case management software. Long-term budgeting should consider:

Recurring subscriptions

Annual bar dues

Personal liability insurance premiums

Law firm marketing costs

Malpractice insurance premiums

Workers’ compensation insurance costs

Unemployment insurance costs

Other expenses for employee benefits

It is possible to start a firm with less than $5,000 in the bank; however, these small businesses often need other financing options down the road. That’s where Lendio comes in. Lendio offers new law firms financing options with a single 15-minute application.

Technology and services

Legal technology and services you may need

The legal industry utilizes a plethora of legal technology and tools that can help lawyers operate a successful practice. While many of these services are not required to practice law, they can make your operation much more efficient, saving time for your staff and money for your clients.

Basic hardware new law firms need

You will need several pieces of hardware to communicate with other attorneys, clients, and courts. Some of the basic hardware you need include:

Computers (preferably laptops)

Printers

Scanners

Phones

You can easily create a paperless law firm wherein you don’t need physical filing cabinets, but that will require additional software and data storage systems.

Software new law firms need

There is an array of innovative software for law firms on the market. These programs benefit attorneys, staff, and clients by making work easier and helping everyone stay organized. Some important software you’ll want to consider for your new law firm include:

Legal practice management system (LPMS)/Case management software

Word processing software (such as Microsoft Word or Google Docs)

PDF readers and editing software (such as Adobe Acrobat)

Interoffice communications (such as Slack or Google Hangouts)

Email software (such as Google or Yahoo)

Office calendaring software

Client relationship management software (CRM)

Data threat security tools (such as Webroot or Norton)

Data or cloud storage

You will need a place to store client documents and other firm information, so that it can be easily accessed by key stakeholders. The most convenient method is to utilize cloud storage through a service like Dropbox.

This storage system can be customized to allow internal or external users to access, upload, and download documents, pictures, and other data. Since the storage is available online, you can have access to it from anywhere, whether you are in the office or about to head to court.

Phone systems

All law firms need to have a phone system, so that clients can easily reach them. While you might be inclined to use your current phone, that will quickly become overwhelming when you gain dozens (or hundreds) of clients. As you’re practice grows it will be helptful to have a dedicated phone line solely for law firm use.

You should also consider using a virtual receptionist who can answer the phones when you are unavailable. This will ensure your clients and potential clients always receive great customer service.

Marketing

New law firm marketing

Legal marketing can feel overwhelming. There are a lot of moving parts, from creating a website to pay per click (PPC) advertising on Google and other platforms. While some firms spend tens of thousands on law firm marketing, that’s not necessary when you’re just beginning your firm. You should create a marketing plan that considers your clients’ needs and how you can meet them in the most efficient way possible.

Branding your new law firm

Branding is one of the most essential parts of new law firm marketing. You want to use effective branding to connect with your clients and put your best foot forward. Develop a logo, slogan, and tone of voice that match your style. Your brand should be presented on everything that you create, from your website to your business cards.

Creating a website

Law firms need to have an online presence. However, it doesn’t have to cost five figures to create a website. If you have time, you can create your own website with templates available online. You may outsource content and SEO (search engine optimization) services to reduce costs and still get good copy. However, there are legal marketing agencies out there who will develop law firm websites for reasonable prices.

Other considerations for running a new law firm

In addition to starting your new law firm, you will have to run it on a day-to-day basis. To do this, you should consider:

Organizational charts, including accountabilities of staff

The American Dream, once the ethos of the United States, offering the highest aspirations and equal opportunities for a comfortable life, has changed. What is the American Dream in 2023, and is the American dream still attainable?

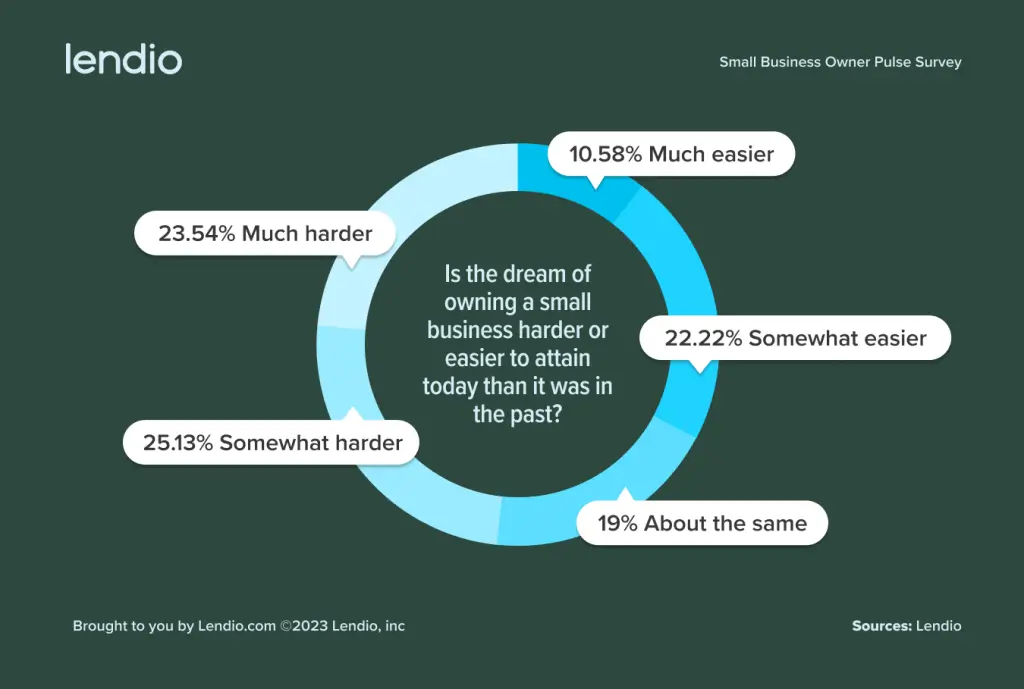

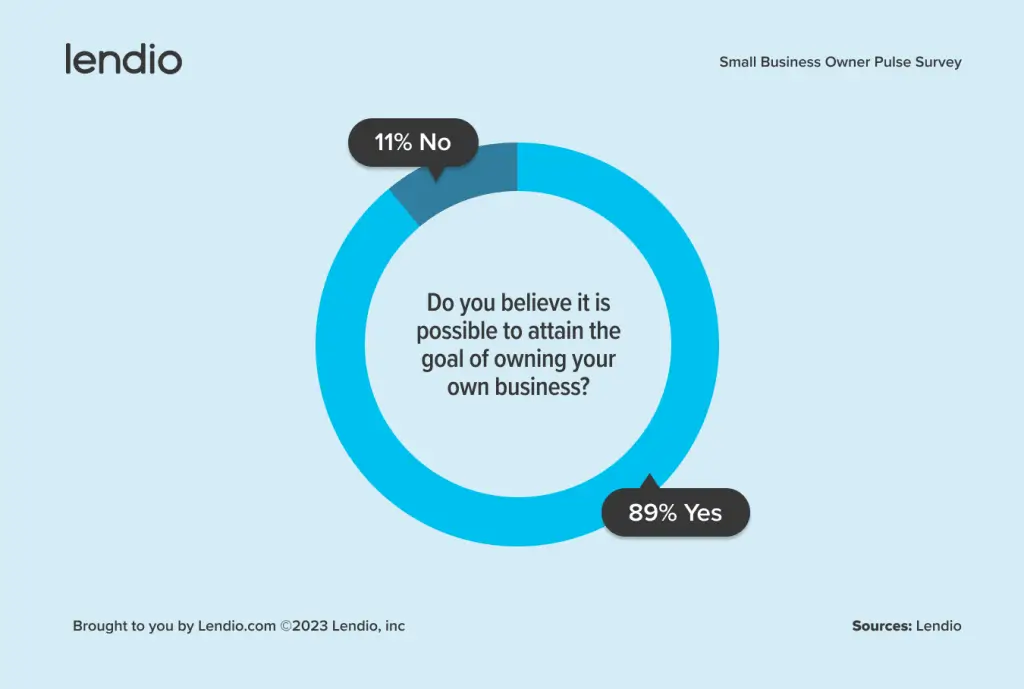

A recent Lendio survey of more than 350 small- and medium-sized business owners across the U.S. found that, while 49% of small business owners believe it is somewhat or much harder to own a small business than it was in the past, 89% still believe it’s possible to reach that goal.

American dream definition.

How small business owners define the American dream.

The original definition of the “American Dream” was based on the prospect of equality, justice, and democracy. Evolving into the belief that anyone can become what they strive to be—the opportunity for upward mobility, economic success, and attaining the life one has always dreamed would be fulfilling.

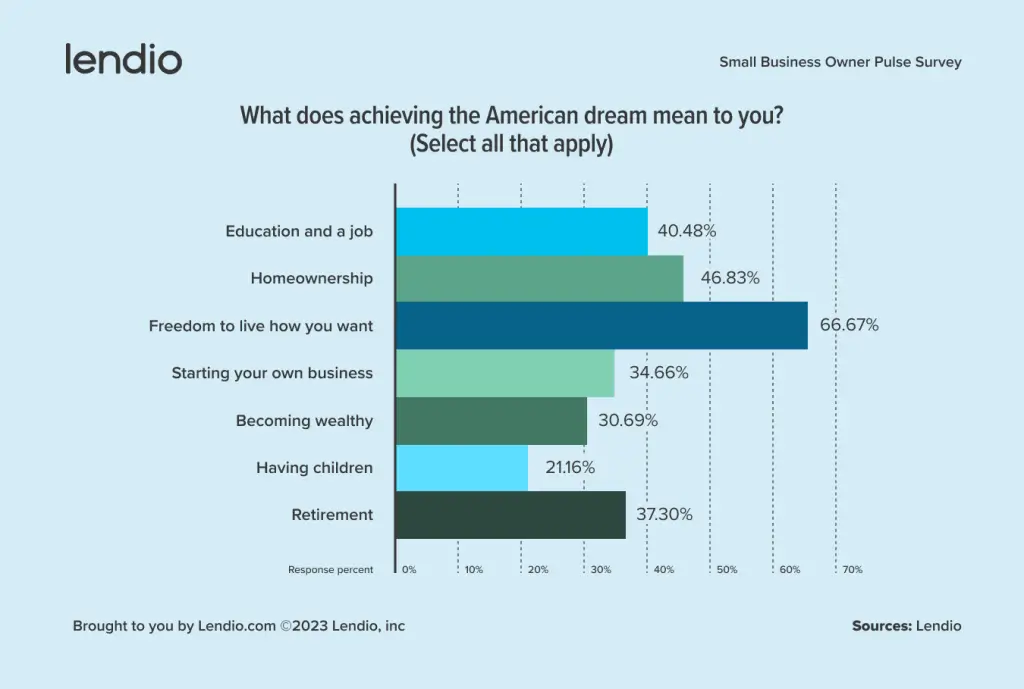

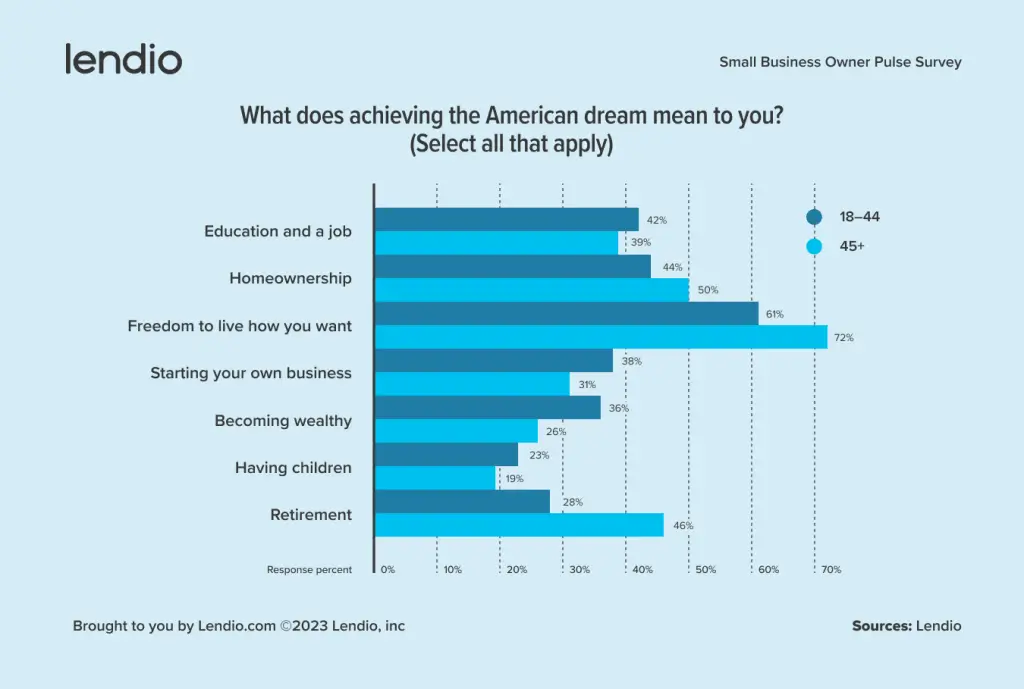

As times have changed, so has the idea behind the dream. While traditional components, such as homeownership (46%) and starting a business (34%), are still identified as important by small business owners, 67% identify freedom to live how you want as the primary component of the American Dream.

What does achieving the American dream mean to you? (Select all that apply)

Response percent

Education and a job

40.48%

Homeownership

46.83%

Freedom to live how you want

66.67%

Starting your own business

34.66%

Becoming wealthy

30.69%

Having children

21.16%

Retirement

37.30%

Based on a 2023 Lendio survey

American dream challenges.

Small business owners remain optimistic but see growing challenges.

Starting a business is a significant step in obtaining the American Dream, and entrepreneurs can face many challenges. There’s no one solution for all businesses. But making a plan and accessing tools make it easier in today’s environment, where small business owners are one click away from equipping themselves in advance. Some of the biggest obstacles to tackle for small business owners include the following:

Funding a business

Finding and keeping customers

Finding and keeping good employees

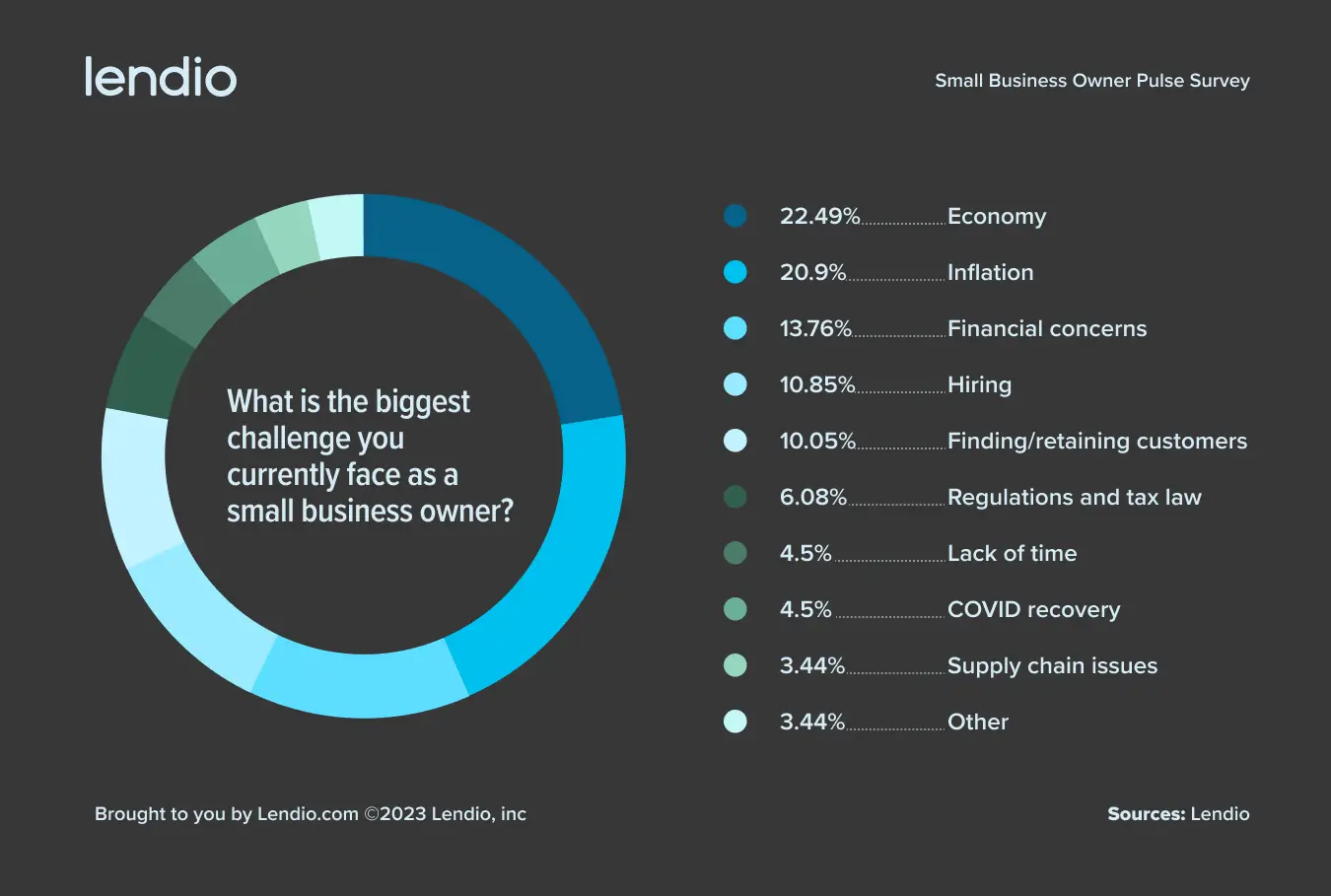

According to the survey, small business owners primarily face challenges related to the economy (23%), inflation (21%) and other financial concerns (14%). Hiring remains a primary challenge for 11% of small business owners. 56% of small business owners state that large corporations, such as Amazon and Google, have a negative impact on growth opportunities for their business.

Generational Differences

Generational differences

Millennials are a highly entrepreneurial group of business owners, with ages ranging from 27 to 42. In this high-rate environment with rising costs, layoffs, and the Great Resignation, we’ve seen a surge in startups. And according to Bloomberg, “creating successful companies is a young person’s game.”

But being an entrepreneur is not just for the young at heart, it’s the American Dream for people of all ages, with 31% of respondents aged 45+ stating that starting a business is part of achieving the American dream. Perhaps unsurprisingly, those owners 45 and above place greater importance on retirement (46%), while those under 45 place more importance on becoming wealthy (36%) as part of the American dream.

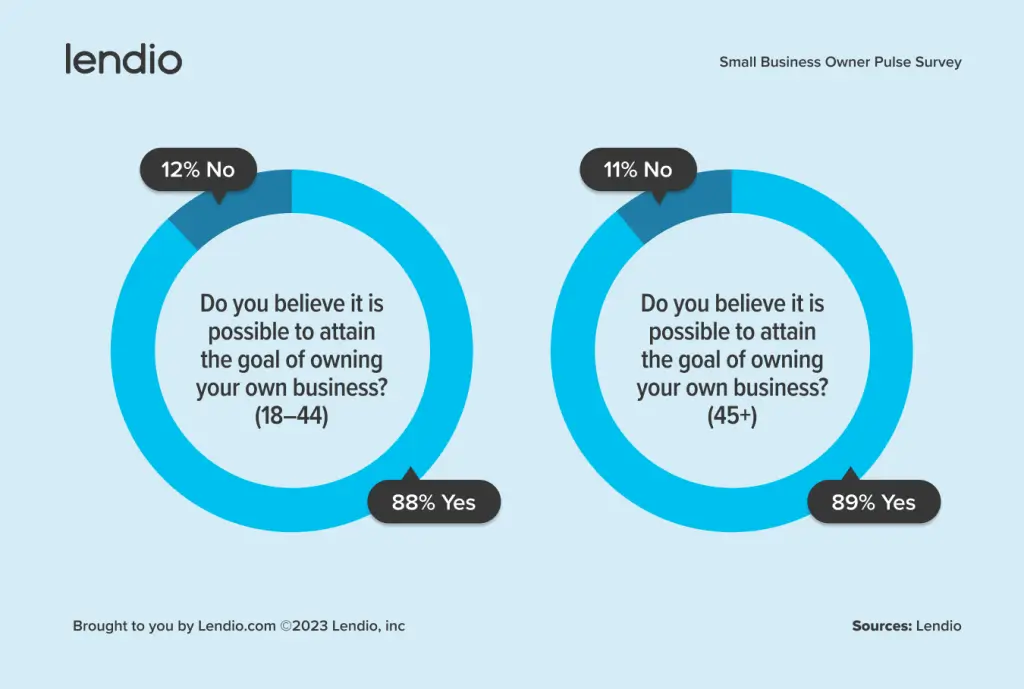

At a certain age, the American Dream can seem easy to give up on or unattainable. The analysis finds a clear correlation between age and sentiment among small business owners. Those over 45 are more pessimistic, seeing the American Dream as more challenging to attain in the current environment. In contrast, those under 45 find it slightly easier to achieve. But entrepreneurship is a reality for both the young and old, with 89% of those age 45+ still believing owning a small business is attainable.

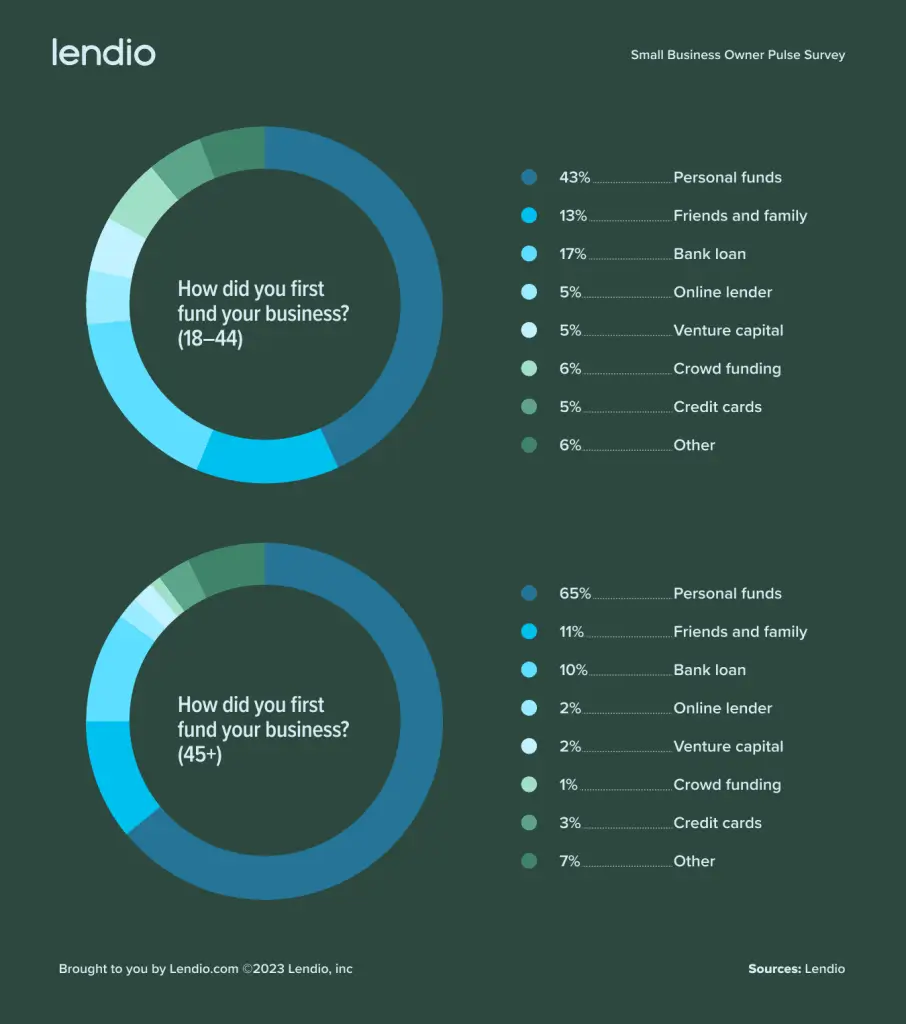

The two generations also fund their businesses differently. While both generations rely heavily on personal funds to start their businesses, those under the age of 45 have started to turn to alternative sources as well, such as crowdfunding (6%) and online lenders (5%).

Access to funding.

Access to funding is key for small businesses.

Access to capital and lower expenses are the key factors for creating an environment where entrepreneurs can start a business.

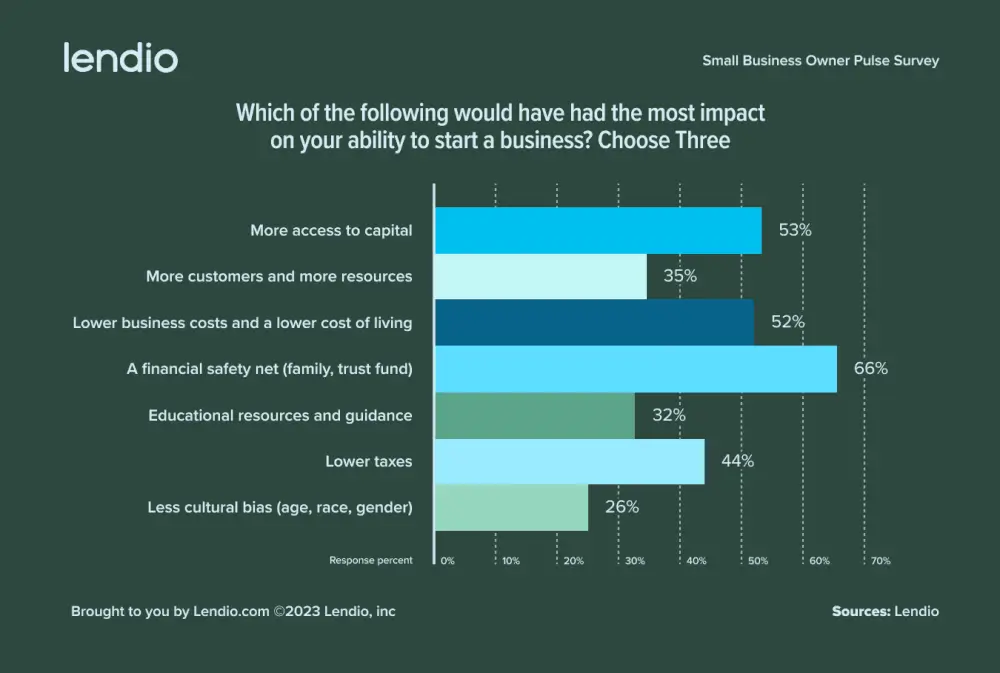

66% of small business owners state having a financial safety net would have had the most impact on their ability to start a business, followed by access to capital at 53%.

Of the respondents, 52% state that living in an area with lower business costs and a lower cost of living would be helpful. 44% state lower taxes would have an impact.

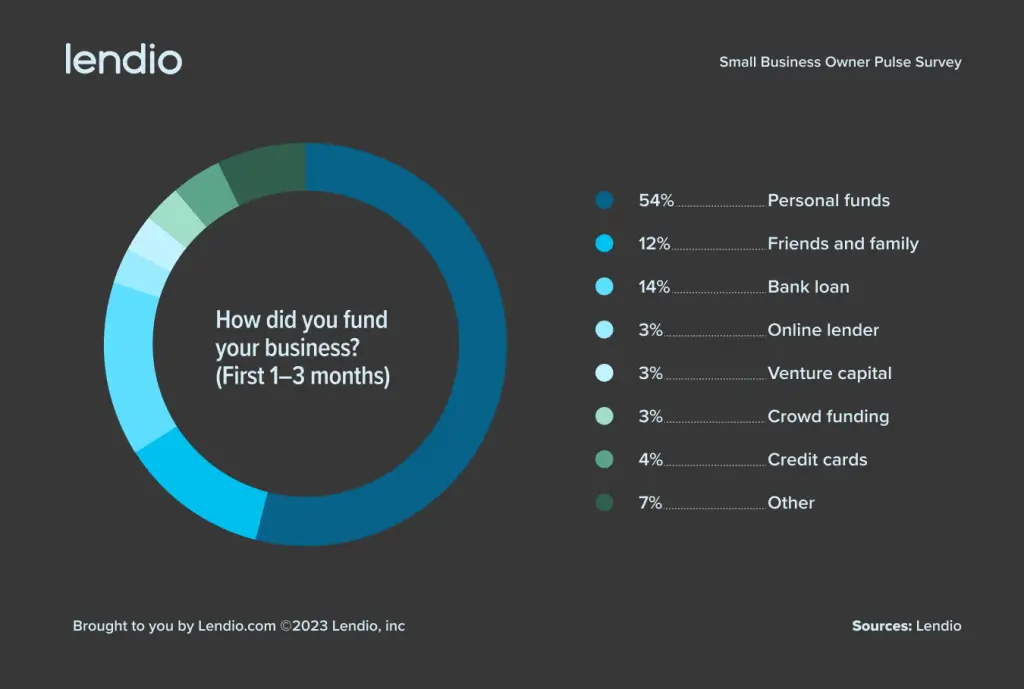

54% of SMB owners started their business with personal funds with another 12% relying on friends and family.

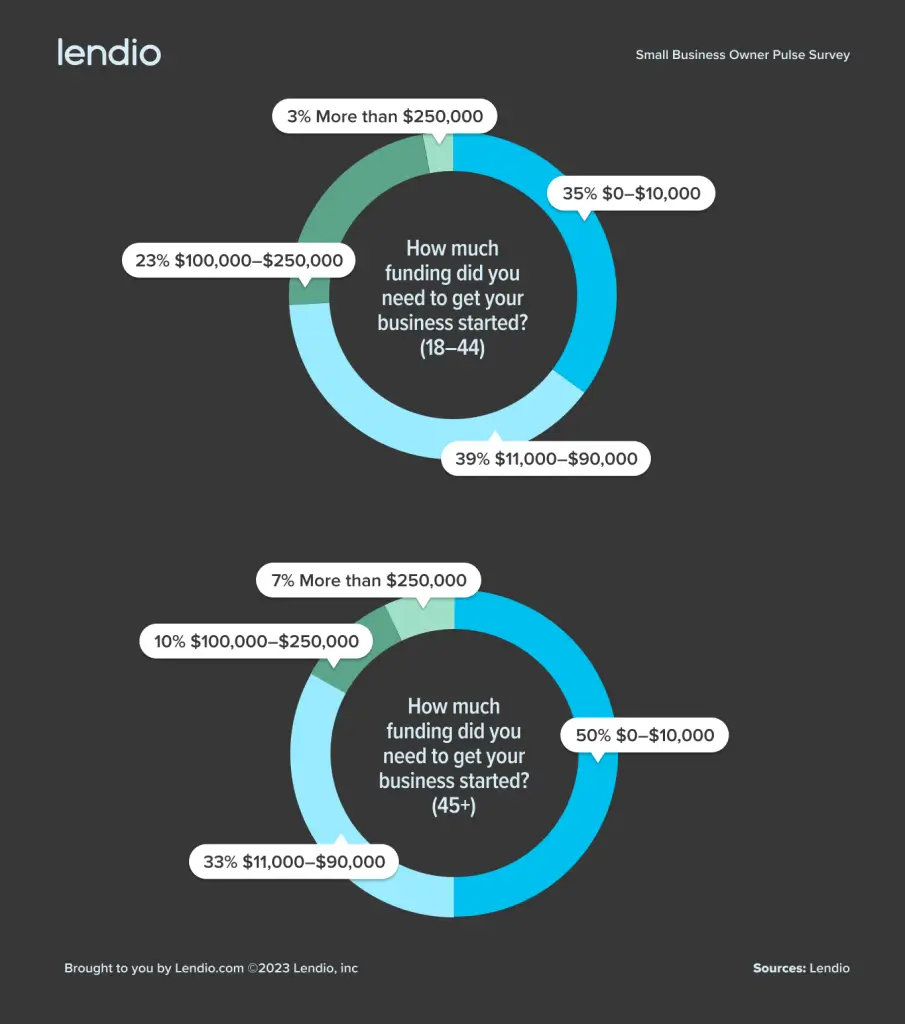

79% of SMB owners needed less than $100,000 to start their business with 43% needing less than $10,000.

Although 49% of respondents believe it’s somewhat or much harder today than in the past to achieve the dream of owning a small business, online loan marketplaces are making it much easier. Lendio is committed to helping entrepreneurs find the right small business loans for their small businesses, so they feel supported and optimistic in achieving their piece of the American Dream.

*Disclaimer: The information, methodologies, data and opinions contained or reflected in Lendio’s Small Business Owner Pulse Survey (the “Survey”) are proprietary of Lendio and is intended for informational purposes only. The Survey does not constitute business or legal advice, and is not a substitute for professional advice. The recommendations provided by Lendio are general industry recommendations, and are not a substitute for your business judgment. The Survey is based on responses to a survey provided by Lendio, but the opinions of those businesses may change over time. Thus, the Survey is not warranted as to its merchantability, completeness, accuracy or fitness for a particular purpose. The Survey is provided “as is” and reflects Lendio’s opinion at the date of their elaboration and publication. Lendio does not accept any liability for damage arising from the use of the Survey in any manner whatsoever. While every effort has been made to ensure that this Survey and the sources of information used herein are free of error, Lendio is not liable for the accuracy, currency and reliability of any information provided in the Survey.

We surveyed 350+ small business owners across the U.S. Here’s what they had to say.

KEY STATS

49% of small business owners believe it’s somewhat or much harder to achieve the dream of owning a small business than in the past.

Those under the age of 45 skew slightly more optimistic with 46% stating owning a small business is slightly or much easier to achieve.

Those over 45 skews more pessimistic; 58% believe it is slightly or much more difficult to reach that dream.

Small business owners are primarily facing challenges related to the economy (23%), inflation (21%) and other financial concerns (14%).

66% of small business owners state having a financial safety net would have had the most impact on their ability to start a business, followed by access to capital at 53%.

54% of SMB owners started their business with personal funds with another 12% relying on friends and family.

79% of SMB owners needed less than $100,000 to start their business with 43% needing less than $10,000.

A small business has been in business about three years (a median of 40 months) when it is first funded by an outside lender and receives a median amount of $47,000.

56% of small businesses state that large corporations have a negative impact on growth opportunities for their business.

Executive Summary

Lendio surveyed more than 350 small-and medium-sized business owners across the U.S. to gather insights about their ability to start and run a small business. The survey included measures of business owners’ most significant challenges, access to capital, impacts on growth, and their ultimate goals for starting a small business.

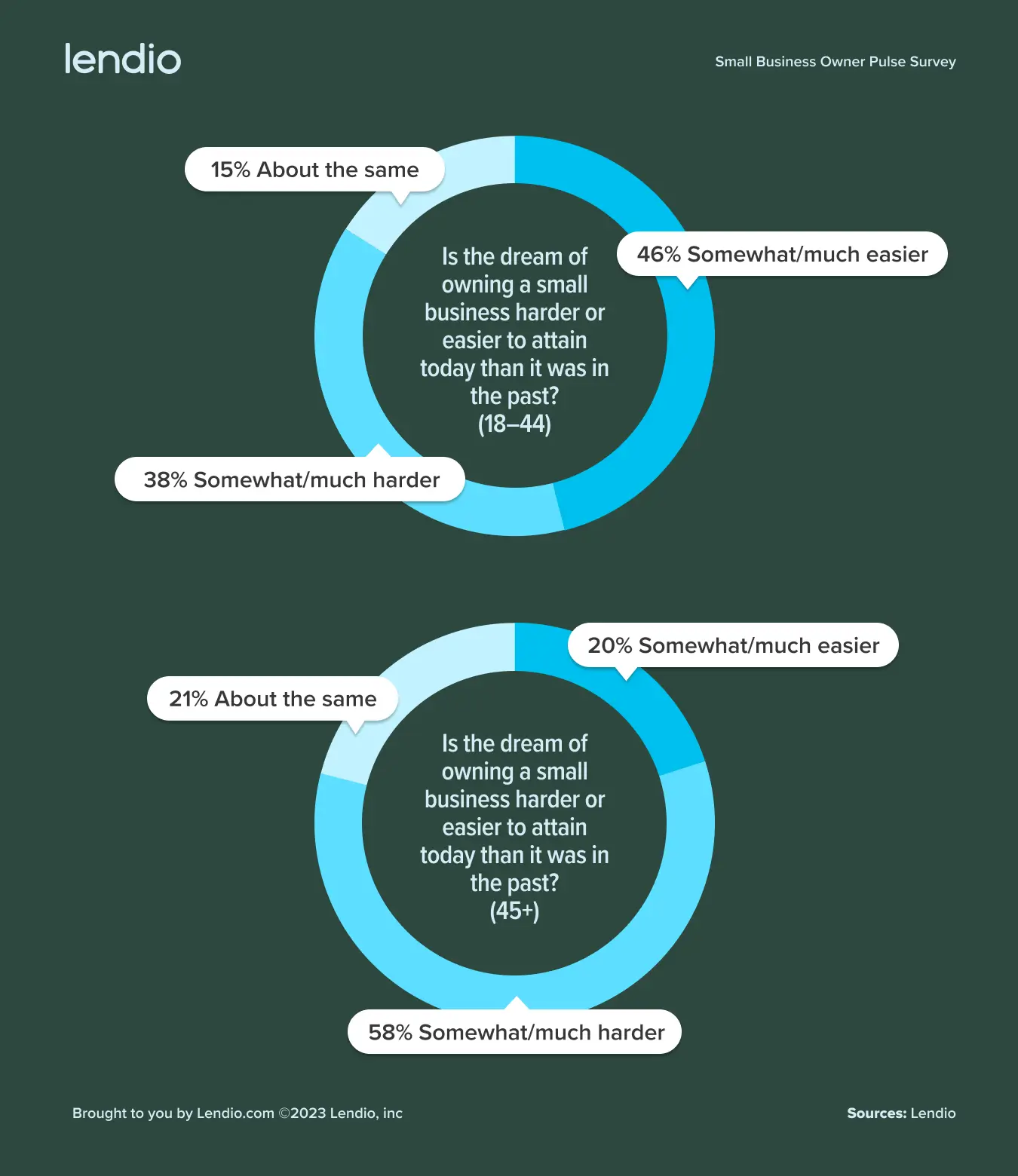

The analysis finds a clear correlation between small business owners’ age and sentiment. Those over 45 are more pessimistic, seeing starting a business as more challenging to attain in the current environment. In contrast, those under 45 find it slightly easier to achieve.

Inflation, economic distress, and labor force were the biggest challenges small business owners cite.

When asked how respondents funded their small businesses, 54% indicated personal funds, followed by bank loans. This survey, along with demographic indicators, can help identify and illuminate the experiences of current and future business owners spanning the different regions of the U.S. Overwhelmingly, responses have consistently shown that access to funding can make or break a company.

“With every business success story comes the ability to have an impact on your community—a ripple effect. 2022 was a challenging year. As we think about the coming year, we’re in your corner, we’re excited to cheer you on, and to help you overcome some of the business challenges you’re facing. We’re optimistic for 2023. We look forward to working with you to get you access to the capital you need to grow your business best.”

Although 49% of respondents believe it’s somewhat or much harder to achieve the dream of owning a small business today than in the past, online loan marketplaces are making it much easier. Lendio is committed to helping entrepreneurs find the best funding options for their small businesses, so they feel supported and optimistic about starting their small businesses.

Key Recommendations*

Based on survey results, we recommend the following to support small business owners:

Loan Access - The rise of online lenders and lending marketplaces has increased access to small business loans, but there is still work to be done to improve small business’s access to funding through automationand faster approvals.

Target Underserved Areas - Lenders should target underserved areas where respondents believe starting a business is less attainable. Those areas tend to also feel greater negative impacts caused by inflation, increasing costs, and economic strains.

Educational Resources - Empowering small business owners through education and resources within their communities can be a major benefit to getting businesses off the ground.

Small Businesses Owners Face Challenges But Remain Optimistic

KEY STATS

49% of small business owners believe it’s somewhat or much harder to achieve the dream of owning a small business than in the past. 33% of SMB owners believe it is somewhat or much easier. 19% say it's about the same.

89% of small business owners believe it’s possible to attain the goal of owning your own business.

While 49% of small business owners believe it is somewhat or much harder to own a small business than it was in the past, 89% still believe it’s possible to reach that goal.

Entrepreneurs can face many challenges when starting a small business. There’s no one solution for all businesses. But making a plan, and accessing tools make it easier in today’s environment where small business owners are one-click-away from equipping themselves in advance. Some of the biggest obstacles to tackle for small business owners include the following:

Funding a business

Finding and keeping customers

Finding and keeping good employees

The Economy’s Effects On Small Businesses

KEY STATS

Small business owners are primarily facing challenges related to the economy (23%), inflation (21%) and other financial concerns (14%).

Hiring remains a primary challenge for 11% of small business owners.

56% of small business state that large corporations have a negative impact on growth opportunities for their business.

The economy is experiencing a slowdown, and the Federal Reserve continues to increase interest rates to tame inflation. Business owners are feeling the effects. In a recent World Economic Forum poll, nearly two-thirds of the economists believe there will be a 2023 recession.

The post-pandemic environment has created many challenges, and small business owners still feel the ripple effects of COVID-19 protocols coupled with inflation. With inflation still at a 40-year high, we asked small business owners about their current biggest challenges.

Small business owners are primarily facing challenges related to the economy, inflation and other financial concerns. Challenges related to Covid recovery and supply chain issues are less of an issue.

Creating An Environment Where Small Businesses Can Thrive

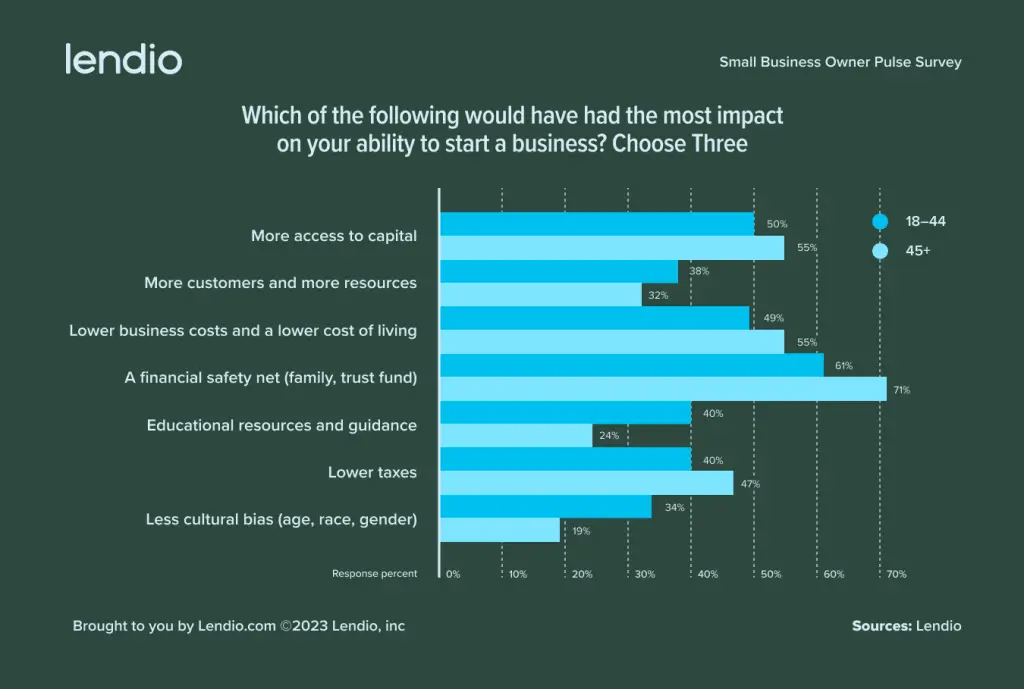

Location, taxes, and socioeconomic factors help to evaluate the best environment for a business which is why we asked respondents to select three choices that most affected their ability to start a business.

Access to capital and lower expenses are the key factors for creating an environment where entrepreneurs can start a business.

KEY STATS

66% of small business owners state having a financial safety net would have had the most impact on their ability to start a business, followed by access to capital at 53%.

Of the respondents, 52% state that living in an area with lower business costs and a lower cost of living would be helpful. 44% state lower taxes would have an impact.

Funding Stats

Start-up funding for a small business can come from one or multiple resources. One of the most common ways entrepreneurs fund their businesses is through savings or friends and family. Alternatively, an infusion of cash from a small business loan may be the way to go. With no shortage of financing options, we asked survey participants how they first funded their businesses.

KEY STATS

54% of SMB owners started their business with personal funds with another 12% relying on friends and family.

79% of SMB owners needed less than $100,000 to start their business with 43% needing less than $10,000.

The average loan amount for a small business owner is $47,000.*

A small business has a median of five employees when it is first funded by an outside lender.*

A small business has been in business for about three years (a median of 40 months) when it is first funded by an outside lender.*

*Based on internal Lendio data of 300,000+ loans funded since 2013.

How Small Business Owners Define The American Dream

The original definition of the “American Dream” was based on the prospect of equality, justice, and democracy. As times have changed, so has the idea behind the dream.

The definition for most small business owners is relatively fluid. While traditional components, such as homeownership (46%) and starting a business (34%), are still identified as important, 67% identify freedom to live how you want to be the primary component of the American Dream.

Generational Differences

KEY STATS

Those under the age of 45 report needing more money to start their business with 23% needing $100K-$250K while only 10% of those aged 45+ needed that amount.

While both generations rely heavily on personal funds to start their businesses, those under the age of 45 have started to turn to alternative sources as well such as crowdfunding (6%) and online lenders (5%).

Millennials are a highly entrepreneurial group of business owners, with ages ranging from 27 to 42. In an environment with rising costs, layoffs, and the Great Resignation, we’ve seen a surge in startups. And according to Bloomberg, “creating successful companies is a young person’s game.”

But being an entrepreneur is not just for the young at heart; it’s a dream for people of all ages, and where economic downturns have historically driven growth, the generations looking to start anew fund their businesses differently.

At a certain age, owning a business can seem easy to give up on or unattainable. But entrepreneurship is a reality for both the young and old. The survey showed a distinct difference in sentiment between younger and older business owners, with older business owners feeling more pessimistic and younger business owners feeling more optimistic.

KEY STATS

46% of younger business owners (18-44) believe owning a small business is somewhat or much easier to achieve.

58% of older business owners (45+) believe owning a small business is somewhat or much harder to achieve.

Despite differing perceptions of challenges both generations agree it’s possible to attain the goal of owning your own business.

The survey also found generational differences in what helps or hinders a small business’s success and what those business owners value most in their life.

While a large majority (71%) of SMB owners aged 18-44 believe large corporations have a negative impact on growth opportunities for their business, 57% of those 45 and above disagree, stating large corporations don’t have a negative impact on their business.

While the generations agree that a financial safety net, access to capital and low costs are most critical to success, those 44 and younger place greater importance on access to educational resources and see cultural bias as a larger inhibitor.

Both generations agree that the freedom to live how you want is the most important component of the American dream. Perhaps unsurprisingly, those 45+ place greater importance on retirement (46%) while those under 45 place more importance on becoming wealthy (36%).

Gender Differences

The survey found relatively few differences between genders other than the amount of funding needed to first start the business.

A significantly greater number of women (49%) needed less than $10,000 to start their business than men (36%).

A significantly greater number of men (21%) needed $100K-$250K to start their business than women (12%).

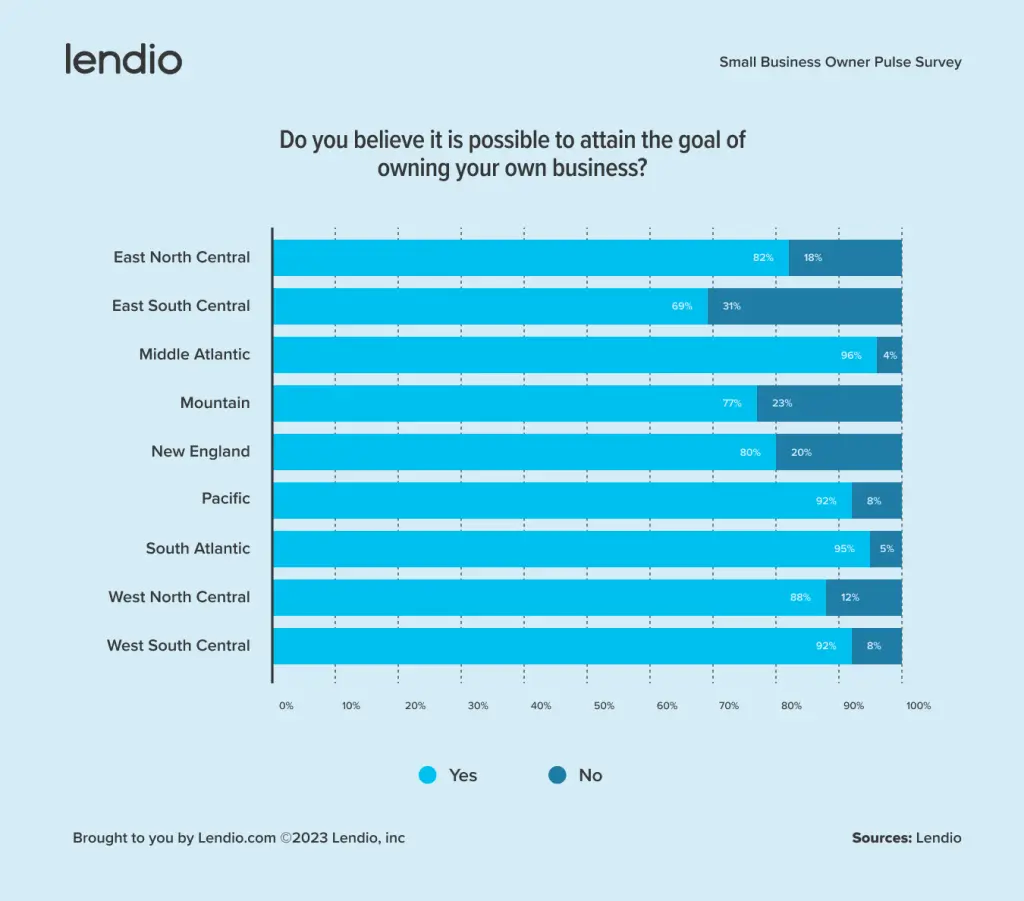

Geographic Differences

There were few significant differences across regions.

The Middle Atlantic region (New York, New Jersey, Pennsylvania) had the most positive sentiment toward being able to start a business with 96% of respondents believing it’s possible.

The East South Central region (Kentucky, Tennessee, Alabama, Mississippi) had the most negative sentiment, with 30% of respondents stating they didn’t believe it was possible to attain the goal of owning your own business.

*Disclaimer: The information, methodologies, data and opinions contained or reflected in Lendio’s Small Business Owner Pulse Survey (the “Survey”) are proprietary of Lendio and is intended for informational purposes only. The Survey does not constitute business or legal advice, and is not a substitute for professional advice. The recommendations provided by Lendio are general industry recommendations, and are not a substitute for your business judgment. The Survey is based on responses to a survey provided by Lendio, but the opinions of those businesses may change over time. Thus, the Survey is not warranted as to its merchantability, completeness, accuracy or fitness for a particular purpose. The Survey is provided “as is” and reflects Lendio’s opinion at the date of their elaboration and publication. Lendio does not accept any liability for damage arising from the use of the Survey in any manner whatsoever. While every effort has been made to ensure that this Survey and the sources of information used herein are free of error, Lendio is not liable for the accuracy, currency and reliability of any information provided in the Survey.

The U.S. Small Business Administration (SBA) offers a variety of attractive loans to small businesses in the U.S. SBA Express loans are one popular loan option you might want to consider if you need no more than $500,000 in funding. Just like other SBA loans, Express loans offer low interest rates and flexible repayment terms that you may not find elsewhere.

Compared to other SBA loans, however, these financing solutions come with much easier applications and faster approval times. Let’s take a closer look at what SBA Express loans are and how they work, so you can decide if they make sense for your unique situation.

What is an SBA Express loan?

An SBA Express loan is part of the SBA 7(a) loan program, which is the most popular SBA funding option. Upon approval from an SBA-approved lender, you can use the funds for a wide variety of business-related expenses, such as commercial real estate, equipment, working capital, debt refinancing, or business expansion.

You can choose from the standard Express loan or Export Express loan and lock in up to $500,000 in funding. While repayment terms depend on loan type and purpose, they go up to seven years for lines of credit, 25 years for real estate loans, and five to 10 years for other loans.

The lender, loan size, and your financial situation will dictate the interest rate you may receive, but SBA Express loans cap out at the prime rate plus 6.5% for loans of $50,000 or less and the prime rate plus 4.5% for loans greater than $50,000. The chart below outlines the key components of these loans.

Types of loans

Standard SBA Express loans, SBA Export Express loans

Maximum SBA guarantee

50%-90% depending on loan type

Loan amount

Up to $500,000

Repayment terms

Up to 10 years for working capital, equipment, and inventory purchases, up to 25 years for real estate, and up to seven years for lines of credit

Interest rates

The prime rate plus 6.5% for loans of $50,000 or less and the prime rate plus 4.5% for loans greater than $50,000

Down payments

Not required. Determined by the lender.

Collateral

Required for loans greater than $50,000

Fees

One-time guarantee fee based on the size of the loan, which can be waived for veteran-owned businesses, and potential lender fees for servicing

Funding times

Depends on the lender, but the SBA will make a decision on standard Express loan applications within 36 hours and Export Express loans within 24 hours

Types of SBA Express loans.

There are two types of SBA Express loans, including standard Express loans and Export Express loans. Let’s dive deeper into the details of each one.

Standard SBA Express loans.

Standard SBA Express loans are designed for qualifying small businesses that operate in the U.S. or the U.S. territories. The SBA responds to applications for these types of loans within 36 hours. With a standard SBA Express loan, you can borrow up to $500,000 and enjoy an SBA guarantee of 50%. While interest rates max out at the prime rate plus 4.5%, they ultimately depend on your qualifications, lender, and loan amount.

SBA Export Express loans.

SBA Export Express loans differ from standard SBA Express loans in that they’re geared toward exporters. If you’re in search of funding to support export activities for your business, this option is worth exploring. The SBA will guarantee 75% of loans that are larger than $350,000 and 90% of loans that are less than $350,000. Approval times are also shortened as the SBA will respond to applications in no more than 24 hours.

How SBA Express loans work.

You can apply for an SBA Express loan through an SBA-approved lender, which may be a bank, credit union, or online lender. To do so, you’ll need to complete SBA Form 1919 and any other forms the financial institution requires. While down payment requirements vary, 10% is typical and startups may have to put more down.

Also, if you opt for an Express loan of over $25,000, you will need to back your loan with collateral. If you choose an Export Express, you’ll need to adhere to the particular collateral requirements set forth by your lender.

Even though each individual lender will make their own eligibility decisions, the SBA will respond to Express loan applications within 36 hours and Export Express loan applications within 24 hours. This is much faster than the five to 10 business days the SBA usually takes for other types of loans. Keep in mind that funding times are also lender-dependent, but are typically completed within 30 to 60 days.

How to take out an SBA Express loan.

If you’re interested in an SBA loan, follow these steps to get one.

Determine your borrowing needs: Since SBA Express loans cap out at $500,000, it’s important to figure out how much money you need. If you’d like to borrow more than $500,000, you may have to explore alternative financing solutions.

Verify your eligibility: Before you go ahead and apply for an SBA Express loan, make sure you meet all the criteria. Your business must be considered a small business by the SBA and have reasonable owner equity to invest. Plus you’ll need to prove that you’ve already invested financial resources toward the business. In addition, you’ll be required to meet the individual lender’s criteria, which may include a minimum credit score of 650, at least two years in business, and strong annual revenue.

Choose a lender: Not all SBA lenders are created equal. That’s why you should shop around and find the ideal option for your unique situation. You can always use the SBA lender matching tool on the SBA website to help you out.

Fill out SBA Form 1919: Once you decide on a lender, complete SBA Form 1919. Be prepared to share information about who owns the business, what you intend to do with the funds, the number of employees you have, and whether you’ve received any SBA loans in the past. Double-check your work to avoid errors and inaccuracies, which may lead to delays with approval and funding.

Submit documentation: Some lenders will ask you to provide certain supporting documents with your application. These may include business credit reports, financial statements, personal and business tax returns, and a business plan.

Wait for approval: As stated, the SBA will respond to standard Express loan applications within 36 hours and Export Express loan applications within 24 hours. Once the lender receives the green light from the SBA, it’s up to them to approve your application and distribute the funds. In most cases, however, you’ll be able to close on your loan within 30 to 60 days.

Pros and cons of SBA Express loans.

Like most business financing solutions, SBA Express loans come with benefits and drawbacks you should consider, including:

Pros

Fast turnaround times: If you’re in need of an SBA loan with quick approval and funding times, the SBA Express loan may be a good option. Depending on the type of loan you choose, the SBA may approve your application within 24 or 36 hours. This is quite fast when you consider that it typically takes them at least five to 10 business days to approve other types of loans.

Flexibility with collateral: As long as your loan is less than $25,000, the SBA doesn’t require collateral. If you don’t want to put your personal or business assets on the line, you’re sure to appreciate this type of flexibility.

Easier application: Compared to other types of SBA loans, SBA Express loans have simpler applications. It won’t take you as long to apply for them, so you can expedite the process of securing funding.

Cons

Smaller borrowing amounts: SBA Express loans cap out at $500,000. While this might seem like a lot of money, it might not be sufficient if you have plans to purchase expensive equipment or acquire a business. You might want to consider the traditional SBA 7(a ) program if you need to borrow more money.

Must meet certain qualifications: Unfortunately, SBA Express loans aren’t available to just anyone. To take advantage of them, you must meet stringent criteria set forth by the SBA and the lender you choose.

Lenders may take a while to distribute funds: Even though the SBA approves SBA Express loan applications quickly, it’s up to the individual lenders to provide funding. Depending on the lender you choose, you may still have to wait weeks or even months for the money.

Bottom line

If you’re in the market for an SBA loan, but want to skip the lengthy application and longer approval times of the traditional SBA 7(a) loan, the SBA Express loan should be on your radar. Before you sign on the dotted line, however, weigh the pros and cons to ensure you’re making the most informed decision. Learn more and apply for SBA loans.

Social media can be a game-changer for small businesses—if you know how to use it. This guide covers everything from choosing the right platforms to creating engaging content and growing your audience. With actionable tips and proven strategies, you’ll learn how to turn likes and follows into real business results.

Email marketing is one of the most powerful tools for small businesses—when done right. This guide covers everything from building your email list to crafting engaging campaigns that drive results. With actionable tips and step-by-step guidance, you’ll learn how to connect with your audience, boost sales, and grow your business through email.

Digital marketing doesn’t have to be overwhelming. This guide simplifies the essentials, from building an online presence to leveraging social media, email, and SEO. Packed with practical tips and step-by-step strategies, it’s designed to help small businesses succeed in the digital world without a big budget or a full marketing team.

Let’s face it. There’s a lot of bad marketing advice out there. Or great advice that’s far too in-depth for a small business owner who isn’t looking to start a full-time career in marketing. We created this guide to cut through the clutter and provide you with principles, direction and the applicable step-by-step how-tos to get the job done.

Your brand is more than just a logo—it’s the heart of your business. This guide walks you through the essentials of small business branding, from defining your identity and crafting your message to building a strong, lasting impression. With clear steps and actionable advice, you’ll create a brand that resonates with customers and sets your business apart.

Hiring for small businesses doesn’t have to be complicated. Your business can achieve success when you understand relevant legal requirements and find the right job candidates for your open positions. This comprehensive guide covers everything from finding the right employees to hire to employee training and development.

Your best customers are your biggest growth opportunity. This guide breaks down customer marketing strategies tailored for small businesses, helping you turn happy customers into loyal advocates. From building relationships to leveraging referrals, discover actionable steps to maximize lifetime value and drive sustainable growth.

From selecting the right franchise opportunity to navigating the financial aspects, this step-by-step resource equips aspiring entrepreneurs with the knowledge and strategies needed to thrive in the world of franchising.

Have a business idea but not sure where to start? Our comprehensive guide to starting a business has everything you need to know. From legal requirements to market research, we’ve got you covered.

Running and growing a business is no easy feat. Our guide to running a business has everything you need to know to keep things running smoothly. From managing employees to marketing your business, we’ve got you covered.

Take your business to the next level with our Accounting Guide. Master the language of numbers, understand financial statements, and make informed decisions based on accurate financial data. Discover the power of sound financial management.

Master the art of cash flow management with our comprehensive guide. Learn strategies to optimize your cash flow, forecast revenue and expenses, and keep your business financially stable. Take control of your finances and achieve long-term success.

Streamline your billing process with our Invoicing Guide. Learn how to create professional invoices, manage client payments, and maintain a healthy cash flow for your business. Get paid faster and efficiently track your revenue.

A great marketing strategy is the foundation of small business success. This guide takes you step-by-step through defining your goals, identifying your audience, and choosing the right channels. With practical tips and clear direction, you’ll build a tailored strategy that drives growth and delivers measurable results.

Navigate the complex world of taxes with our Tax Preparation Guide. From understanding tax obligations to maximizing deductions and filing quarterly taxes, we’ll help you stay compliant and minimize your tax burden. Unlock the secrets of tax success for your business.

Stay on top of your business finances with our Bookkeeping Guide. Learn the art of tracking income and expenses, maintaining financial records, and keeping your books in order. Unlock financial success with our expert tips.

Need help securing funding for your business? Our business loans guide simplifies the financing process, explains key terms, and walks you through your loan options.